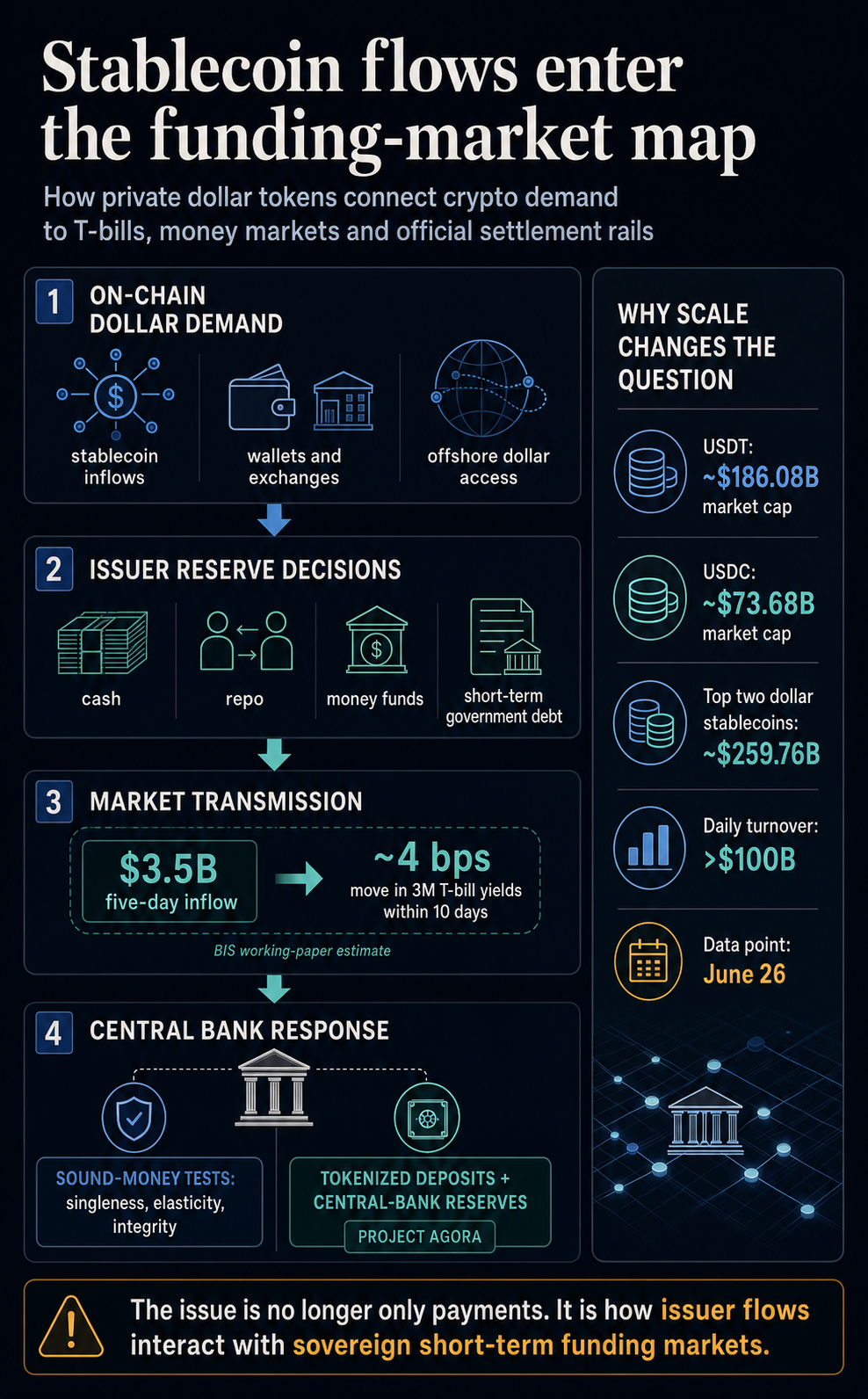

Stablecoin flows have crossed from crypto liquidity into the market map central banks use to trace greenback funding.

