In conventional markets, the VIX offers merchants a strategy to hedge or commerce anticipated stock-market volatility relatively than take a direct view on the S&P 500. CME Bitcoin volatility futures now give Bitcoin merchants a regulated model of that concept: a strategy to wager on volatility with out betting on Bitcoin’s value.

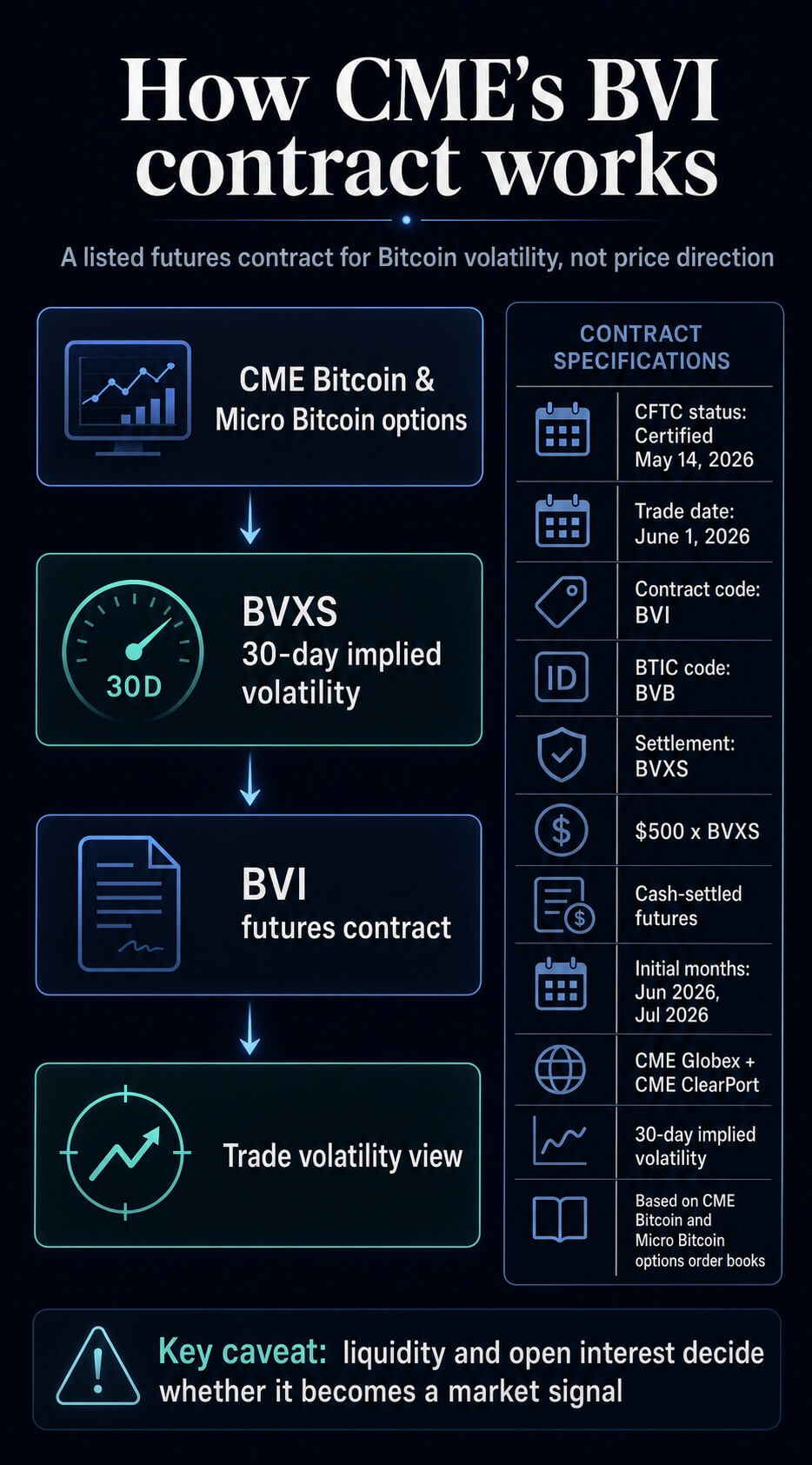

The alternate plans to checklist Bitcoin Volatility futures to start out buying and selling on June 1, whereas a Might 14 Commodity Futures Buying and selling Fee product document lists the contract as Licensed.

