The SEC moved the crypto market construction ahead on Apr. 13 with out ready for Congress to behave.

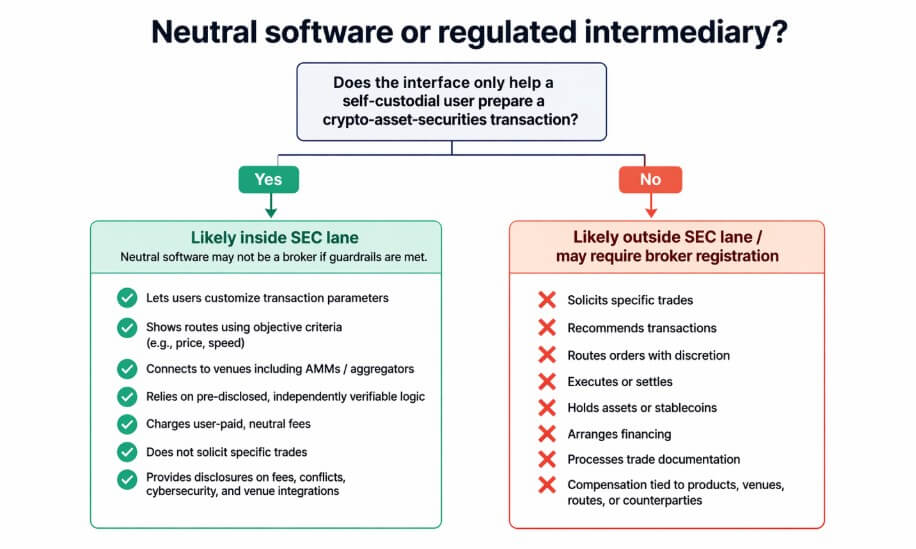

The company’s Division of Buying and selling and Markets revealed a employees assertion on Lined Person Interfaces, reminiscent of web sites, browser extensions, wallet-linked apps, and cellular functions that assist customers in self-custodial setups put together transactions in crypto asset securities.

Employees mentioned it is not going to object to those suppliers working with out broker-dealer registration below Alternate Act Part 15, offered they keep inside a strict set of behavioral and disclosure guardrails.

That framing of the conditional, slender, and intentionally provisional displays that the SEC is much sufficient into its personal regulatory program to sketch working situations for an on-chain securities stack, but nonetheless depending on Congress for something that lasts.

What the assertion really does

A Lined Person Interface Supplier qualifies if it permits customers to customise transaction parameters, avoids soliciting particular trades, depends on pre-disclosed and independently verifiable routing logic, and presents execution choices based mostly on goal elements reminiscent of worth or velocity, amongst others.

The assertion expressly consists of distributed ledger buying and selling techniques, reminiscent of automated market maker (AMM) liquidity swimming pools and liquidity aggregators, as venues to which these interfaces could join.

That’s the first time the SEC has described, with any operational specificity, how a self-custodial interface layer for crypto asset securities might operate whereas staying outdoors dealer standing.

For tokenized securities builders, the working image that emerges is a intentionally skinny stack consisting of software program that helps customers categorical preferences, examine routes, evaluate costs and gasoline prices, and signal by way of a self-custodial pockets.

The doc attracts the periphery at something that appears like intermediation, reminiscent of no suggestions, no discretionary order routing, no execution, no custody of funds or stablecoins, no settlement, no financing preparations, and no soliciting particular trades.

The place the lane ends

Any interface that negotiates transaction phrases, holds person property, executes or settles transactions, arranges financing, conducts impartial valuations, or processes commerce documentation falls outdoors the scope of the assertion.

Compensation tied to particular merchandise, venues, routes, or counterparties additionally disqualifies a supplier.

The SEC’s permitted zone covers goal route show and user-directed parameter settings. Something involving execution, routing discretion, or custody requalifies a supplier as a dealer.

The assertion explicitly identified that an middleman enterprise mannequin requires dealer registration, no matter whether or not the pockets is self-custodial. Its scope ends on the interface layer, leaving full-service DeFi merchandise fully outdoors its protection.

