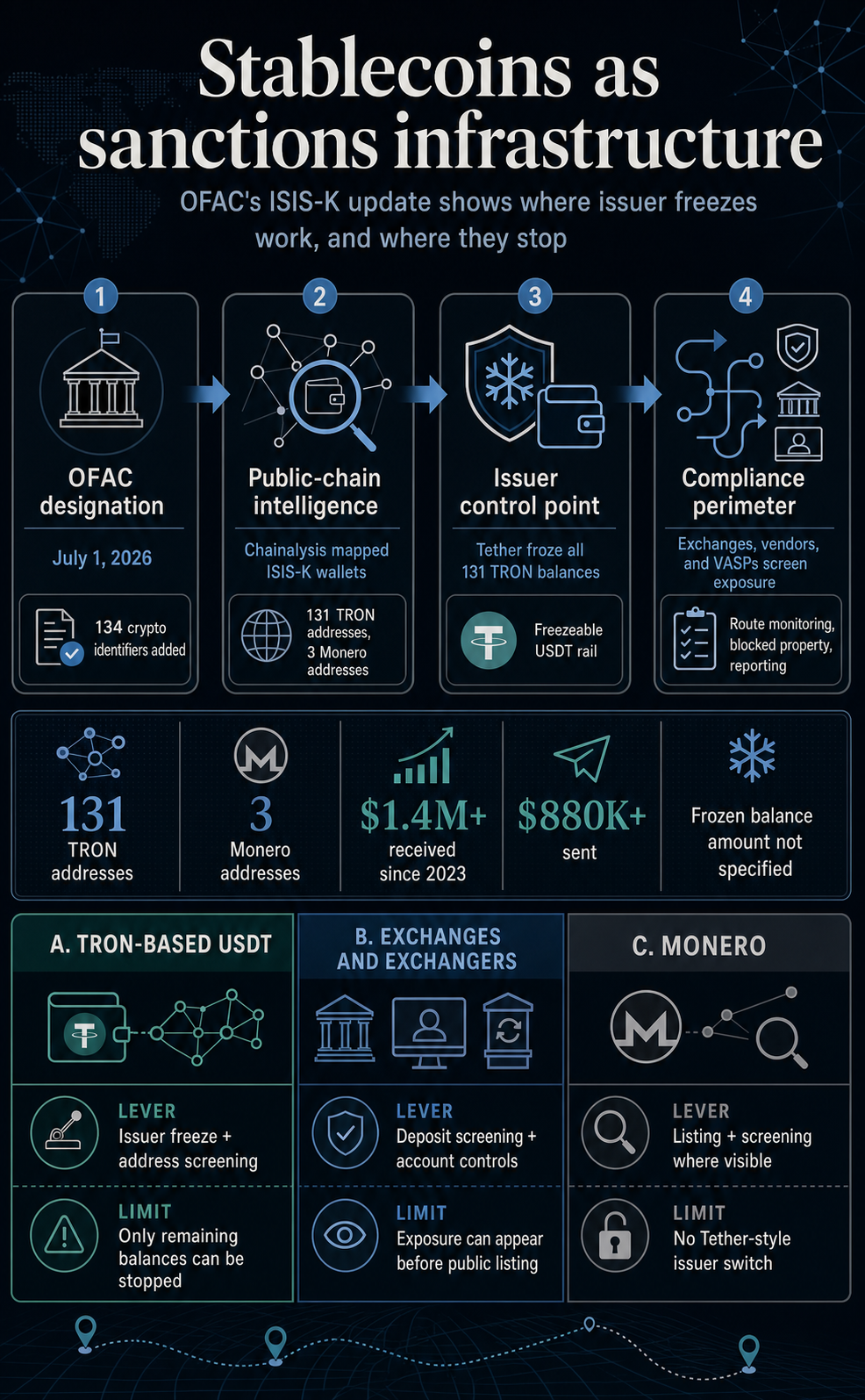

ISIS-Ok, the Islamic State affiliate lively throughout Afghanistan, Pakistan, and elements of Central Asia, had USDT balances frozen on 131 TRON addresses after an OFAC sanctions replace, creating an enforcement check for stablecoins. As soon as public-chain intelligence, a sanctions checklist, and issuer controls had been in place, Tether might freeze the balances inside its personal token system.

The July 1 motion up to date the ISIL Khorasan designation with digital-currency identifiers. Chainalysis mentioned OFAC added 134 crypto addresses, together with 131 TRON addresses and three Monero addresses.

