Stablecoins have moved from a crypto-policy-side market to Kevin Warsh’s Federal Reserve’s dollar-policy agenda.

Fed Governor Christopher Waller used the central financial institution’s June 22 greenback convention to border digital belongings, together with stablecoins, as a part of the analysis agenda across the greenback’s worldwide position.

The remarks had been a analysis sign quite than a brand new stablecoin coverage. They modified the context: stablecoin flows now sit alongside greenback funding, cost rails, cross-border capital motion, safe-asset demand, and the query of how personal token issuers contact public greenback infrastructure.

That reframes the market. Greenback-backed stablecoins are nonetheless crypto buying and selling instruments, cost tokens, and regulatory objects. The Fed’s greenback agenda now treats them as a attainable transmission channel too.

Waller’s remarks and the Fed’s convention agenda place them inside a bigger system: personal digital-dollar claims that may transfer throughout exchanges, wallets, issuers, banks, and reserve portfolios, whereas nonetheless counting on the U.S. greenback and the short-term belongings backing it.

The cheap query is what adjustments if these issuers develop into one of many channels by means of which international demand for {dollars} reaches the banking system and the Treasury market.

The Fed is treating stablecoins as greenback rails

Waller’s welcoming remarks on the Fifth Convention on the Worldwide Roles of the Greenback described distributed-ledger applied sciences and tokenized belongings, together with stablecoins, as creating channels for international greenback intermediation alongside, or in reference to, conventional banks and cost techniques.

The convention agenda clarifies the coverage body. The Fed and the New York Fed organized the June 22-23 occasion round monetary innovation, digital belongings, the greenback’s roles in funding and funds, market construction, reserve-currency standing, digital fragmentation, and geopolitics.

Stablecoins sit inside that wider digital-dollar analysis map, alongside different digital-asset and market-structure questions.

The greenback’s position is often mentioned when it comes to banks, Treasury markets, overseas reserves, commerce invoicing, and offshore funding. Stablecoins add a non-public expertise layer to that map.

A consumer exterior the US can maintain a dollar-denominated token, transfer it throughout blockchains, commerce it towards different belongings, or redeem it by means of an issuer whereas interacting with the greenback system another way from a financial institution depositor or money-market-fund investor.

The result’s a extra difficult type of greenback entry. Stablecoins can prolong greenback attain by making greenback claims simpler to carry and switch.

They’ll additionally pull personal issuers into coverage debates as soon as reserve administration, redemptions, liquidity shocks, or offshore demand develop into massive sufficient to have an effect on different markets.

For this reason scale adjustments the coverage drawback. Stablecoins stay small in contrast with the total Treasury market, but they’re already massive inside crypto.

