DefiLlama’s RWA class knowledge places the RWA tokenization market close to $30 billion on-chain, with solely $2.47 billion showing as DeFi lively TVL, the worth truly deposited or pooled inside third-party DeFi protocols the platform tracks.

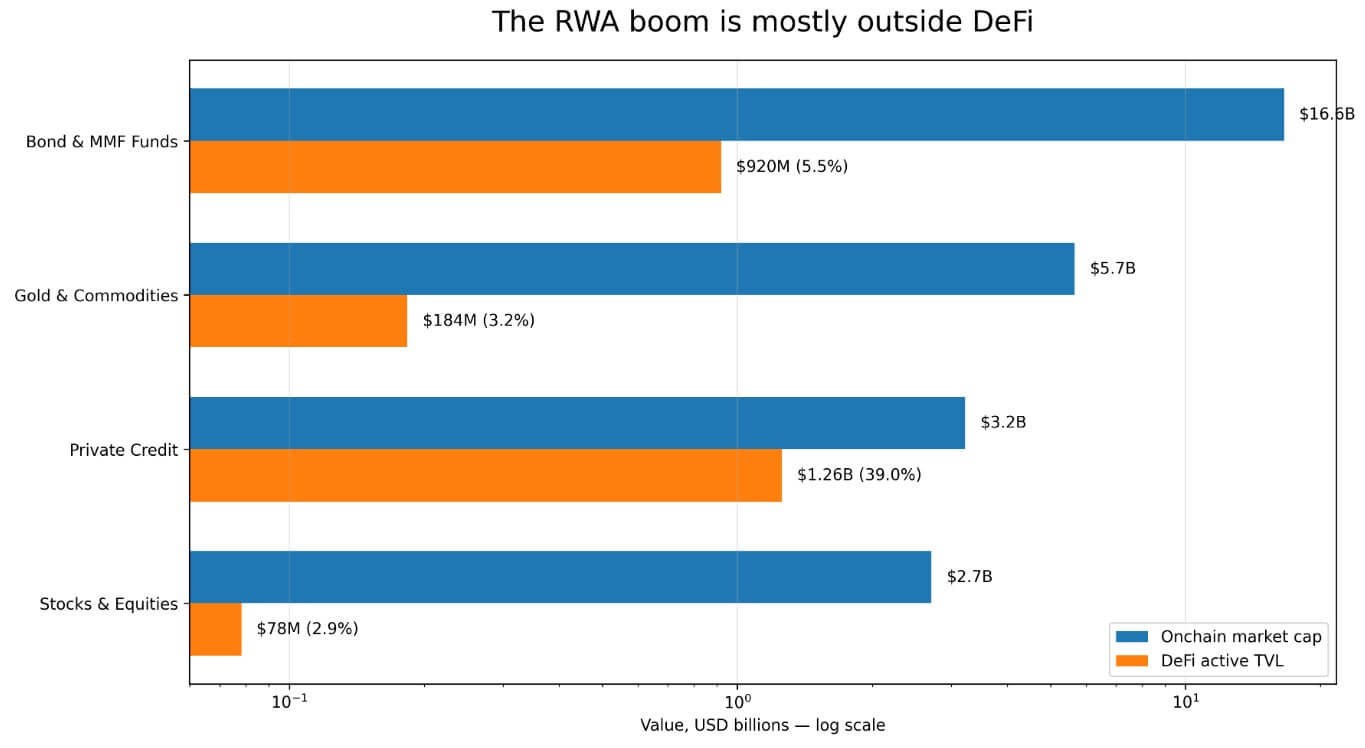

The remainder of the tokenized real-world property market sits exterior the lending markets and collateral vaults that make crypto property composable. Bond and cash market funds are the most important single RWA class at over $16.6 billion on-chain, but they carry solely $920 million in DeFi lively whole worth locked (TVL).

Gold and commodities sit at $5.7 billion on-chain towards $183.6 million in DeFi, whereas shares and equities contribute $2.7 billion on-chain towards $78.27 million in DeFi.

Personal credit score stands aside with $3.226 billion on-chain and $1.257 billion in DeFi lively TVL, a 39% ratio, pushed by protocols like Maple Finance and Centrifuge that constructed their merchandise as lending devices from inception.

