Congress is shifting crypto’s subsequent adoption combat into the tax code, the place authorized rails and on a regular basis usability can cut up aside.

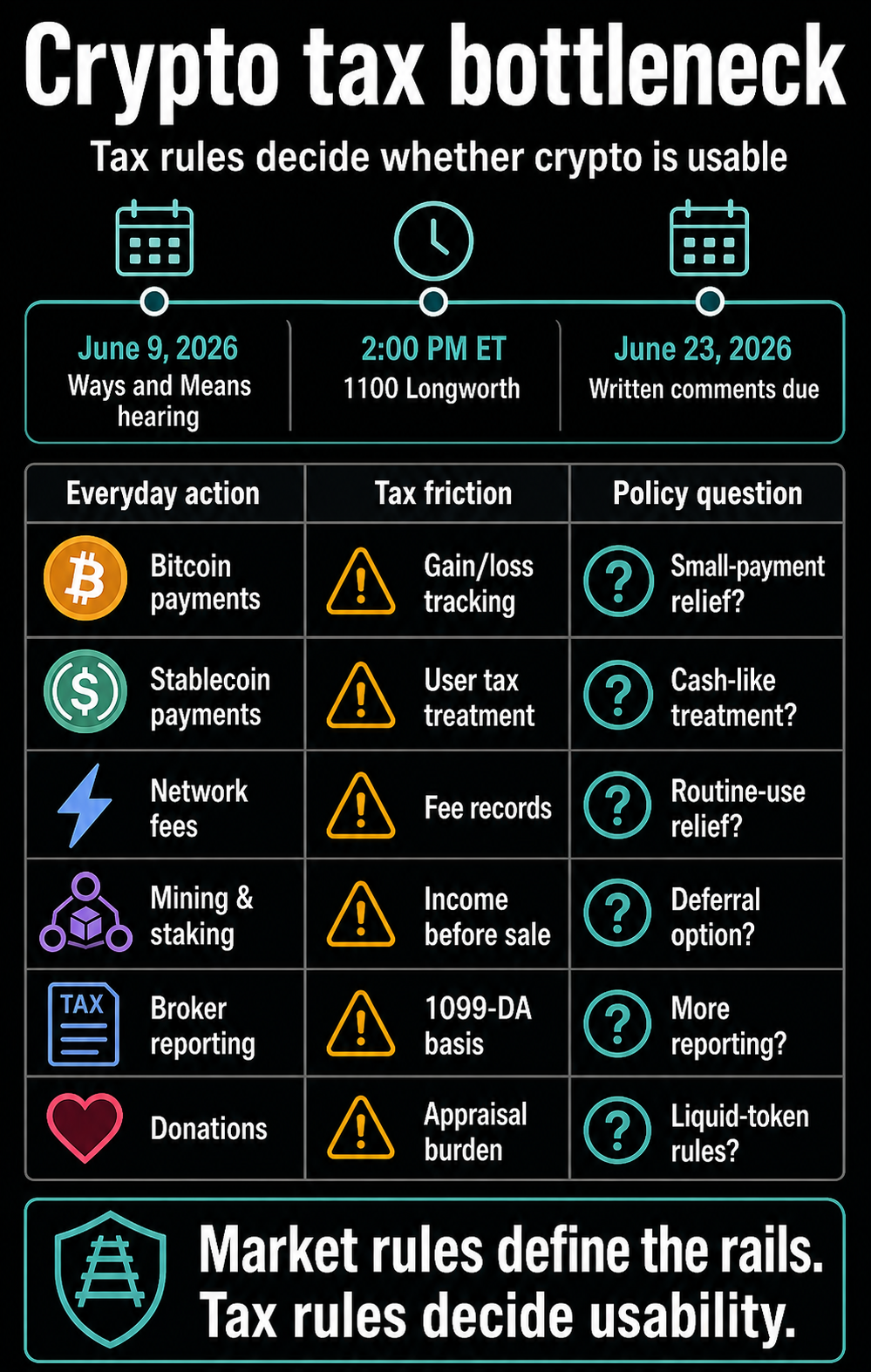

The Home Methods and Means Committee is scheduled to carry a June 9 legislative listening to on digital asset taxation at 2:00 PM ET in 1100 Longworth. The witness checklist contains Sarah Reilly of Constancy Investments, Lawrence Zlatkin of Coinbase, Jason Somensatto of Coin Heart, and Mike Kaercher of the Tax Regulation Heart at NYU Regulation.

