Bitcoin may commerce across the clock, however its liquidity does not anymore. The asset that was speculated to grow to be extra resilient after absorbing billions in institutional capital by means of ETFs has as a substitute developed a break up persona, one that appears deep and orderly throughout New York buying and selling hours and significantly extra fragile as soon as Wall Avenue’s desks go darkish.

Recent information from Kaiko printed this week quantifies what many merchants have felt for some time: the identical ETF-driven maturation that deepened Bitcoin’s weekday market has hollowed out its weekend buying and selling, making a two-tier buying and selling surroundings the place smaller members soak up a disproportionate share of danger.

Since spot Bitcoin ETFs launched in January 2024, institutional participation has concentrated throughout US weekday classes, pushing the share of buying and selling quantity occurring in these hours to roughly 47%, in keeping with Kaiko’s evaluation.

Weekday volumes now constantly run at double weekend ranges, a niche that has widened all through 2025 and into 2026 as institutional allocations have grown. The promise of a uniform 24/7 market, the characteristic that was supposed to tell apart crypto from every little thing else in finance, is weakening in observe as a result of Bitcoin continues to be open each Saturday and Sunday, whereas the capital that gives its depth is not.

BTC nonetheless trades 24/7, however critical liquidity is turning into extra selective

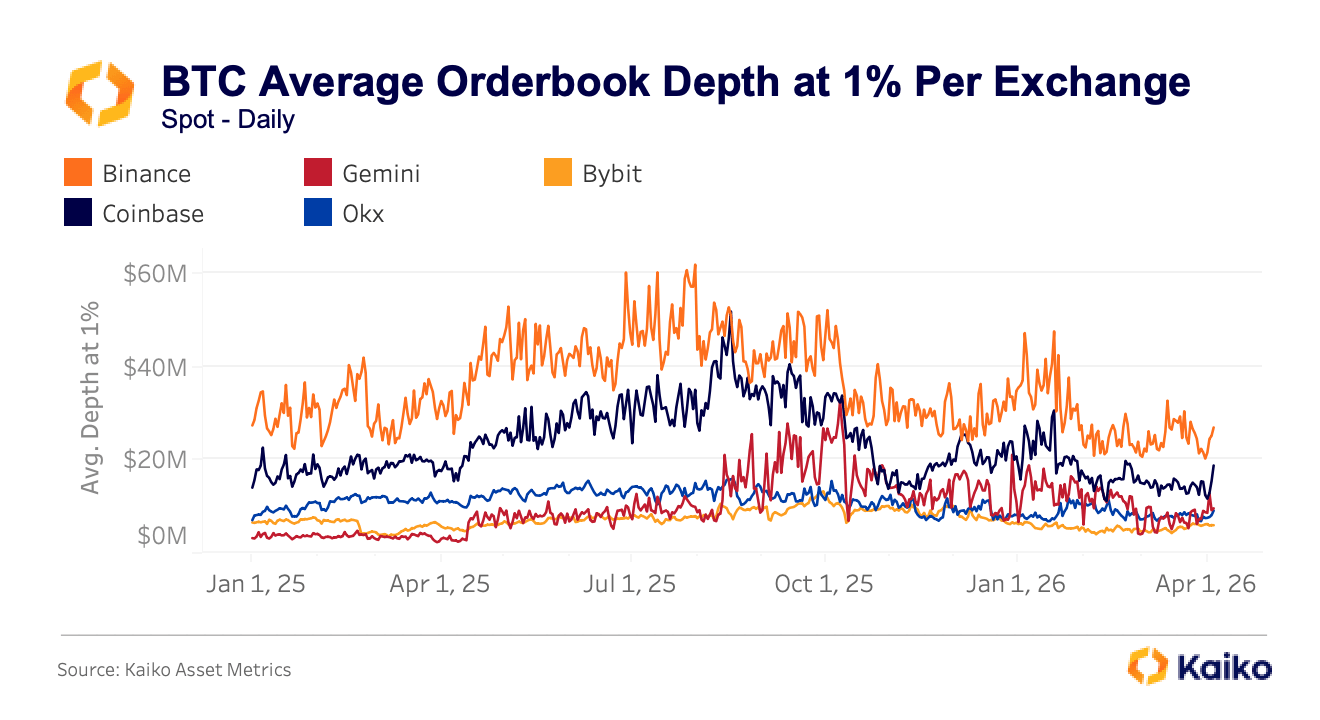

The shift is seen in what merchants name orderbook depth, the whole greenback worth of purchase and promote orders sitting inside a given distance of the present worth. It is an essential measure of liquidity, because it features as a tough measure of how a lot promoting or shopping for a market can soak up earlier than the value begins shifting towards you.