That makes the launch a market-structure check: whether or not Bitcoin is prepared for a regulated futures contract tied to anticipated turbulence itself.

The contract, ticker BVI, will settle financially to the CME CF Bitcoin Volatility Index – Settlement, or BVXS. The index is designed to mirror a 30-day ahead view of implied volatility drawn from CME Bitcoin and Micro Bitcoin choices order books.

In sensible phrases, a buying and selling desk can specific whether or not it expects Bitcoin’s subsequent month to be calmer or extra risky with out utilizing Bitcoin futures, spot ETFs, or choices to take a direct value view.

The product carries a VIX-style really feel, nevertheless it doesn’t make BVI a confirmed Bitcoin concern gauge earlier than buying and selling begins. It places a regulated contract round one thing merchants already watch: how a lot motion the market expects from Bitcoin, impartial of whether or not the following transfer is larger or decrease.

The VIX grew to become essential in conventional finance as a result of it turned anticipated volatility into a standard threat language. Portfolio managers use it to hedge shocks, choices desks use it to cost stress, and analysts use it as a shorthand for market concern. BVI is trying to deliver the same layer to Bitcoin, nevertheless it nonetheless has to show that merchants will use it in measurement.

CME’s new contract shifts the commerce away from value route

The certification element updates CME’s Might 5 launch announcement with out altering the fundamental timeline. The contract moved from deliberate pending regulatory evaluation within the announcement to a CFTC product document marked Licensed.

CME’s corresponding Might 14 submitting says the contract might be accessible on CME Globex and CME ClearPort from Sunday, Might 31, forward of the June 1 buying and selling session.

The certification is a list milestone: CME has licensed the contract underneath the related CFTC course of, whereas regulatory endorsement and future liquidity stay separate questions.

It offers institutional desks a well-known alternate and clearing framework for a Bitcoin volatility commerce.

For many readers, the important thing phrases are easier: BVI is the futures contract, BVXS is the index it settles to, and every contract is price $500 instances the BVXS degree.

The preliminary listed months are June 2026 and July 2026.

The sensible distinction is publicity. Bitcoin futures let merchants take a view on the place BTC will commerce. Bitcoin ETFs give buyers spot-linked publicity inside brokerage accounts.

Bitcoin choices can specific each value and volatility views, however they require choices execution and options-risk administration. BVI packages a volatility view right into a listed futures contract that rises or falls with the market’s expectation for Bitcoin motion relatively than with Bitcoin’s spot value alone.

CME’s product web page makes that distinction specific, saying the contract is supposed for hedging Bitcoin publicity in opposition to rising or falling volatility and for buying and selling expectations of market turbulence impartial of Bitcoin’s value route.

BVXS turns choices costs into the reference level

The futures contract is barely as helpful because the benchmark beneath it. BVXS is the each day settlement model of the CME CF Bitcoin Volatility Index.

CF Benchmarks describes BVXS as a once-a-day benchmark representing a forward-looking, 30-day constant-maturity implied volatility measure primarily based on CME Bitcoin and Micro Bitcoin choices order books.

In follow, the Bitcoin volatility index converts CME choices pricing right into a each day reference level for anticipated BTC turbulence.

BVXS doesn’t monitor Bitcoin itself. It tracks what choices costs suggest about how a lot Bitcoin might transfer over the following 30 days. That makes BVXS a Bitcoin implied volatility benchmark relatively than a spot-price benchmark.

If choices merchants value in additional uncertainty, the index can rise even earlier than Bitcoin makes a big transfer. If choices merchants demand much less safety or anticipate calmer buying and selling, the index can fall even whereas Bitcoin stays directionally energetic.