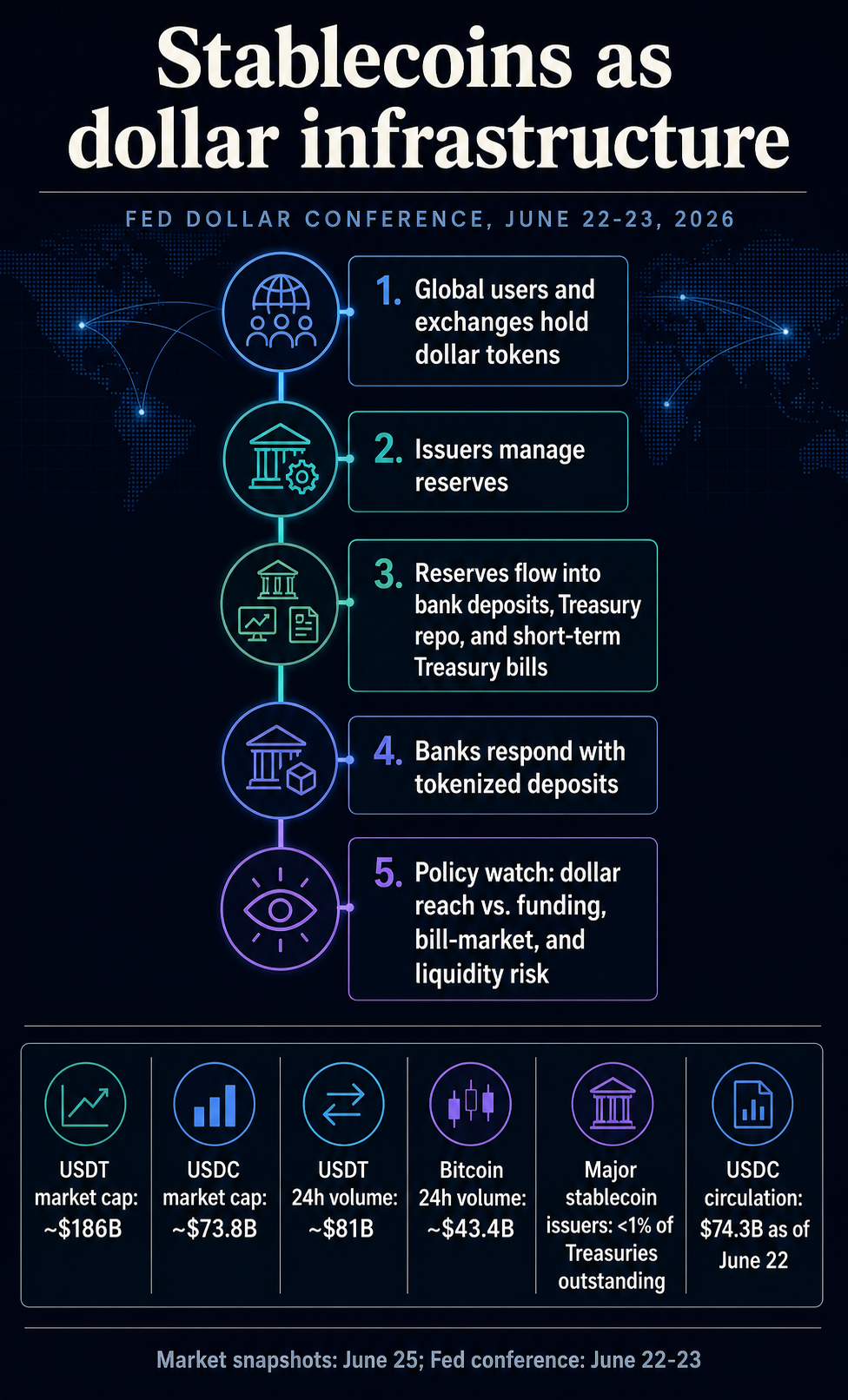

CryptoSlate market information confirmed Tether and USDC among the many 5 largest crypto belongings by market capitalization, with USDT at almost $186 billion and USDC at almost $73.8 billion on June 25.

Tether’s 24-hour quantity alone was round $81 billion, almost double Bitcoin‘s roughly $43 billion in the identical market view.

These figures are just one cut-off date. The bigger level is that greenback tokens now have sufficient scale and turnover to immediate central-bank researchers to ask the place the {dollars} behind them come from, the place reserves are held, what occurs throughout redemptions, and whether or not the flows create strain in locations that had been beforehand studied largely by means of banks and cash funds.

Circle’s personal supplies put USDC in circulation at $74.3 billion as of June 22 and describe the token as backed by extremely liquid money and cash-equivalent belongings. Circle additionally says many of the reserve is held within the Circle Reserve Fund, an SEC-registered authorities cash market fund managed by BlackRock.

That sort of construction turns a cost token right into a reserve-management channel. A change in stablecoin demand can change demand for financial institution deposits, Treasury repo, or short-term Treasury payments, relying on how the issuer manages backing belongings.

The dollar-policy narrative, subsequently, goes past one-to-one redemption. The coverage difficulty is whether or not sufficient personal tokens, backed by enough short-term greenback belongings, may be built-in into the distribution and absorption of greenback liquidity.

