A Home of Lords committee has advised the Financial institution of England to rethink stablecoin caps earlier than the UK’s regime is finalized.

The Monetary Companies Regulation Committee revealed its report, Stablecoins: ready for regulation, on June 3, turning a technical debate over reserve design right into a check of whether or not the UK can construct a pound-denominated stablecoin market with out making it uneconomic from the beginning.

The stress level is the design of the safeguards. The committee helps 1:1 backing and accepts that stablecoins can create dangers round monetary stability, shopper safety, and illicit finance.

Its problem is extra particular: the Financial institution’s proposed safeguards could also be calibrated for a market that doesn’t but exist within the UK.

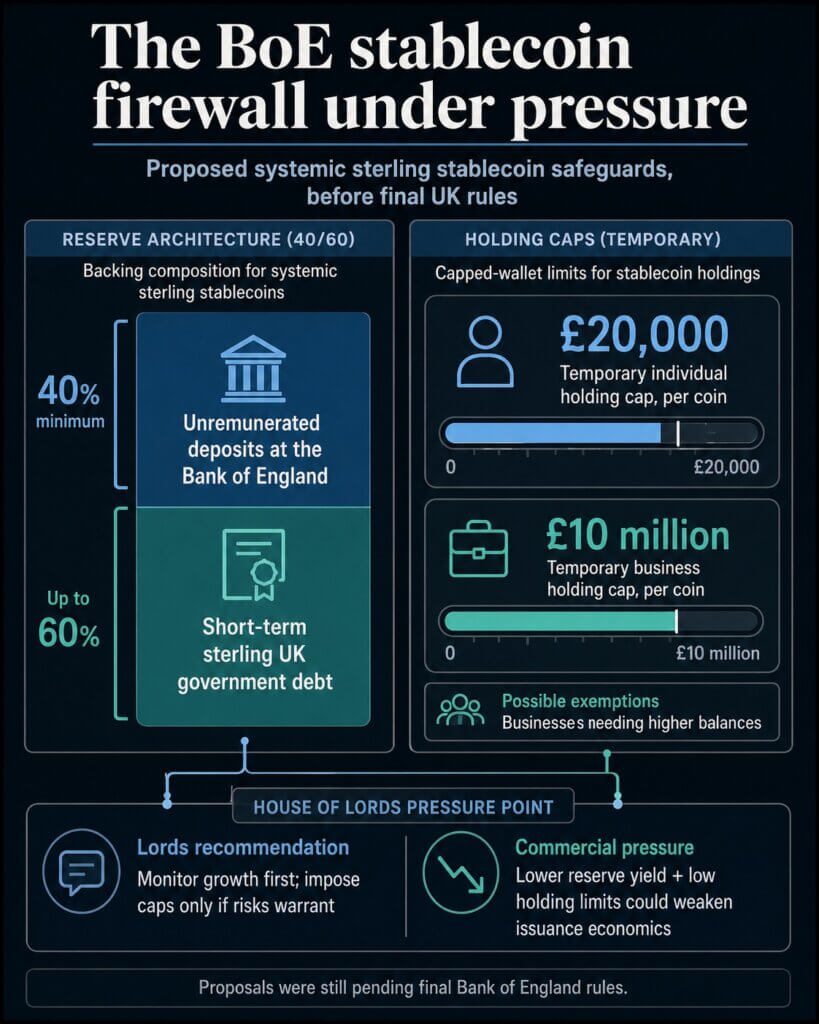

Two measures sit on the middle of that critique. The Financial institution has proposed non permanent per-coin holding limits of £20,000 for people and £10 million for companies.

It has additionally proposed requiring systemic sterling stablecoin issuers to maintain no less than 40% of backing belongings as deposits on the Financial institution of England that don’t earn curiosity.

