Coinbase, the biggest US-based alternate, ended a tough first quarter with a contemporary check of investor confidence after the crypto alternate missed Wall Avenue estimates by reporting one other quarterly loss, and later suffered a service disruption tied to an Amazon Internet Companies (AWS) outage.

The sequence gave buyers a pointy reminder of the corporate’s two competing narratives. Coinbase stays closely uncovered to crypto buying and selling cycles, which weakened within the first three months of the yr as Bitcoin and different digital belongings retreated from latest highs.

On the similar time, the corporate is asking the market to worth it much less as a easy token alternate and extra because the infrastructure layer for stablecoins, derivatives, prediction markets, and synthetic intelligence-driven funds.

Buying and selling slowdown hits first-quarter outcomes

Coinbase reported income of $1.41 billion for the quarter ended March 31, beneath Wall Avenue expectations of about $1.52 billion. The corporate posted a lack of $1.49 per share, in contrast with expectations for a revenue, as weaker buying and selling exercise weighed on its largest income stream.

The corporate reported a internet lack of $394.1 million, marking its second consecutive quarterly loss after a $667 million loss within the fourth quarter of 2025. A yr earlier, Coinbase had posted a revenue of $65.6 million.

The weak spot was clearest in transaction income, which stays intently tied to buyer buying and selling exercise. Coinbase generated $755.8 million in transaction income, beneath analyst estimates of about $805 million.

Shopper transaction income fell 23% from the earlier quarter to $567 million, pushed by a 35% decline in shopper spot buying and selling quantity. Institutional transaction income declined 27% to $136 million, whereas different transaction income fell 17% to $53 million.

The pullback could be linked to a weaker quarter for crypto markets. Knowledge from CoinGlass confirmed Bitcoin completed the primary quarter down over 20%, lowering the sort of speculative exercise that sometimes helps alternate income.

Notably, decrease costs and thinner buying and selling exercise additionally pressured different crypto corporations throughout the interval, as merchants moved away from riskier digital-asset positions.

Coinbase leans into the ‘every little thing alternate’

On X, CEO Brian Armstrong used the earnings name to argue that crypto infrastructure is transferring into a brand new section.

He mentioned the on-chain financial system has reached “escape velocity” and that Coinbase’s full-stack platform is positioned to seize the subsequent wave of monetary exercise, together with AI brokers transacting with stablecoins.

In his argument, the corporate is already changing into extra diversified, as evidenced by the truth that its subscription and providers section has turn out to be a bigger a part of its enterprise, supported by stablecoins, staking, custody, and different merchandise much less straight tied to day by day buying and selling volumes.