Stablecoins compete for each funds and balances

Fed employees analysis has already begun to separate potential financial institution results from the less complicated declare that stablecoins drain deposits. A Could FEDS Be aware stated stablecoins are notable as a result of they mix balance-holding and cost performance on digital rails, which means they compete for each transaction balances and cost flows.

A separate Fed observe from December described the deposit impression as conditional. Stablecoin progress could scale back, recycle, or restructure financial institution deposits relying on who calls for the tokens, what belongings they convert, and the way issuers maintain reserves.

Home customers shifting transaction balances out of banks would have one impact. Offshore customers searching for digital {dollars} may have one other.

Issuers parking reserves in banks, cash funds, repo, or payments would transmit the expansion by means of completely different components of the monetary system.

Banks are actually a part of the response. The Clearing Home introduced on June 5 that main monetary establishments are backing an on-chain commercial-bank-money initiative to assist tokenized deposit clearing and settlement whereas connecting blockchain exercise to RTP and CHIPS.

The announcement reveals the path of the financial institution response: hold digital cash motion inside regulated commercial-bank cash as stablecoins construct always-on greenback rails.

A 2026 New York Fed employees analysis report argued that stablecoin exercise can transmit liquidity stress to banks and complicate monetary-policy implementation.

That’s not an official coverage assertion, nevertheless it factors to the identical difficulty Waller’s convention framing raised: as soon as stablecoins work together with banks, reserves, and wholesale funds, their results can leak out of crypto markets.

The strongest macro hyperlink is short-term safe-asset demand. A June BIS working paper discovered that dollar-backed stablecoin inflows can decrease short-term Treasury invoice yields, with results that intensify throughout Treasury market stress and because the sector grows.

The paper’s discovering is pretty particular: it describes yield compression from inflows at quick tenors, with no declare in regards to the full Treasury curve.

Treasury advisory supplies add the size test. A 2026 Treasury Borrowing Advisory Committee presentation discovered that main stablecoin issuers maintain lower than 1% of excellent Treasuries.

The identical presentation additionally stated stablecoins may enhance demand for short-end Treasury issuance if future progress comes from new offshore greenback demand. That mixture is the stress policymakers have to trace.

In the present day, stablecoins may be small relative to the total Treasury market and nonetheless have an effect on payments and repo on the margin.

On a bigger scale, their reserve portfolios may develop into one other supply of demand for the most secure and most liquid greenback belongings. Throughout stress, redemptions may work within the different path.

The dollar-reinforcement argument depends upon this channel. If greenback stablecoins proceed to unfold overseas, they will broaden entry to greenback devices with out requiring a overseas consumer to have a U.S. checking account.

However that additionally means personal issuers and reserve managers develop into a part of the distribution system for greenback liquidity. The extra profitable the mannequin turns into, the more durable it’s to deal with it as a crypto facet market.

The following sign is how the system absorbs them

The Fed’s June convention leaves open whether or not stablecoins will stay a tolerated personal extension of greenback dominance or develop into a extra explicitly regulated layer of greenback infrastructure. It reveals that the query has moved into the greenback’s important analysis agenda.

The near-term alerts counsel policymakers will watch whether or not stablecoin progress is pushed by offshore greenback demand or home substitution from financial institution deposits.

Banks will check whether or not tokenized deposits can match the velocity and programmability of stablecoins whereas maintaining balances inside the banking system. Issuers must show that reserves, redemptions, and focus dangers can stand up to fast growth or contraction in stablecoin provide.

That’s what adjustments when the Fed treats stablecoins as a part of international greenback transmission. A token that when regarded like crypto’s settlement asset turns into a non-public greenback rail with public penalties.

Its progress can assist greenback attain, however it will probably additionally increase questions on financial institution funding, Treasury-bill demand, and liquidity stress in the identical body.

The edge is decrease than changing banks or dominating Treasury markets. Stablecoins develop into a coverage drawback as soon as they’re massive sufficient, helpful sufficient, and linked sufficient that greenback demand more and more passes by means of them.