The Lords report says these selections may form whether or not a GBP stablecoin market develops in any respect. If a pound stablecoin can’t be held in helpful quantities or generate sufficient reserve earnings to assist the issuer’s enterprise, the UK may find yourself with clear guidelines, however few corporations keen to construct the merchandise these guidelines are supposed to govern.

The Guidelines Beneath Stress

The Financial institution of England’s November 2025 session proposed a cut up backing mannequin for systemic sterling stablecoins.

Not less than 40% of backing belongings would sit as deposits on the Financial institution, whereas as much as 60% might be held in short-term sterling-denominated UK authorities debt.

The Financial institution’s case is that central-bank deposits present fast liquidity if holders search massive redemptions in a brief interval. In its session, it stated the edge aligned with estimates of potential short-term redemption requests drawn from stress occasions in conventional and crypto markets.

The 60% government-debt allowance was meant to enhance issuer viability in contrast with an earlier mannequin that will have positioned all backing belongings in unremunerated central-bank deposits.

That compromise is now underneath stress. The Lords committee concluded that remuneration and liquidity necessities for backing belongings may have a big impact on issuer viability and UK competitiveness.

It urged the Financial institution to contemplate the affect of requiring a proportion of unremunerated belongings and to rethink whether or not deposits held on the Financial institution ought to be remunerated at Financial institution Price.

The committee additionally pushed the Financial institution towards a extra versatile strategy to backing-asset composition. It stated the Financial institution ought to be open to a principles-based and fewer prescriptive mannequin, with necessities adjusted as market conduct and dangers develop into clearer.

The identical logic applies to holding limits. The Financial institution’s proposal would cap every particular person’s holdings of a systemic stablecoin at £20,000 per coin and every enterprise’s holdings at £10 million, with potential exemptions for companies that want increased balances in regular operations.

In a November information launch, the Financial institution framed these limits as non permanent instruments to guard entry to credit score whereas the monetary system adapts to new types of cash.

The committee’s advice was sharper. Given the early stage of the GBP stablecoin market, it stated the Financial institution ought to monitor progress and impose holding limits provided that monetary stability dangers clearly warrant them.

If limits develop into mandatory, the committee stated the Financial institution ought to seek the advice of to make sure they are often applied in a sensible approach that also meets the Financial institution’s aims.

Why The Financial institution Is Cautious

The Financial institution’s concern goes past competitors with banks. Within the UK, financial institution deposits do extra work contained in the credit score system than they do in another main markets.