Issuers constructed classes corresponding to Treasury funds, gold, and equities for institutional holding and controlled fund structure.

Permissioned structure limits DeFi composability

DefiLlama classifies BlackRock’s cash market fund, BUIDL, as permissioned and data solely $18.9 million in DeFi lively TVL for the fund.

IOSCO’s November 2025 last report on monetary asset tokenization famous that BUIDL created a permissioned system on public blockchains for issuance, custody, secondary buying and selling between allowlisted certified traders, dividend distribution, and redemption.

Potential holders should clear a Securitize-managed allowlist, and on-chain transactions carry no authorized impact till a switch agent reconciles them with the off-chain report.

That makes BUIDL a compliance infrastructure that runs on blockchain rails for institutional holding and transfer-agent reconciliation. The truth that the fund’s contracts work together solely with allowlisted addresses prevents direct deposit into open protocols like Aave or Uniswap with no compliant wrapper in between.

BlackRock’s February 2026 Uniswap integration moved a portion of BUIDL onto the platform. Nonetheless, Securitize controls the listing of eligible establishments and market makers, and entry stays restricted to certified purchasers with no less than $5 million in property.

IOSCO discovered that secondary buying and selling of tokenized cash market funds (MMFs) usually operates this manner and concluded that the sector has but to ship the promised secondary-market liquidity advantages.

RedStone’s March 2026 tokenization report recognized that the toughest a part of tokenization is dealing with compliance, identification, switch restrictions, sanctions, and company actions throughout jurisdictions and chains. That makes Morpho and Aave Horizon the clearest RWA DeFi examples within the present knowledge set.

Each extra compliance constraint a platform builds in makes the asset tougher to combine into DeFi, and issuers of tokenized Treasuries, Treasury funds, and MMFs constructed these constraints in by design to fulfill their regulated investor base.

| Constraint | What it means | Why it limits DeFi use |

|---|---|---|

| KYC / allowlisting | Solely accepted wallets can maintain or switch the asset | Open DeFi swimming pools can not freely settle for the token |

| Switch-agent reconciliation | Onchain motion may have offchain authorized affirmation | Good contracts alone could not finalize possession |

| Certified-investor limits | Entry is restricted to establishments or high-net-worth patrons | Retail DeFi liquidity is excluded |

| NAV / redemption home windows | Fund shares redeem on issuer schedules | Arduous to suit real-time AMMs or collateral liquidations |

| Centralized venue buying and selling | Exercise happens on CEXs or issuer platforms | It doesn’t seem in DeFi Energetic TVL |

The gold and commodities class provides a 3rd dimension to the stack, as CoinGecko knowledge confirmed that tokenized gold spot quantity hit $90.7 billion within the first quarter of 2026, surpassing the total yr 2025. But centralized exchanges account for the overwhelming majority of spot buying and selling for tokenized property.

The $183.6 million DeFi lively TVL determine for the class displays exercise targeting centralized venues, which falls completely exterior DefiLlama’s DeFi protocol monitoring.

The place the bull case lives

Ondo’s USDY crossed $1 billion in TVL in early 2026 and operates throughout 9 blockchains. Ondo International Markets, which launched in September 2025 to supply tokenized US shares and ETFs to non-US traders, constructed its tokens free of charge transferability and DeFi collateral acceptance, reaching $650 million in TVL and over $12 billion in cumulative buying and selling quantity.

RedStone’s report counts over $620 million in RWA deposits on Morpho and $423.5 million in whole market measurement on Aave Horizon, two lending protocols which have made RWA collateral a practical product.

These merchandise exhibit that composability is achievable on the issuance degree when designers construct for permissionless circulation from the beginning.

DWF Labs’ April 2026 roundtable with individuals from Centrifuge, Falcon Finance, and xStocks concluded that the RWA market is bifurcating into two lanes: one for ownership-first, permissioned rails, and one other for composability-first designs that mix compliant issuance with secondary-market utility.

Centrifuge’s Graham Nelson mentioned that strict allowlisting prevents an asset from getting into open swimming pools when each pool participant should be individually onboarded.