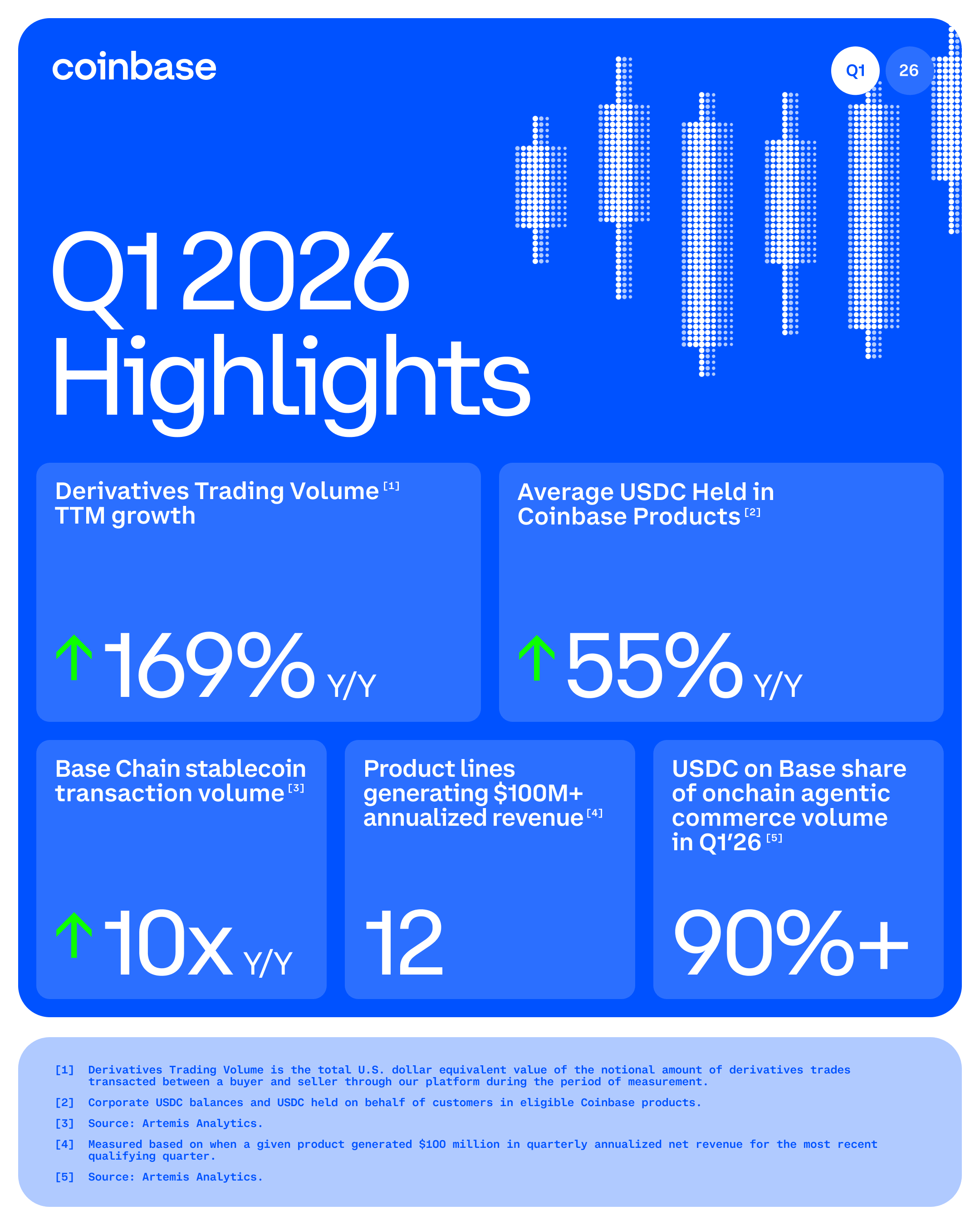

For context, the alternate’s stablecoin income totaled $305 million within the quarter, up from $274 million a yr earlier. Coinbase mentioned the rise was pushed by development out there worth of USDC and document common USDC balances held in Coinbase merchandise.

On the similar time, the agency mentioned it gained share in each spot and derivatives buying and selling globally, reaching an all-time excessive of 8.6% within the crypto buying and selling quantity market share.

The corporate additionally recorded about $4.2 billion in first-quarter derivatives buying and selling quantity, up 169% from the identical interval a yr earlier.

That development helps Armstrong’s “every little thing alternate” plan, which goals to make Coinbase a venue not just for shopping for and promoting Bitcoin, Ethereum, and different tokens but in addition for derivatives, real-world belongings, prediction markets, and, finally, different types of monetary publicity.

Chief Monetary Officer Alesia Haas argued that Coinbase’s underlying enterprise remained robust to help that thesis whereas noting that the agency has 12 product strains producing greater than $100 million in annualized income.

This view was additionally corroborated by Armstrong, who added:

“Our thesis is easy: crypto is the most effective type of cash, and the infrastructure will overhaul the present monetary system. If it includes cash, it is going to contain crypto. Coinbase is uniquely positioned to capitalize on this transformation.”

Outage exams infrastructure pitch

That message was sophisticated by the service disruption that adopted the earnings launch.

Coinbase mentioned some customers have been unable to transact on Coinbase Alternate after AWS reported issues in its US-EAST-1 area.

The difficulty was linked to elevated temperatures at an information heart in Northern Virginia, the place a thermal occasion triggered energy loss and broken some {hardware} tied to EC2 situations and EBS volumes.

On X, Coinbase acknowledged:

“Coinbase methods are designed to be resilient to a single zone outage, and are designed to get better shortly if this occurs. On this case, we noticed failures impacting a number of AWS zones, which triggered an prolonged outage of core buying and selling providers. Coinbase customers skilled an prolonged outage whereas the AWS group labored to revive temperature controls and different Amazon Managed Companies.”

As of press time, the agency mentioned the first problem was totally resolved, and all markets had been re-enabled for buying and selling.

For a standard alternate, a cloud-linked outage is a technical incident. For Coinbase, the timing made it extra consequential.

The corporate is making an attempt to place itself as a core venue for buying and selling, funds, stablecoins, derivatives, prediction markets, and on-chain monetary purposes. A several-hour disruption after an earnings miss gave skeptics one more reason to query whether or not the infrastructure can scale with the broader ambitions.

The difficulty additionally revived acquainted considerations about crypto platforms’ dependence on centralized expertise suppliers. Coinbase operates in an business constructed round decentralization, but its retail and institutional entry factors nonetheless depend on standard cloud infrastructure.

That doesn’t undermine Coinbase’s enterprise by itself. Main monetary and expertise corporations depend on AWS and different cloud suppliers. But it surely offers buyers one other metric to observe as Coinbase expands into extra markets the place uptime, settlement reliability, and institutional belief carry larger weight.

Bulls look towards a $300 billion state of affairs

Nonetheless, probably the most aggressive bull case now rests on Coinbase changing into a serious platform for AI-native finance.