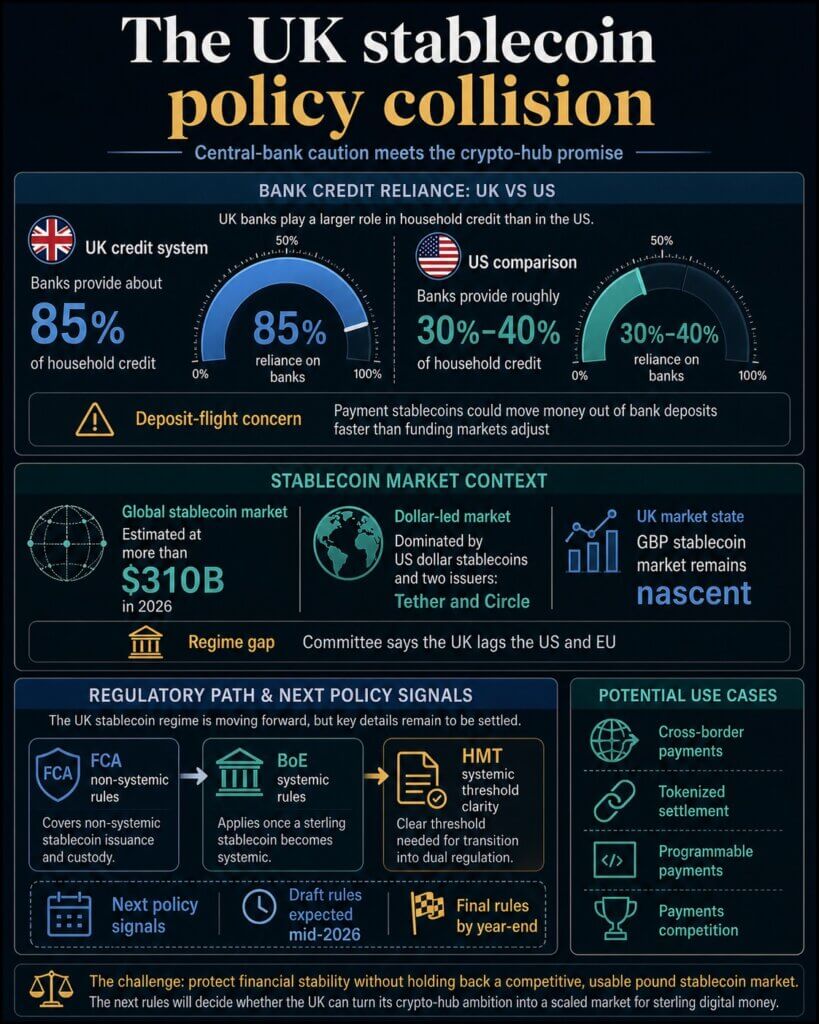

In oral proof to the committee in March, Sarah Breeden, the Financial institution’s deputy governor for monetary stability, stated banks present about 85% of family credit score within the UK, in contrast with roughly 30% to 40% within the US.

Her argument was that if deposits moved quickly into fee stablecoins and that funding was not changed, the outcome might be a drop in credit score for households and companies.

That’s the financial-stability case for a circuit breaker. The Financial institution is designing for a future during which stablecoins are extensively used as cash for on a regular basis funds, past their present use in crypto buying and selling.

If adoption moved rapidly by means of social media platforms, e-commerce networks, wallets, or automated fee instruments, the Financial institution worries that cash may depart deposits quicker than banks and funding markets may regulate.

The committee accepts that threat. Its report says stablecoins can pose challenges round monetary stability, illicit finance, and shopper safety.

It additionally welcomes 1:1 backing, audited reserves, disclosure, statutory belief protections, and the proposed Financial institution backstop lending facility for systemic issuers.

The disagreement is about timing and prescription. Lawmakers are asking whether or not the Financial institution ought to impose caps and reserve economics earlier than there’s sufficient proof about how a pound stablecoin market would behave.

A protecting rulebook may cut back the prospect of a disorderly shift out of financial institution deposits. It may additionally make the regulated model of the product much less enticing than offshore, dollar-denominated, or non-systemic alternate options.

The stakes are increased as a result of the report describes the UK stablecoin market as nascent whereas the worldwide market is already massive and dollar-led.

It says the worldwide stablecoin market was estimated at greater than $310 billion in 2026, overwhelmingly dominated by US greenback stablecoins and two issuers, Tether and Circle.

For the UK, that creates a strategic downside. A sterling stablecoin market may assist cross-border funds, tokenized settlement, programmable funds, and competitors in funds.

It may additionally cut back the danger that UK customers and companies default to greenback stablecoins as a result of pound alternate options by no means get sufficient regulatory readability or business scale.

The committee says the UK is already lagging the US and EU in creating a stablecoin regime, although it says the nation is now transferring in the suitable course.

The FCA’s stablecoin issuance and crypto custody session covers the non-systemic facet of the regime, whereas the Financial institution’s guidelines apply as soon as a sterling stablecoin turns into systemic.

The transition between these regimes stays one of many areas issuers want to know earlier than they’ll construct sturdy enterprise plans.

The Subsequent Sign Is The Draft Rulebook

The timing makes the Lords report greater than a retrospective critique. Breeden advised the committee in March that the Financial institution anticipated draft guidelines in the midst of 2026, last guidelines by year-end, and purposes from stablecoin issuers by the top of the 12 months.

