BlackRock has up to date its regulatory submitting for a brand new Bitcoin Premium Revenue ETF, signaling an imminent launch that intensifies a Wall Avenue race towards Goldman Sachs Group to seize yield-seeking digital asset traders.

On June 10, the world’s largest asset supervisor submitted an up to date prospectus to the Securities and Trade Fee (SEC) for the iShares Bitcoin Premium Revenue ETF, which can commerce below the ticker BITA.

The modification introduces crucial operational and pricing parameters, together with an annualized sponsor price of 0.65% that might be payable at the least quarterly.

The price positions BITA as a higher-cost various to plain-vanilla spot Bitcoin funds, akin to BlackRock’s personal iShares Bitcoin Belief (IBIT).

Nonetheless, this price is considerably beneath the expense constructions typical of bigger equity-based covered-call ETFs at the moment working in conventional monetary markets.

In the meantime, Bloomberg Intelligence ETF analyst Eric Balchunas mentioned the submission possible represents the ultimate structural adjustment earlier than the fund receives regulatory approval to start public buying and selling.

Contained in the Seed Capital and Belief Mechanics

The up to date registration assertion gives an operational have a look at the fund’s preliminary monetary standing, filling in a number of key metrics that had been omitted within the preliminary January submitting.

The documentation notes that an preliminary seed investor acquired 198,000 shares at $50 per share on June 1, which supplied $9.9 million in proceeds to determine the belief.

In response to the submitting, BlackRock deployed that capital to determine the fund’s baseline portfolio on June 9. The belief acquired precisely 109.9630217 Bitcoin alongside 90,901 shares of IBIT.

Concurrently, the fund managers wrote 856 choices contracts to provoke the income-generating element of the technique. Following these transactions, the belief reported a web asset worth of roughly $9.99 million, representing an preliminary web asset worth per share of $49.97.

To keep up each day operations, the prospectus notes that the belief intends to meet its ongoing 0.65% sponsor price by periodically liquidating parts of its IBIT holdings.

This mechanical design displays the fund’s blended composition, holding bodily Bitcoin, liquid spot ETF shares, and money devices concurrently whereas writing choices contracts primarily towards its IBIT fairness allocation.

The covered-call technique and volatility dynamics

The funding mandate positions BITA as a covered-call Bitcoin ETF designed to trace Bitcoin’s baseline efficiency whereas producing premium distributions.

The administration staff intends to attain this by promoting name choices on IBIT shares and, sometimes, on specialised indexes that monitor broader spot Bitcoin exchange-traded merchandise.

By promoting these choices, the fund collects upfront premiums from counterparties looking for leveraged publicity to potential upward actions in IBIT’s share value. In change for this instant income stream, the fund surrenders its proper to capital appreciation above a predetermined strike value.

BlackRock’s technique entails sustaining a goal overwrite stage between 25% and 35% of the belief’s whole web asset worth.

This partial overwrite technique ensures {that a} important majority of the portfolio stays unhedged, permitting shareholders to take part in a portion of Bitcoin’s market rallies whereas using a smaller section of the asset base to maintain distribution yields.

For asset allocators, the construction mirrors equity-linked revenue automobiles which have gained substantial market share during times of range-bound or reasonably optimistic inventory efficiency.

Cryptocurrency presents a novel underlying asset for this technique because of its structurally elevated implied volatility relative to standard asset courses like equities or sovereign debt. Excessive volatility inflates the market value of choices contracts, theoretically permitting BITA to reap bigger premiums than comparable stock-index funds.

Nevertheless, this income-generation mannequin entails inherent trade-offs. In a pointy cryptocurrency bull market, the written name choices cap the fund’s whole returns, inflicting BITA to underperform the underlying spot asset.

Conversely, the technique provides average draw back safety throughout flat or mildly declining market environments, because the collected premiums offset minor capital losses.

Goldman Sachs escalates the aggressive race

The timing of BlackRock’s modification intensifies a confrontation with Goldman Sachs, which has superior its personal regulatory framework for a competing automobile.

The Goldman Sachs Bitcoin Premium Revenue ETF is projected to finish its regulatory evaluation course of and turn out to be efficient close to the start of July.

Whereas each Wall Avenue establishments are focusing on equivalent buyer demographics, their operational frameworks exhibit stark variations.

The Goldman Sachs product is not going to maintain bodily cryptocurrency immediately. As an alternative, the funding technique dictates that at the least 80% of its web property might be directed into automobiles offering Bitcoin publicity, together with exterior spot Bitcoin ETPs, exchange-traded choices contracts, and a wholly-owned subsidiary based mostly within the Cayman Islands.