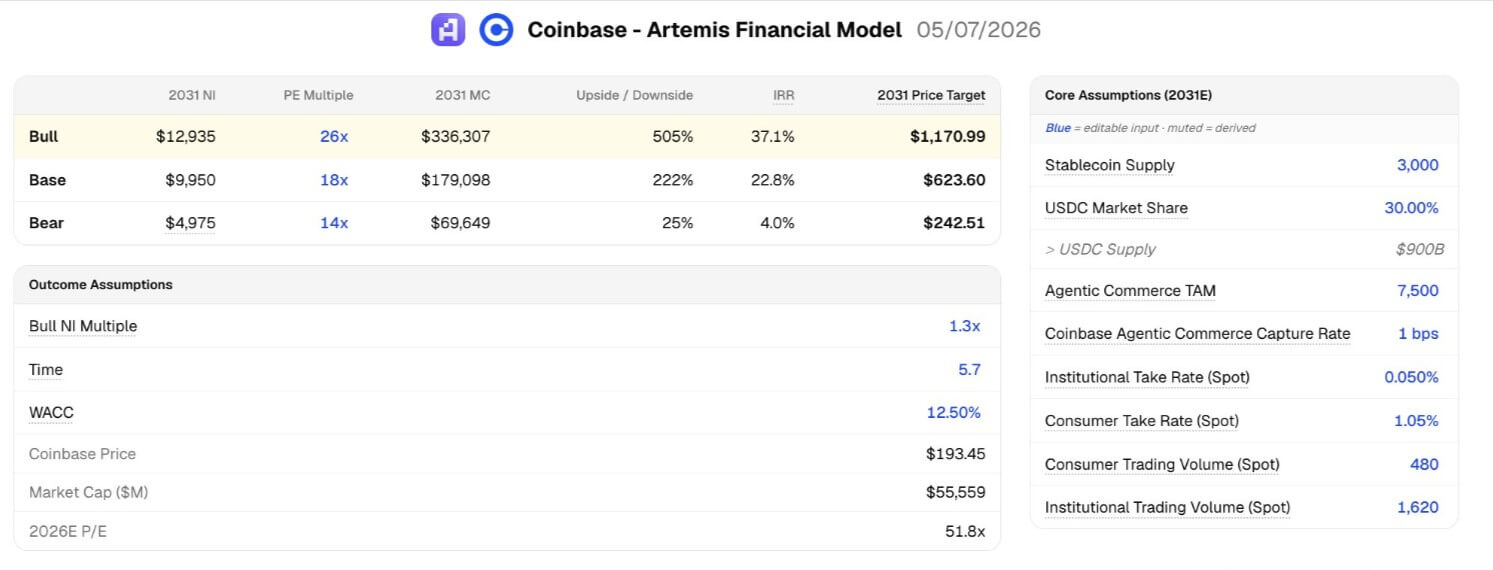

Blockchain analytics agency Artemis has argued that Coinbase might be price greater than $300 billion by 2031, roughly six occasions its present market worth.

The projection will depend on a number of assumptions: stablecoin provide reaching about $3 trillion, USDC capturing 30% of that market, agentic commerce reaching $7.5 trillion in annual spending, and Coinbase capturing one foundation level of that exercise.

The mannequin additionally assumes Coinbase’s internet transaction income grows at an 11% compound annual price and that subscription and providers income rises from about 40% of complete income to 65% by 2031.

In that state of affairs, Coinbase would generate about $23 billion in income and $10 billion in internet revenue by 2031.

That projection is much from assured. It requires stablecoins to turn out to be a a lot bigger a part of world finance, USDC to carry or broaden its market place, Base to stay related, and AI brokers to turn out to be significant financial actors relatively than a speculative expertise theme.

It additionally requires Coinbase to handle the dangers that surfaced throughout the newest quarter. Buying and selling income nonetheless fell sharply when crypto costs weakened.

The corporate remained uncovered to market cycles. Its shares reacted negatively to the earnings miss. A cloud-linked outage interrupted service at a second when the corporate was making an attempt to emphasise reliability and scale.

But the quarter additionally confirmed why Coinbase stays tough to worth by a easy alternate a number of.

The corporate purchased $88 million price of Bitcoin throughout the quarter, bringing its holdings to 16,492 BTC. It expanded stablecoin income, gained buying and selling share, grew derivatives quantity, and continued constructing new enterprise strains that might be much less tied to retail spot hypothesis over time.

Coinbase’s near-term story remains to be formed by crypto costs, buying and selling urge for food, and working execution. Its longer-term valuation will depend on whether or not stablecoins, Base, derivatives, prediction markets, and AI-driven commerce can turn out to be giant sufficient to alter the corporate’s earnings base.

The primary quarter gave either side proof. Bears noticed decrease income, one other loss, weaker buying and selling, and an outage.

Bulls noticed an organization nonetheless including customers’ native models, increasing past spot markets, and constructing towards a monetary platform that might turn out to be far bigger if crypto’s subsequent section is pushed by funds and automatic commerce relatively than one other retail buying and selling increase.