Protocols that maintain property in good contracts, execute swaps on behalf of customers, or bundle routing with custody are intermediaries in a distinct regulatory class.

The aid is restricted to a product form, with the broader on-chain buying and selling financial system outdoors the assertion’s scope.

A 3-part SEC marketing campaign

The Apr. 13 assertion is the third in a deliberate sequence. On Jan. 30, the SEC revealed an announcement on tokenized securities, framing it as a part of a broader effort to make clear how federal securities legal guidelines apply to crypto property.

On Mar. 17, the company described its interpretive work on crypto asset regulation as a significant step towards readability, complementing Congress’s market construction work.

Commissioner Hester Peirce and Buying and selling and Markets Director Jamie Selway each described the Apr. 13 launch as incremental infrastructure for tokenized securities and crypto market construction.

In February, Chairman Paul Atkins and Peirce mentioned employees have been engaged on an exemption for restricted buying and selling of sure tokenized securities on novel platforms, together with AMMs. Peirce later mentioned the exemption into account could be slender.

The markets these guidelines deal with already carry actual quantity. RWA.xyz at present exhibits $29.3 billion in distributed real-world property, over $1 billion in tokenized public equities and ETFs, and $13.4 billion in tokenized US Treasuries.

DTCC has mentioned DTC is making ready a tokenization service for the second half of 2026. The SEC is sketching guidelines for a market that already has customers and switch exercise.

Two futures for product design

The bull case runs by way of the narrower exemption arriving earlier than the legislative window closes.

If the SEC follows the Apr. 13 impartial interface assertion with a bounded AMM pilot that caps, allowlists, and governs on-chain tokenized securities buying and selling alongside the traces Atkins described, on-chain tokenized securities buying and selling turns into operational inside a bounded regulatory field.

Builders who designed their interfaces across the impartial software program customary would have infrastructure in place when the exemption lands. The payoff is an on-chain securities stack that’s purposeful, if constrained, earlier than Congress finalizes a broader statute.

The bear case is product paralysis on the product edge. As a result of the assertion carries no authorized power, creates no enforceable rights, and expires in 5 years absent Fee motion, counsel at cautious organizations could deal with the Apr. 13 lane as too fragile for something formidable. Interfaces keep informational or routing-light.

Severe tokenized securities buying and selling concentrates in incumbent-led, permissioned pilots, reminiscent of DTCC’s tokenization service, large-bank packages, and comparable constructions constructed round registered entities, whereas the product architectures the assertion aimed to allow get deferred indefinitely.

The congressional variable

The doc’s personal disclaimer conveys the fragility as employees views solely, with out authorized power or impact, and wanting the Fee’s motion that may give it sturdiness.

Senate Banking introduced a crypto market construction markup in January and postponed it as bipartisan talks continued. As of Apr. 15, no new public markup date seems in committee supplies.

Treasury Secretary Scott Bessent urged Congress to cross the CLARITY Act on Apr. 9.

All three knowledge factors converge on the identical conclusion: solely a statute can hold a lane open established by the SEC.

Galaxy Analysis and the Blockchain Affiliation pressed the SEC on Apr. 14 for conditional AMM aid, whereas SIFMA argued new on-chain buying and selling constructions ought to proceed below sturdy rulemaking with comparable investor-protection requirements.

That three-way cut up between company employees, crypto-native business, and incumbent monetary infrastructure is exactly the configuration that makes Congressional decision obligatory and politically troublesome.

| Stakeholder | What they need | Why it issues |

|---|---|---|

| SEC employees | Slender working room below present authority | Lets elements of the market transfer now with out ready for Congress |

| Crypto-native business | Conditional AMM aid and workable tokenized-securities rails | Needs actual product deployment earlier than laws is completed |

| Incumbent monetary infrastructure / SIFMA | Sturdy rulemaking and comparable investor-protection requirements | Pushes for permanence, predictability, and conventional safeguards |

| Congress | A statutory market-structure framework | Solely path to sturdy, non-reversible readability |

Chairman Atkins has constantly framed Challenge Crypto as a complement to legislative work. The Apr. 13 assertion is the clearest expression of that posture, being actual sufficient to construct round now, and contingent sufficient to require one thing extra sturdy.