The committee additionally set a June 23 deadline for written feedback, giving tax writers two weeks after the listening to to construct the file.

The listening to places tax guidelines on the identical coverage monitor as market construction and fee stablecoins. The GENIUS Act created a federal payment-stablecoin framework, whereas the CLARITY Act handed the Home and stays a part of the market-structure debate.

Market guidelines can outline authorized rails. Tax legislation decides whether or not a person who buys one thing with Bitcoin, strikes funds on-chain, pays a community charge, earns staking rewards, mines a block, or donates digital belongings can keep away from a separate calculation.

The query earlier than tax writers is sensible: if crypto is supposed to perform as funds and settlement infrastructure, ought to each small on-chain motion stay a taxable occasion or recordkeeping job?

The fee drawback is a tax drawback

The present baseline begins with the IRS view that convertible digital forex is property for federal tax functions, that means basic property-transaction guidelines apply.

That body turns a fee into greater than a fee. A person might have to know foundation, truthful market worth, and achieve or loss on the time of spending as an alternative of recording that {dollars} modified arms.

Taxpayers see that friction within the IRS digital belongings overview, which says individuals ought to reply sure to the digital asset query in the event that they disposed of digital belongings for items or companies in any quantity, exchanged one digital asset for one more, or paid a switch charge with digital belongings.

The identical overview says digital asset transactions should be reported whether or not or not they lead to taxable achieve or loss.

For a long-term investor, these guidelines might seem like unusual capital-asset accounting. For a fee person, they’re a design constraint.

A small Bitcoin transaction can require the identical conceptual equipment as a sale of an funding. A community charge paid in crypto can matter even when the person is shifting belongings between wallets the person owns or controls.

Lawmakers have already got a impartial map of that drawback. The Joint Committee on Taxation’s 2025 digital asset report mentioned no digital asset is handled as forex for federal earnings tax functions and that no basic de minimis rule excludes features on small private transactions.

It additionally famous the asymmetry for private use: features could be acknowledged, whereas losses usually are usually not allowed exterior enterprise or income-production settings.

That’s the core adoption bottleneck. A market can have clear buying and selling venues, regulated issuers, and higher dealer reporting whereas nonetheless leaving routine fee habits too burdensome for regular use.

Stablecoins might obtain particular therapy as a result of Congress already acted on their regulatory standing. The GENIUS Act, enacted as Public Regulation 119-27 in July 2025, created a federal regime for fee stablecoins.

Issuer guidelines and reserve requirements, nevertheless, go away user-side tax therapy as a separate query.

Stablecoins might get the primary tax break

One stay proposal exhibits how tax writers might attempt to bridge that hole. The Digital Asset PARITY Act bundle addresses stablecoin fee therapy, source-of-income guidelines, lending transactions, wash-sale and constructive-sale guidelines, mark-to-market elections, mining and staking reward timing, charitable contributions, and a Treasury examine on small digital asset transaction aid.

Probably the most direct fee provision considerations regulated greenback stablecoins. Underneath the PARITY one-pager, qualifying stablecoin spending could be handled like money for tax functions when qualification situations are met.

If enacted, that would make fee stablecoins simpler to make use of in on a regular basis commerce as a result of the person wouldn’t should deal with every qualifying stablecoin fee like a mini disposition of property.

Stablecoin-specific aid would reply a part of the usability query. It might assist digital {dollars}, however Bitcoin-style funds and different non-stablecoin transfers would nonetheless face foundation monitoring.

That distinction makes the listening to greater than a stablecoin follow-up. It’s a check of whether or not Congress desires tax aid to help regulated greenback tokens alone or to handle small digital asset exercise extra broadly.

Sen. Cynthia Lummis has already pushed the broader model of that debate, proposing a $300 de minimis rule with a $5,000 annual cap.

PARITY, in contrast, asks Treasury to review de minimis aid for small digital asset transactions and supply interim steerage. These approaches suggest totally different coverage priorities.