Which means the following coverage doc will present whether or not the Financial institution treats the report as a purpose to alter the design or as a problem to elucidate the present mannequin extra clearly.

The indicators to observe are particular: whether or not per-holder caps stay, whether or not the Financial institution shifts towards combination issuance guardrails or monitoring triggers, whether or not the 40% deposit share is adjusted, and whether or not any Financial institution deposits obtain remuneration.

Rewards will rely, too. The committee famous comparatively little demand for issuers to pay curiosity on stablecoins, however stated the therapy of rewards, rebates, or different incentives may have an effect on the creation of a GBP stablecoin market and the UK’s worldwide competitiveness.

That query connects stablecoin guidelines to the broader funds market, the place card networks and monetary apps already compete by means of reward constructions.

The report additionally asks for extra readability from HM Treasury on when a stablecoin turns into systemic. That threshold is central for issuers as a result of it determines when a agency strikes from the FCA-only monitor into twin regulation by the Financial institution and FCA.

If the transition is just too unsure, scaling could develop into a threat in itself.

In a November information launch, the Financial institution framed these limits as non permanent instruments to guard entry to credit score whereas the monetary system adapts to new types of cash.

The committee’s advice was sharper. Given the early stage of the GBP stablecoin market, it stated the Financial institution ought to monitor progress and impose holding limits provided that monetary stability dangers clearly warrant them.

If limits develop into mandatory, the committee stated the Financial institution ought to seek the advice of to make sure they are often applied in a sensible approach that also meets the Financial institution’s aims.

Why The Financial institution Is Cautious

The Financial institution’s concern goes past competitors with banks. Within the UK, financial institution deposits do extra work contained in the credit score system than they do in another main markets.

In oral proof to the committee in March, Sarah Breeden, the Financial institution’s deputy governor for monetary stability, stated banks present about 85% of family credit score within the UK, in contrast with roughly 30% to 40% within the US.

Her argument was that if deposits moved quickly into fee stablecoins and that funding was not changed, the outcome might be a drop in credit score for households and companies.

That’s the financial-stability case for a circuit breaker. The Financial institution is designing for a future during which stablecoins are extensively used as cash for on a regular basis funds, past their present use in crypto buying and selling.

If adoption moved rapidly by means of social media platforms, e-commerce networks, wallets, or automated fee instruments, the Financial institution worries that cash may depart deposits quicker than banks and funding markets may regulate.

The committee accepts that threat. Its report says stablecoins can pose challenges round monetary stability, illicit finance, and shopper safety.

It additionally welcomes 1:1 backing, audited reserves, disclosure, statutory belief protections, and the proposed Financial institution backstop lending facility for systemic issuers.

The disagreement is about timing and prescription. Lawmakers are asking whether or not the Financial institution ought to impose caps and reserve economics earlier than there’s sufficient proof about how a pound stablecoin market would behave.

A protecting rulebook may cut back the prospect of a disorderly shift out of financial institution deposits. It may additionally make the regulated model of the product much less enticing than offshore, dollar-denominated, or non-systemic alternate options.

The stakes are increased as a result of the report describes the UK stablecoin market as nascent whereas the worldwide market is already massive and dollar-led.

It says the worldwide stablecoin market was estimated at greater than $310 billion in 2026, overwhelmingly dominated by US greenback stablecoins and two issuers, Tether and Circle.

For the UK, that creates a strategic downside. A sterling stablecoin market may assist cross-border funds, tokenized settlement, programmable funds, and competitors in funds.

It may additionally cut back the danger that UK customers and companies default to greenback stablecoins as a result of pound alternate options by no means get sufficient regulatory readability or business scale.

The committee says the UK is already lagging the US and EU in creating a stablecoin regime, although it says the nation is now transferring in the suitable course.

The FCA’s stablecoin issuance and crypto custody session covers the non-systemic facet of the regime, whereas the Financial institution’s guidelines apply as soon as a sterling stablecoin turns into systemic.