Kaiko tracks depth at 1% from the midpoint, which means all of the resting orders inside one % above and beneath the present Bitcoin worth, and that determine varies enormously relying on the place you commerce. Binance constantly offers round $30 million in depth at that stage, whereas Coinbase ranges between $16 million and $20 million.

Secondary exchanges, together with Gemini, Bybit, and OKX, sometimes present $10 million to $15 million in quantity, producing a two-to-three-times differential that interprets instantly into worse costs for anybody putting a significant order on the improper platform.

That differential does not stay secure beneath stress, and actually, it tends to blow out nearly precisely when it might be costliest. Through the tariff-driven sell-off final October, BTC spot costs diverged materially throughout venues inside minutes, with Binance quoting $102,318, OKX exhibiting $102,142, and Bybit lagging at $101,675, a $643 unfold that continued for a number of minutes moderately than the seconds one would count on if the same old automated arbitrage mechanisms have been closing gaps effectively.

The sample repeated throughout March 2026’s geopolitical escalation within the Center East, when the price of buying and selling BTC-USDT on Bybit surged 230% from its regular stage, with comparable spikes on OKX and Binance. Each episodes started on weekends, when institutional members had already stepped away, and order books have been at their thinnest.

When Wall Avenue closes, the hole between “the value” and your worth can widen quick

This has some very actual and tangible penalties. On Feb. 1, Bitcoin worth plunged beneath $78,000 on a Saturday afternoon, triggering roughly $2.2 billion in liquidations throughout greater than 335,000 merchants inside 24 hours.

The drawdown was amplified by structurally skinny weekend liquidity moderately than by any crypto-specific elementary breakdown, which means the market wasn’t responding to unhealthy information about Bitcoin a lot as to the mechanical actuality that fewer members have been current to soak up promoting strain.

A subsequent VanEck evaluation of the broader February sell-off discovered that Bitcoin’s single-day worth transfer on Feb. 5 ranked among the many quickest crashes within the asset’s recorded historical past by statistical measures of velocity and magnitude, the sort of excessive occasion that likelihood fashions would predict nearly by no means happens, but has now surfaced twice in 5 months.

A dealer shopping for or promoting on a Saturday night, or on any secondary venue throughout elevated volatility, might not obtain something near the consensus Bitcoin worth they consider they’re transacting at.

The hole between the quoted worth and the executed worth tends to widen when the implications of a foul fill are most extreme, and that asymmetry falls hardest on the members who lack the institutional infrastructure to attend for higher situations.

Whereas retail merchants clearly nonetheless take part in crypto, Kaiko’s analysis suggests they have been pushed into the thinner, much less protected elements of it. By way of time, retail is extra uncovered throughout off-hours and weekends, the intervals when ETF flows are inactive and institutional market-making retreats.

By way of geography, retail stays dominant in markets that do not resemble the US ETF-driven Bitcoin commerce in any respect, with South Korea persevering with to run closely on retail participation and altcoin quantity whereas Turkey’s crypto exercise displays macro-stress hedging and stablecoin demand moderately than the institutional exercise we have seen surge within the US.

There’s additionally an asset dimension to the break up.

Institutional capital, channeled by means of ETFs and prime brokerage preparations, has standardized Bitcoin buying and selling greater than anything in crypto, concentrating subtle market-making and deep liquidity round BTC, leaving the remainder of the panorama (altcoins, local-currency pairs, smaller platforms) with thinner protection and fewer skilled assist. Speculative and fragmented exercise persists in abundance throughout the broader market, simply not in the identical exchanges and hours that establishments have colonized.

Identical Bitcoin, completely different market high quality

What emerges from this information is one thing that is more and more troublesome to disclaim: there might now be two Bitcoin markets working in parallel. A deeper, extra environment friendly, institution-shaped weekday market accessible by means of ETFs and prime venues, and a thinner, extra risky off-hours market the place smaller merchants usually tend to be current and extra more likely to bear the price of poor execution.

In concept, Bitcoin is identical asset for everybody, however in observe, the standard of the market you encounter relies upon closely on while you commerce and the place you commerce.

None of that is an argument that ETFs broke Bitcoin. Institutional participation has introduced actual advantages, together with deeper combination liquidity, tighter common spreads throughout regular situations, and a level of legitimacy that not one of the earlier cycles had.

Cumulative web inflows into US spot Bitcoin ETFs nonetheless sit round $53 to $54 billion since launch, even after heavy outflows in early 2026, and so they’ve absorbed monumental capital and survived real volatility with out collapsing.

However the identical forces that improved Bitcoin’s finest hours seem to have uncovered how uneven the market turns into when that participation recedes, delivering maturity for some classes whereas leaving fragility in others.