That distinction makes the product greater than one other entry rail. A fund that owns Bitcoin publicity via spot holdings, ETFs, futures, or structured merchandise might not need to promote the underlying publicity each time market stress rises.

It might as an alternative desire a device that targets volatility immediately. Conversely, a dealer might anticipate turbulence round a macro print, regulatory occasion, ETF-flow reversal, or market dislocation with out having conviction on whether or not BTC breaks larger or decrease.

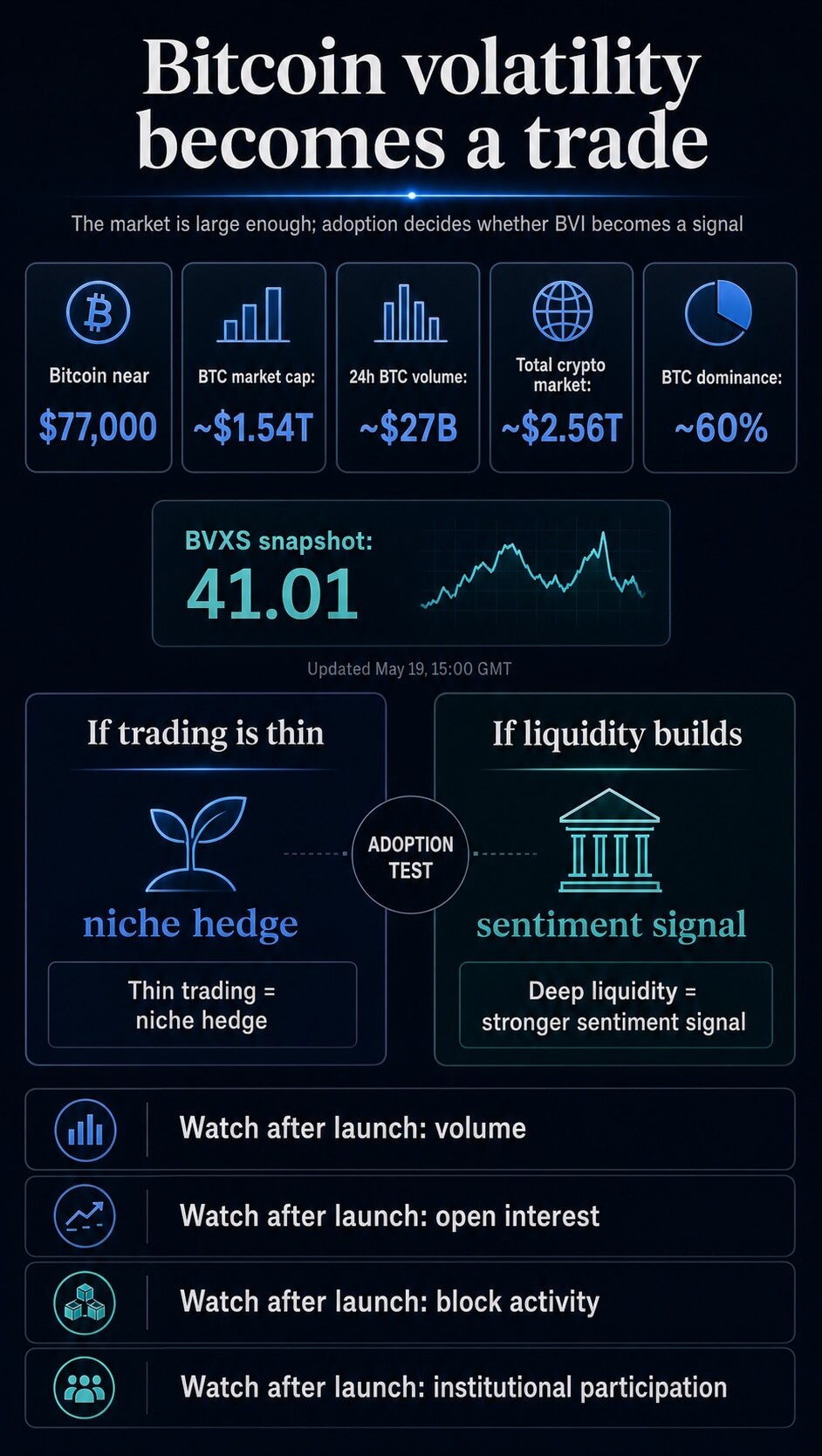

As of publication on Might 20, the newest CF Benchmarks determine accessible earlier than the session confirmed BVXS at 41.01, down 0.99%.