Centrifuge’s DeRWA strategy addresses this by wrapping compliant major issuance with freer secondary transferability. Falcon Finance’s Artem Tolkachev referred to as composability and exit mechanics the bridges between real-world property and crypto liquidity.

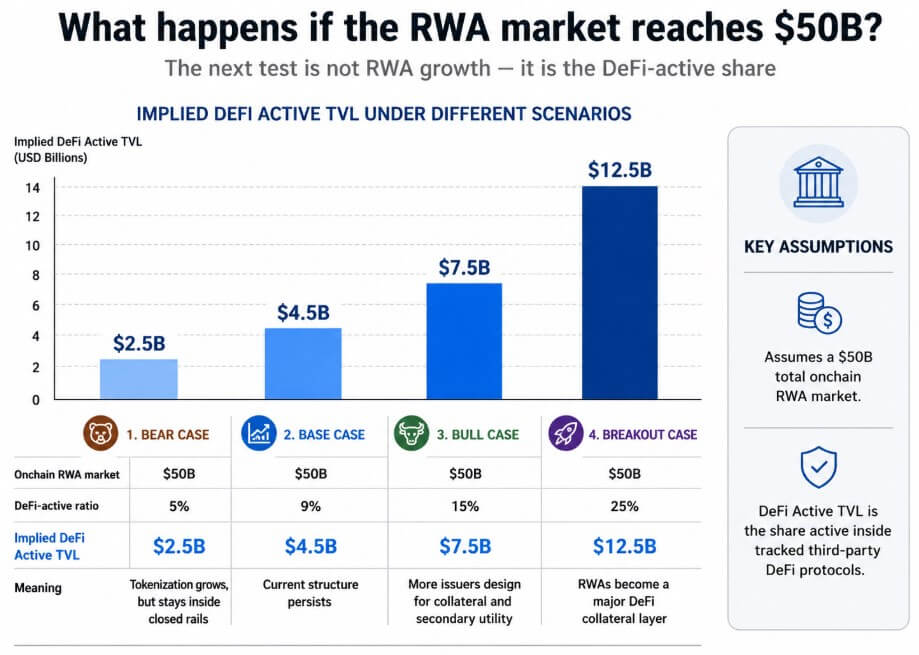

The bull case is that sufficient of the market strikes on this course to tug the DeFi-active ratio meaningfully above 9% as the entire on-chain RWA market approaches $50 billion.

The bear case, within the knowledge

Customary Chartered tasks $2 trillion in tokenized property by 2028 however warns that the increase might consolidate inside financial institution infrastructure, with open markets capturing little of the expansion.

IOSCO’s November 2025 report discovered that tokenized property nonetheless largely depend on typical monetary infrastructure for distribution and secondary buying and selling due to accessibility and liquidity constraints on DLT platforms.

The ECB famous in its April 2026 tokenization analysis that the shortage of widespread requirements can entrench tokenized markets as remoted swimming pools, every with its personal compliance framework, settlement layer, and entry mannequin, thereby concentrating liquidity inside closed networks.

Bond and MMF funds at 5.5%, gold and commodities at 3.2%, and shares and equities at 2.9% put numbers to that structural separation.

Most tokenized Treasury and MMF merchandise carry minimal funding thresholds, KYC necessities, transfer-agent reconciliation cycles, and NAV-aligned redemption home windows which are structurally incompatible with real-time AMM pricing or permissionless collateral vaults.

Regulators required these options, and issuers accepted them.

Two markets, one scoreboard

The $30 billion determine and the $2.47 billion DeFi lively TVL determine measure two distinct markets the trade teams underneath the identical RWA label.

One is regulated on-chain finance, consisting of MMFs, Treasury funds, custody rails, and issuer-managed data reconciled by switch brokers. The opposite is DeFi composability, comprised of property deposited in lending protocols, used as permissionless collateral, and built-in into automated yield methods.

Morpho’s $620 million in RWA deposits and USDY’s nine-chain footprint present the second market has actual traction.

For the DeFi-active ratio to surpass 9%, issuers must select a construction that permits permissionless circulation by design as an alternative of the BUIDL structure, the place the compliance construction is the product.

With many of the present $28.56 billion in on-chain market cap within the permissioned camp, tokenized property nonetheless look extra like regulated on-chain finance than open DeFi collateral.