The Financial institution for Worldwide Settlements, in its June 23 Annual Financial Report chapter on innovation past stablecoins, argued that non-public greenback tokens nonetheless fall in need of the core assessments of cash. The identical official-sector push now sits alongside a working paper estimate {that a} $3.5 billion, five-day stablecoin influx can transfer three-month Treasury invoice yields by about 4 foundation factors inside 10 days.

The consequence is sensible. Stablecoins have gotten a measurable channel between on-chain greenback demand and the entrance finish of sovereign debt markets.

For crypto, stablecoin development now carries a funding-market sign. For central banks, reserve administration, redemption habits, and tokenized settlement design sit inside the identical coverage dialog.

The cash assessments behind the market danger

The BIS chapter begins from a primary financial check. Cash works as a result of customers can deal with one unit as equal to a different, as a result of the system can provide liquidity when funds have to settle, and since the community can management monetary crime and protect belief.

Stablecoins can transfer quick and might be programmed into public blockchains. BIS acknowledges that utility. Its argument is that present preparations lack the institutional help wanted for financial institution deposits and central financial institution cash to operate as no-questions-asked settlement belongings.

Within the BIS framework, the weak factors are singleness, liquidity elasticity, and integrity. Stablecoins might commerce close to par more often than not, however they lack the identical entry to central financial institution settlement or system-wide liquidity backstops. They’ll additionally fragment throughout chains and venues, making interoperability and monetary integrity more durable to implement at scale.

Adoption modifications the coverage query. A stablecoin used primarily as a crypto quote asset is one other. A stablecoin that turns into a big reserve-backed greenback instrument held throughout exchanges, wallets, and offshore markets is one other.

The issuer then has to determine the place reserves are held, how redemptions are met, and which belongings are purchased or bought as demand modifications.

The clearest quantity comes from the BIS working paper on stablecoins and protected asset costs. The paper estimates {that a} $3.5 billion mixture stablecoin influx, about two commonplace deviations in its pattern, lowers three-month Treasury invoice yields by roughly 0.71 foundation factors on affect and as much as 4 foundation factors inside 10 days.

The paper frames the impact as sample-specific reasonably than a rule for each stablecoin movement. It makes use of each day knowledge from January 2021 to March 2026, native projections, and an instrument designed to isolate shocks to stablecoin flows.

It additionally says the estimate is strongest within the maturity bucket the place issuers are more than likely to carry reserves, and that results are amplified when Treasury-market intermediaries are beneath stress or because the stablecoin sector grows.

That’s the coverage sign within the proof. A four-basis-point transfer in a single short-rate instrument is small in isolation. It’s nonetheless an indication that stablecoin issuers have turn into massive sufficient for his or her reserve allocation to indicate up out there used to cost protected greenback liquidity.

The companion BIS paper on making stablecoins secure(r) provides the opposite facet of the identical mechanism. Giant redemptions can pressure issuers to lean on money buffers or promote short-dated bonds.

The paper fashions how liquidity and capital thresholds can scale back default and spillover dangers once they work as usable buffers, whereas inflexible guidelines can even push issuers into bond gross sales too early throughout stress.

| Stablecoin channel | Market hyperlink | Coverage sign |

|---|---|---|

| New inflows | Extra demand for short-term Treasuries or repo | BIS estimates influx shocks can compress front-end yields the place issuer reserves are invested |

| Redemptions | Money use or bond gross sales | BIS fashions present buffers can scale back spillovers, however threshold design can form stress transmission |

| Overseas demand | Digital greenback entry and FX conversion | BIS analysis hyperlinks internet stablecoin-flow shocks to parity gaps, native currencies and greenback funding premiums |

| Official tokenization | Tokenized deposits and central financial institution reserves | BIS tasks are testing supervised settlement rails contained in the two-tier financial system |

Separate BIS analysis on stablecoin flows and FX markets extends the purpose past T-bills. It finds that shocks to internet stablecoin inflows can widen deviations from stablecoin-dollar parity, have an effect on native foreign money values, and alter short-term greenback funding premiums.