Bitcoin now has a CME-linked implied-volatility benchmark sitting underneath a listed futures product.

Why establishments might care a couple of Bitcoin concern commerce

For establishments, BVI provides a less complicated strategy to separate a commerce that Bitcoin futures, choices, and ETFs typically combine collectively.

In a directional product, the dealer is normally uncovered to Bitcoin’s degree. A protracted Bitcoin futures place advantages if BTC rises and loses if it falls. A spot ETF holder is tied to the asset’s route.

Choices can isolate volatility, however the commerce is extra advanced and carries publicity to strike choice, expiry, time decay, and place administration.

BVI offers desks a cleaner listed expression of the query: will Bitcoin transfer roughly than the market at present expects?

That may assist desks hedge portfolios, value structured merchandise, handle choices books, or place round occasions the place the scale of the transfer issues greater than the route.

The timing additionally matches CME’s broader crypto market-structure push. CME says 24/7 cryptocurrency futures and choices buying and selling is scheduled to start Might 29, shortly earlier than the BVI launch. It additionally extends CME’s Bitcoin derivatives stack past directional futures, choices, and ETF-adjacent market publicity.

The 2 developments level in the identical route: regulated crypto derivatives have gotten much less like a facet session connected to conventional market hours and extra like infrastructure designed round how crypto really trades.

CryptoSlate’s latest Bitcoin protection has largely adopted the directional and entry questions which have dominated the market: ETF-flow reversals, inflation stress, choices liquidity round spot ETF merchandise, institutional accumulation, and the fading economics of some retail ATM fashions.

CME’s volatility contract strikes the dialogue into a special layer. It asks whether or not Bitcoin’s threat can turn into a product in its personal proper.

Bitcoin’s scale makes the query significant. CryptoSlate’s market pages confirmed Bitcoin close to $77,000 on Might 20, with a market capitalization round $1.54 trillion and 24-hour quantity round $27 billion.

The broader crypto market stood round $2.56 trillion, with BTC dominance close to 60%. In that context, a regulated volatility future is an try to make the market’s expectation of Bitcoin motion tradable in a extra direct type.

The launch check is liquidity, not branding

Evaluating CME BVI futures to the VIX can, nonetheless, overstate the product earlier than buying and selling information exists.

VIX futures and choices are established devices for buying and selling or hedging volatility threat. BVI has not earned that standing but.

The check after June 1 might be sensible: whether or not the contract attracts quantity, open curiosity, block exercise, and sufficient institutional participation to turn into a significant sign.

CME’s submitting says buying and selling volumes, open curiosity ranges, and value info might be revealed each day. These figures will carry extra weight than the launch label.

If quantity builds, BVI might give market individuals a cleaner strategy to hedge Bitcoin publicity once they anticipate turbulence, or to precise a view that anticipated volatility is just too excessive or too low.

It might additionally give analysts one other sign on market stress alongside ETF flows, choices positioning, futures foundation, and spot liquidity.

If buying and selling is skinny, the product might stay helpful for some desks with out changing into a broad sentiment gauge. That consequence would nonetheless add a regulated device to the Bitcoin derivatives stack, however it could fall wanting turning Bitcoin volatility right into a broadly adopted market instrument.

CME has a CFTC-certified Bitcoin Volatility futures contract scheduled for June 1, tied to a 30-day implied-volatility benchmark constructed from CME Bitcoin choices information.

It offers establishments a strategy to commerce Bitcoin’s anticipated turbulence with out making a direct value wager. Whether or not it turns into Bitcoin’s concern commerce relies on what occurs as soon as merchants can really use it.