The transition between these regimes stays one of many areas issuers want to know earlier than they’ll construct sturdy enterprise plans.

The Subsequent Sign Is The Draft Rulebook

The timing makes the Lords report greater than a retrospective critique. Breeden advised the committee in March that the Financial institution anticipated draft guidelines in the midst of 2026, last guidelines by year-end, and purposes from stablecoin issuers by the top of the 12 months.

Which means the following coverage doc will present whether or not the Financial institution treats the report as a purpose to alter the design or as a problem to elucidate the present mannequin extra clearly.

The indicators to observe are particular: whether or not per-holder caps stay, whether or not the Financial institution shifts towards combination issuance guardrails or monitoring triggers, whether or not the 40% deposit share is adjusted, and whether or not any Financial institution deposits obtain remuneration.

Rewards will rely, too. The committee famous comparatively little demand for issuers to pay curiosity on stablecoins, however stated the therapy of rewards, rebates, or different incentives may have an effect on the creation of a GBP stablecoin market and the UK’s worldwide competitiveness.

That query connects stablecoin guidelines to the broader funds market, the place card networks and monetary apps already compete by means of reward constructions.

The report additionally asks for extra readability from HM Treasury on when a stablecoin turns into systemic. That threshold is central for issuers as a result of it determines when a agency strikes from the FCA-only monitor into twin regulation by the Financial institution and FCA.

If the transition is just too unsure, scaling could develop into a threat in itself.

CryptoSlate has already coated adjoining UK fee infrastructure strikes, together with Revolut’s pound stablecoin sandbox trial and the Financial institution’s 24/7 settlement plans.

The Lords report strikes the talk to a distinct level: whether or not the UK’s stablecoin rulebook will let a sterling market develop into commercially significant as soon as tokenized funds enter the system.

The Financial institution remains to be finalizing the regime, and the committee remains to be asking for financial-stability protections. The brand new stress is for the Financial institution to indicate that its safeguards won’t cease a pound stablecoin market earlier than it has an opportunity to kind.

That’s the dwell check for the UK’s crypto-hub promise. The subsequent draft guidelines will present whether or not the Financial institution’s stablecoin firewall is a brief guardrail, a redesign in progress, or a value issuers determine the pound market can’t soak up.

” width=”819″ top=”1024″ data-srcset=”https://cryptoslate.com/wp-content/uploads/2026/06/ig_00979bc5d4b7cc9f016a1fefdcf1b88191817712db7a8bb4c5-819×1024.jpeg 819w, https://cryptoslate.com/wp-content/uploads/2026/06/ig_00979bc5d4b7cc9f016a1fefdcf1b88191817712db7a8bb4c5-240×300.jpeg 240w, https://cryptoslate.com/wp-content/uploads/2026/06/ig_00979bc5d4b7cc9f016a1fefdcf1b88191817712db7a8bb4c5-768×960.jpeg 768w, https://cryptoslate.com/wp-content/uploads/2026/06/ig_00979bc5d4b7cc9f016a1fefdcf1b88191817712db7a8bb4c5.jpeg 1122w” data-sizes=”(max-width: 819px) 100vw, 819px” />

CryptoSlate has already coated adjoining UK fee infrastructure strikes, together with Revolut’s pound stablecoin sandbox trial and the Financial institution’s 24/7 settlement plans.

The Lords report strikes the talk to a distinct level: whether or not the UK’s stablecoin rulebook will let a sterling market develop into commercially significant as soon as tokenized funds enter the system.

The Financial institution remains to be finalizing the regime, and the committee remains to be asking for financial-stability protections. The brand new stress is for the Financial institution to indicate that its safeguards won’t cease a pound stablecoin market earlier than it has an opportunity to kind.

That’s the dwell check for the UK’s crypto-hub promise. The subsequent draft guidelines will present whether or not the Financial institution’s stablecoin firewall is a brief guardrail, a redesign in progress, or a value issuers determine the pound market can’t soak up.