The discovering stops in need of turning each stablecoin switch right into a macro occasion. It exhibits why central banks are finding out these flows as a part of greenback and FX plumbing.

Scale makes the spillover query more durable to disregard

CryptoSlate market knowledge on June 26 confirmed Tether with a market capitalization of about $186.08 billion and a 24-hour buying and selling quantity of about $84.95 billion. USDC stood at a market cap of almost $73.68 billion and a each day buying and selling quantity of $15.54 billion.

Collectively, the 2 largest dollar-stablecoins represented roughly $259.76 billion in market worth and greater than $100 billion in each day buying and selling quantity. Stablecoins stay far smaller than the Treasury market, however their reserve portfolios are concentrated in money, repo, cash funds, and short-duration authorities debt.

The US and European coverage backdrop helps clarify why the reserve query is arriving now. The White Home framed the GENIUS Act round 100% liquid backing, month-to-month reserve disclosures, and the concept regulated stablecoins might help demand for Treasuries and the greenback.

That may be a coverage declare, reasonably than a market certainty, nevertheless it explains why reserve composition has turn into central.

Europe is asking the same query from the opposite facet. The European Fee opened a 2026 overview of MiCA’s crypto-asset framework, together with asset-referenced and e-money tokens.

The ECB has additionally argued that stablecoins have moved to the middle of the coverage debate as dollar-denominated tokens elevate questions on financial sovereignty and sovereign bond demand.

The stay problem is the type of monetary establishment issuers turn into as soon as regulation pushes them towards particular reserve belongings, disclosures, redemption guidelines, and supervisory reporting.

That coverage combine leaves central banks with a more durable activity than approving or rejecting a product class. Reserve guidelines can enhance disclosure, liquidity self-discipline, and redemption confidence, but they’ll additionally make issuer portfolios simpler to learn as massive funding-market positions.

A regulated stablecoin issuer that buys payments in measurement throughout development and sells or runs down liquid belongings throughout stress is greater than a fee firm in market phrases. It’s also a stability sheet whose flows can work together with the devices used to transmit greenback liquidity.

Tokenized financial institution cash is the official various

The chapter’s most popular path is to combine tokenized finance into the present two-tier financial system, wherein central financial institution cash anchors settlement and controlled non-public establishments present companies to customers.

That’s the place Undertaking Agora suits. The BIS Innovation Hub challenge brings collectively central banks and greater than 40 regulated monetary establishments to check wholesale cross-border funds utilizing tokenized business financial institution deposits and tokenized central financial institution reserves on a shared platform.

In a Could 27 announcement, BIS stated the challenge has already proven that atomic multi-currency settlement might be executed utilizing tokenized deposits and central financial institution reserves whereas preserving the authorized character of these devices.

The subsequent section is meant to maneuver towards real-value testing.

That’s the institutional reply to the stablecoin query. Personal stablecoins have proven that customers need programmable greenback devices that transfer throughout digital venues. Central banks at the moment are testing whether or not the identical capabilities might be delivered via tokenized deposits and central financial institution settlement belongings with out shedding the safeguards that earn a living work beneath stress.

For crypto markets, the consequence reaches past tighter stablecoin regulation. If issuers are massive reserve managers, then inflows, redemptions, and asset allocation turn into funding-market indicators.

If tokenized deposits achieve traction, stablecoins face competitors from a mannequin that gives programmability with out leaving the banking and central-bank settlement perimeter.

The subsequent factor to observe is whether or not stablecoin development comes primarily from new offshore demand for digital {dollars} or from balances that might in any other case sit in banks and cash funds.

The primary path might deepen demand for short-end greenback belongings whereas extending the greenback’s attain. The second might make redemptions, reserve gross sales, and bank-funding shifts extra necessary in stress.

Both approach, the controversy has moved. Stablecoins are nonetheless fee tokens for customers and liquidity rails for crypto venues. They’re additionally changing into a part of the equipment via which greenback demand reaches sovereign debt markets.

That’s the reason central banks are treating them as greater than crypto plumbing.