One favors stablecoin funds. The opposite would make it simpler for belongings corresponding to Bitcoin for use in small transactions with out fixed accounting drag.

| Exercise | Tax friction at challenge | Coverage strain level |

|---|---|---|

| Bitcoin funds | Property therapy can require achieve or loss calculation on spending. | Broader small-transaction aid or a de minimis rule would matter most. |

| Stablecoin funds | Regulatory approval leaves user-side tax therapy as a separate query. | PARITY would deal with qualifying regulated greenback stablecoin funds like money. |

| Community charges | Charges paid with digital belongings can create reportable tax data. | Lawmakers should determine how routine on-chain motion needs to be handled. |

| Mining and staking | Rewards can create earnings earlier than sale or money realization. | PARITY proposes a deferral election for as much as 5 taxable years. |

| Lending and buying and selling | Tax guidelines should distinguish unusual financing from disguised gross sales or abuse. | PARITY pairs lending therapy with wash-sale and constructive-sale provisions. |

| Donations | Noncash property guidelines can add valuation and appraisal burdens. | PARITY proposes totally different therapy for liquid belongings and fewer liquid tokens. |

Charges, mining and staking expose the identical design selection

Community charges deliver the identical tax friction to blockchain infrastructure. On-chain charges are the price of utilizing the community, but paying them with a digital asset can create reportable data even when the person is just settling or shifting belongings exterior a business buy.

Mining and staking create a special model of the mismatch. IRS steerage and JCT supplies describe rewards as taxable when acquired below present guidelines, whereas the PARITY supplies body that therapy as a cash-flow drawback for community members who might owe tax earlier than promoting the asset.

The proposed reply is an election to defer earnings recognition for as much as 5 taxable years till disposition.

For proof-of-work miners and proof-of-stake validators, that timing is operationally essential. They safe networks and obtain digital belongings as rewards.

Taxing these rewards at receipt can pressure a valuation and legal responsibility earlier than there’s money to pay it. Deferral would protect taxation whereas shifting the timing nearer to a sale or different disposition.

Dealer reporting is one other a part of the identical shift. For 2026 and past, the IRS Type 1099-DA directions require digital asset brokers to report gross proceeds for gross sales after 2025 and embody foundation reporting for lined securities.

Additionally they present elective reporting strategies for stablecoins and NFTs and add wash-sale fields for tokenized securities. The directions tackle rewards and staking funds by means of an exception relatively than by making these funds reportable on Type 1099-DA.

These guidelines go away user-side tax questions in place, however they present the tax system turning into extra specific about digital asset exercise. Reporting infrastructure, anti-abuse guidelines, and adoption aid are actually being constructed on the identical time.

The listening to will present how lawmakers attempt to distinguish unusual community use from transactions that needs to be handled like funding gross sales or tax-avoidance trades.

The listening to turns market construction right into a usability check

The witness checklist displays that broader terrain. Constancy and Coinbase deliver market and platform views. Coin Heart brings a policy-advocacy view. The Tax Regulation Heart at NYU Regulation brings a tax-law lens.

Collectively, they put the committee in place to ask what guidelines would assist the business, which guidelines are administrable for the IRS, and what therapy is truthful to taxpayers.

The June 23 remark deadline is the subsequent significant sign after the listening to. Written submissions might present whether or not commenters converge round stablecoin-specific therapy, a de minimis rule for small digital asset transactions, mining and staking timing aid, or stricter reporting and anti-abuse provisions.

CLARITY belongs within the background. Its Home passage confirmed bipartisan urge for food for outlining market oversight, and its Senate standing nonetheless issues for exchanges, brokers, issuers, and regulators.

The tax listening to asks a special query. Even when market construction turns into clearer, crypto’s on a regular basis usefulness relies on whether or not tax guidelines let individuals transact with out treating each fee, charge, and reward like a tax-lot train.

The end result may form which type of crypto adoption Congress is keen to encourage. Stablecoin-only aid may steer funds towards regulated digital {dollars} and go away Bitcoin primarily in an funding or treasury function for a lot of customers.

Broader aid for small digital asset transactions would sign a bigger ambition: crypto as usable fee know-how alongside its function as a regulated asset class.

The June 9 listening to is a coverage bottleneck in its personal proper. The legislation can inform firms the place to register and inform stablecoin issuers how you can function, however tax guidelines determine whether or not an individual can truly use a digital asset with out opening a spreadsheet.

Till Congress solutions that query, spending crypto stays much less like tapping a card and extra like promoting a tiny piece of property every time.