It additionally mentioned Tether froze the balances on all 131 TRON addresses.

The end result turns a sanctions entry right into a map of who can cease the move of cash. Governments determine a goal; blockchain intelligence maps the wallets; exchanges and compliance distributors display screen for publicity; and a freezeable issuer can interrupt balances inside its token system.

Chainalysis mentioned the 131 TRON wallets managed by ISIS-Ok had obtained greater than $1.4 million since 2023 and despatched greater than $880,000. These figures don’t present how a lot remained within the wallets when Tether froze them, and so they shouldn’t be handled because the frozen steadiness.

However the move totals present the enforcement mannequin in motion. The wallets had been greater than symbolic identifiers on an inventory. They had been a part of an on-chain funding route that touched mainstream providers and may very well be screened after designation.

Stablecoin sanctions now have an issuer swap

OFAC has handled digital-currency addresses as sanctions identifiers for years, however stablecoins add a management level that doesn’t exist in the identical approach for each crypto asset.

OFAC’s virtual-currency steering says it might add digital-currency addresses to the SDN Checklist and that events figuring out blocked digital forex ought to block the property and report related info.

For an trade, custodian, fee agency, or compliance vendor, meaning screening the listed addresses and associated publicity. For a stablecoin issuer, it could actually additionally imply disabling the token steadiness on the contract or issuer-control layer.

Tether had already moved towards that posture. In December 2023, the corporate mentioned it had launched a voluntary wallet-freezing coverage for exercise associated to people on OFAC’s SDN Checklist.

The ISIS-Ok case reveals what that coverage means in observe when the asset sits on a clear chain with a big USDT footprint.

The result’s a unique type of sanctions perimeter. Conventional sanctions typically work by way of banks, correspondent accounts, fee processors, and custodians. On this mannequin, the stablecoin issuer sits nearer to the asset itself.

If a listed handle holds a freezeable token, the enforcement pathway can run by way of the issuer fairly than relying solely on exchanges to reject deposits or withdrawals.

That doesn’t make the system automated or full. It nonetheless will depend on well timed intelligence, correct labeling, authorized course of, operational capability, and the issuer’s willingness or obligation to behave.

It additionally raises onerous questions on personal firms changing into choke factors for dollar-linked tokens that flow into globally. However the ISIS-Ok replace reveals that the issuer function is not theoretical.

That is the coverage rigidity stablecoin issuers now carry. The identical management that lets an issuer reply to a sanctions designation can grow to be a standing expectation from regulators, legislation enforcement, exchanges, and analytics companies.

As soon as that expectation exists, a greenback token is judged by greater than reserve high quality, liquidity, and redemption entry. Additionally it is judged by how briskly its issuer can act when a listed pockets seems on-chain.

TRON-based USDT sits on the middle of the case

The TRON handle depend is the element that provides the motion its form. Chainalysis mentioned the ISIS-Ok replace included 131 TRON addresses, in contrast with three Monero addresses.

Tether’s freeze utilized to the TRON aspect as a result of these balances had been in a token system the issuer can management.

That element impacts exchanges and fee companies as a result of TRON-based USDT has grow to be a standard rail for quick, low cost greenback transfers. When a sanctions motion names TRON addresses, the compliance burden doesn’t cease on the listed wallets.

Corporations must ask whether or not they obtained funds from these addresses, despatched funds to them, interacted with associated clusters, or served prospects by way of adjoining cash-out routes.

Chainalysis mentioned a number of of the designated wallets despatched funds to Syria-based crypto exchangers and had heavy publicity to mainstream providers. That’s the place stablecoin sanctions grow to be infrastructure fairly than paperwork.

The listed handle is the start line. The true work is mapping counterparties, deposits, withdrawals, service publicity, and any linked addresses that will not but be public.

Tether’s latest historical past reinforces that development. In April, the corporate mentioned it supported freezing greater than $344 million in USDT in coordination with OFAC and U.S. legislation enforcement.

In Could, it mentioned the T3 Monetary Crime Unit involving Tether, TRON, and TRM Labs had frozen greater than $450 million tied to illicit crypto flows.

These are separate actions from the ISIS-Ok replace, however they present a repeatable sample: analytics determine threat, public or personal enforcement channels flag wallets, and the issuer freeze turns into a part of the response.

The coverage backdrop is transferring in the identical course. In an April proposed rule, FinCEN and OFAC set out AML/CFT and sanctions compliance necessities for permitted fee stablecoin issuers, together with technical capacities to dam, freeze, and reject impermissible transactions.