Moreover, Goldman Sachs plans to implement a extra aggressive choices overwrite framework. Its regulatory filings point out an anticipated choices overwrite stage ranging between 40% and 100% of its whole Bitcoin publicity below commonplace market situations.

| Function | iShares Bitcoin Premium Revenue ETF (BITA) | Goldman Sachs Bitcoin Premium Revenue ETF |

|---|---|---|

| Direct BTC Holdings | Sure (blended with IBIT) | No (makes use of ETPs and Cayman subsidiary) |

| Goal Overwrite Vary | 25% to 35% of NAV | 40% to 100% of publicity |

| Sponsor/Administration Charge | 0.65% annualized | To be finalized |

| Major Choices Goal | IBIT shares and spot Bitcoin indexes | Broad Bitcoin ETPs and choices markets |

This operational variance may dictate market preferences as soon as each funds are lively. Goldman’s wider overwrite parameters allow larger theoretical distribution yields throughout stagnant market situations however expose traders to extra intensive upside caps throughout sudden Bitcoin market rallies.

Alternatively, BlackRock’s conservative 25% to 35% vary retains larger capital appreciation potential at the price of decrease baseline distribution targets.

Maturation of the Bitcoin ecosystem

The transition towards actively managed, yield-bearing cryptocurrency merchandise marks the second main evolution of the digital asset ETF ecosystem.

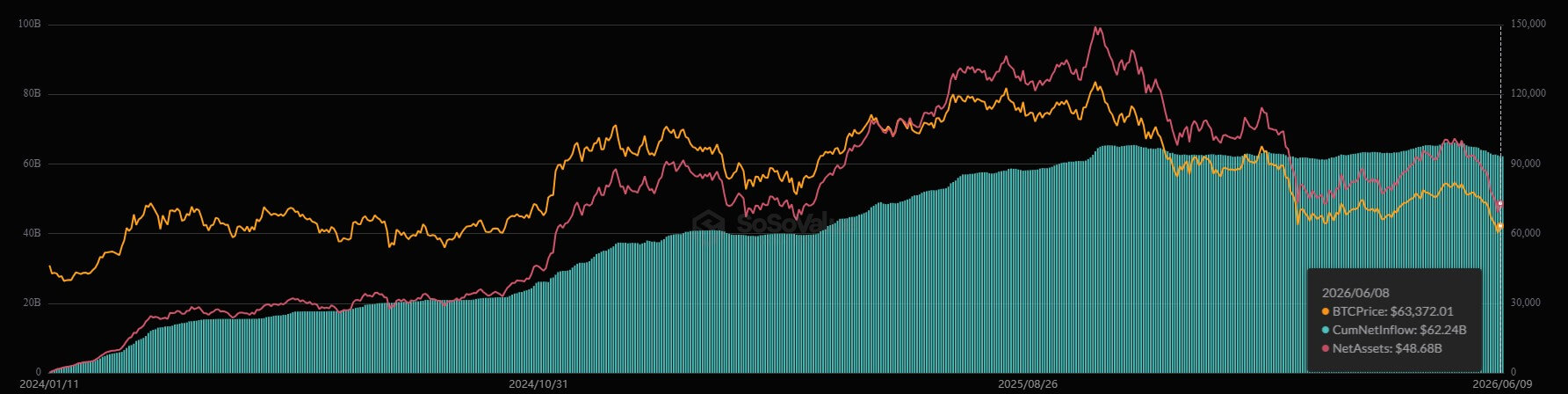

The primary section centered completely on establishing direct infrastructure, exemplified by BlackRock’s flagship spot automobile, IBIT, which has collected $62 billion in whole web inflows since its 2024 launch, in response to information compiled by SoSoValue.

The introduction of BITA and Goldman’s rival product indicators that Bitcoin ETF revenue is changing into a definite product class past fundamental spot publicity.

Wall Avenue asset managers at the moment are specializing in product differentiation to draw risk-averse institutional portfolios and wealth advisory networks that prioritize recurring money move over pure hypothesis.

This rising section shouldn’t be with out present competitors. The upcoming institutional choices will enter a market the place specialised issuers have already established an early foothold. The NEOS Bitcoin Excessive Revenue ETF (BTCI), as an illustration, has collected greater than $1 billion in property below administration by using a comparable options-driven yield framework.

In the meantime, the long-term viability of those premium revenue automobiles rests on investor schooling concerning the excellence between structural yield and conventional fixed-income securities.

The payouts generated by BITA and its friends are derived completely from choices pricing dynamics and market volatility, moderately than curiosity funds or underlying company money flows.

Consequently, distribution charges will fluctuate based mostly on macroeconomic shifts, buying and selling volumes, and shifting choices volatility indices.