Regulators more and more deal with stablecoin issuers as monetary infrastructure with compliance duties, not simply software-adjacent token firms.

| Rail | Enforcement lever | Restrict |

|---|---|---|

| TRON-based USDT | Issuer freeze, handle screening, trade monitoring | Solely remaining token balances may be frozen; prior flows nonetheless require tracing |

| Centralized exchanges and exchangers | Account controls, deposit screening, withdrawal blocks, reporting | Publicity could seem earlier than a public designation or by way of intermediaries |

| Monero and different non-issuer belongings | Sanctions itemizing, screening, investigative tracing the place potential | No Tether-style issuer management level for freezing balances |

The Monero addresses present the place the mannequin stops

The identical OFAC replace additionally included three Monero addresses. That distinction is necessary as a result of it reveals the restrict of issuer-driven enforcement.

Monero accounts are managed by way of personal keys, not by a centralized issuer that may disable a token steadiness. OFAC can checklist an XMR handle, and exchanges or different lined companies can display screen for publicity the place they’ve visibility.

Investigators can nonetheless pursue leads, counterparties, gadgets, service suppliers, and consumer errors. However there isn’t any equal of asking Tether to freeze a USDT steadiness on the issuer layer.

That cut up is more likely to form conduct. If stablecoin freezes grow to be quicker and extra routine, sanctioned actors and illicit networks have incentives to shift funds towards belongings or routes with fewer issuer controls.

That doesn’t make these routes secure or invisible. It does make them tougher to interrupt at a single company management level.

For governments, the enchantment of freezeable stablecoins is apparent. Public chains go away trails. Stablecoins typically contact centralized providers. Issuers can act like fee processors or banks when authorized and operational situations are met.

The result’s a sanctions instrument that may transfer quicker than conventional cross-border finance in some instances.

For crypto customers and infrastructure suppliers, the tradeoff is simply as clear. The identical function that lets an issuer cease funds tied to a sanctioned terrorist group additionally confirms that tokenized {dollars} carry centralized management.

That could be acceptable, even anticipated, for regulated fee stablecoins. It additionally marks a dividing line between belongings designed to behave like compliant money-market infrastructure and belongings designed to attenuate third-party management.

That dividing line provides the ISIS-Ok motion its forward-looking edge. The enforcement achieve is strongest when illicit finance makes use of tokenized {dollars} on public chains.

The motivation to adapt is strongest when these actors can transfer into belongings or venues the place the issuer swap is absent, visibility is weaker, or cash-out factors sit exterior cooperative channels.

The subsequent battle is over the route, not the pockets

The ISIS-Ok replace factors to the following section of crypto sanctions: enforcement will focus much less on a single pockets and extra on the route round it.

A listed handle may be frozen if it holds issuer-controlled stablecoins. It may be screened by exchanges and custodians. Its counterparties may be mapped by analytics companies.

However the funding community can nonetheless adapt by transferring by way of new addresses, unlisted intermediaries, offshore exchangers, privateness instruments, or belongings with out issuer controls.

The OFAC and Chainalysis document goes past Tether freezing 131 wallets. Stablecoin rails have gotten a part of a standing enforcement stack.

The stack consists of sanctions lists, blockchain intelligence, issuer controls, trade compliance, and vendor tooling. Every half covers a unique piece of the route.

The ISIS-Ok case additionally reveals the mannequin’s built-in limitation. Freezeable stablecoins are highly effective when illicit finance makes use of tokenized {dollars} on clear chains.

They’re much less decisive when funds have already moved, when balances are gone, when counterparties sit exterior cooperative venues, or when exercise shifts to belongings with no centralized issuer.

For stablecoin issuers, the message is that scale now comes with enforcement expectations. For exchanges, the stress is to detect publicity earlier than a listed pockets arrives on the deposit web page.

For compliance distributors, the worth is in turning public designations into real-time routing maps. For customers, the case is a reminder that probably the most liquid on-chain {dollars} usually are not impartial pipes. They’re programmable balances inside programs that may be stopped.

The subsequent sign might be whether or not actions like this stay case-by-case responses or grow to be a standard working layer for greenback stablecoins.

If issuer freezes, trade screening, and chain analytics proceed to converge, stablecoins will do extra than simply transfer {dollars} on public chains. They are going to assist determine which on-chain {dollars} can hold transferring.