BlackRock’s 2026 chairman’s letter positions the digital pockets as asset administration’s subsequent main distribution frontier.

Within the letter, Larry Fink writes that “right this moment, there’s little or no entry to conventional funding merchandise in digital wallets” and that BlackRock plans to “lead the cost” in altering that.

Numbers again the assertion: BlackRock says it already has almost $150 billion in AUM linked to digital property, together with $65 billion in stablecoin reserves and almost $80 billion in digital asset ETPs.

Fink describes wallets as an underbuilt distribution channel for mainstream investing, one the place BlackRock sees a structural hole and plans to maneuver.

His imaginative and prescient is {that a} single regulated digital pockets may maintain ETFs, digital euros, tokenized bonds, and fractional pursuits in property like infrastructure and personal credit score.

From rhetoric to infrastructure

What provides this credibility is that BlackRock already operates throughout significant items of the stack.

The agency’s Circle Reserve Fund, which holds nearly all of USDC’s reserve property, stood at $68.167 billion as of Mar. 20, already above the $65 billion determine within the letter.

BlackRock’s BUIDL tokenized Treasury fund sat at over $2 billion as of Mar. 23, deployed throughout eight blockchain networks. Each are reside, scaling positions with actual AUM behind them.

In February, Uniswap Labs and Securitize introduced that BUIDL can be tradable by UniswapX, with Securitize managing allowlisted investor entry and compliance.

BlackRock’s head of digital property, Robert Mitchnick, described it as a significant step towards interoperability between tokenized dollar-yield funds and stablecoins.

The structure is a BlackRock product publicity transferring alongside crypto-native rails, cleared by a regulated compliance layer.

Fink connects the pockets argument to a broader distribution thesis developed elsewhere within the letter. He factors to India, the place JioBlackRock introduced in additional than 1,000,000 buyers in beneath a 12 months, as a mannequin for smartphone-native entry to capital markets.

He writes that half the world already carries a digital pockets on their telephone. The pockets passage reads as an extension of that logic, for the reason that telephone is already within the person’s hand, and the subsequent step is to make monetary merchandise accessible by it.

RWA.xyz exhibits the tokenized US Treasury market at roughly $12 billion as of Mar. 23, with complete stablecoin worth at roughly $317 billion.

The on-chain money layer and the tokenized asset layer are actually giant sufficient to operate collectively as a distribution system.

Fink frames tokenization as an replace to market plumbing, a option to make investments simpler to concern, commerce, and entry throughout conventional and digital markets working facet by facet.

That framing positions BlackRock’s pockets ambition inside a mainstream modernization story, and the agency’s personal AUM figures again it up.

What the pockets thesis truly means

Probably the most direct learn of what wallet-native BlackRock merchandise appear to be in follow begins with tokenized money and Treasury publicity.

That’s the place the agency already has reside scale and the place the market already has traction.

Franklin Templeton’s Benji platform affords a concrete precedent. They provide a cell utility by which buyers can purchase, promote, and look at tokenized fund positions, with yield distributed on to their wallets and tokens transferable peer-to-peer.

The subsequent layer is wallet-accessible ETF or fund share wrappers. Fink names ETFs explicitly as one thing a regulated digital pockets may carry.

BlackRock manages nearly $80 billion in digital asset ETPs, giving it each the product infrastructure and the regulatory expertise to increase that floor space towards pockets supply.

Past that, the longer-dated path Fink sketches is fractional entry to personal markets, distributed by pockets interfaces to buyers who at the moment attain these merchandise solely by advisers and excessive minimums.

| Product layer | What it may appear to be in a pockets | Why it’s believable |

|---|---|---|

| Tokenized money / Treasury publicity | Pockets-accessible yield merchandise, tokenized Treasury funds | BlackRock already has BUIDL and stablecoin-reserve scale |

| ETF / fund-share wrappers | Regulated pockets entry to acquainted public-market merchandise | Fink explicitly names ETFs as one thing digital wallets may maintain |

| Personal-market publicity | Fractional pursuits in infrastructure or non-public credit score | Fink explicitly factors to tokenized private-market entry as a part of the top state |

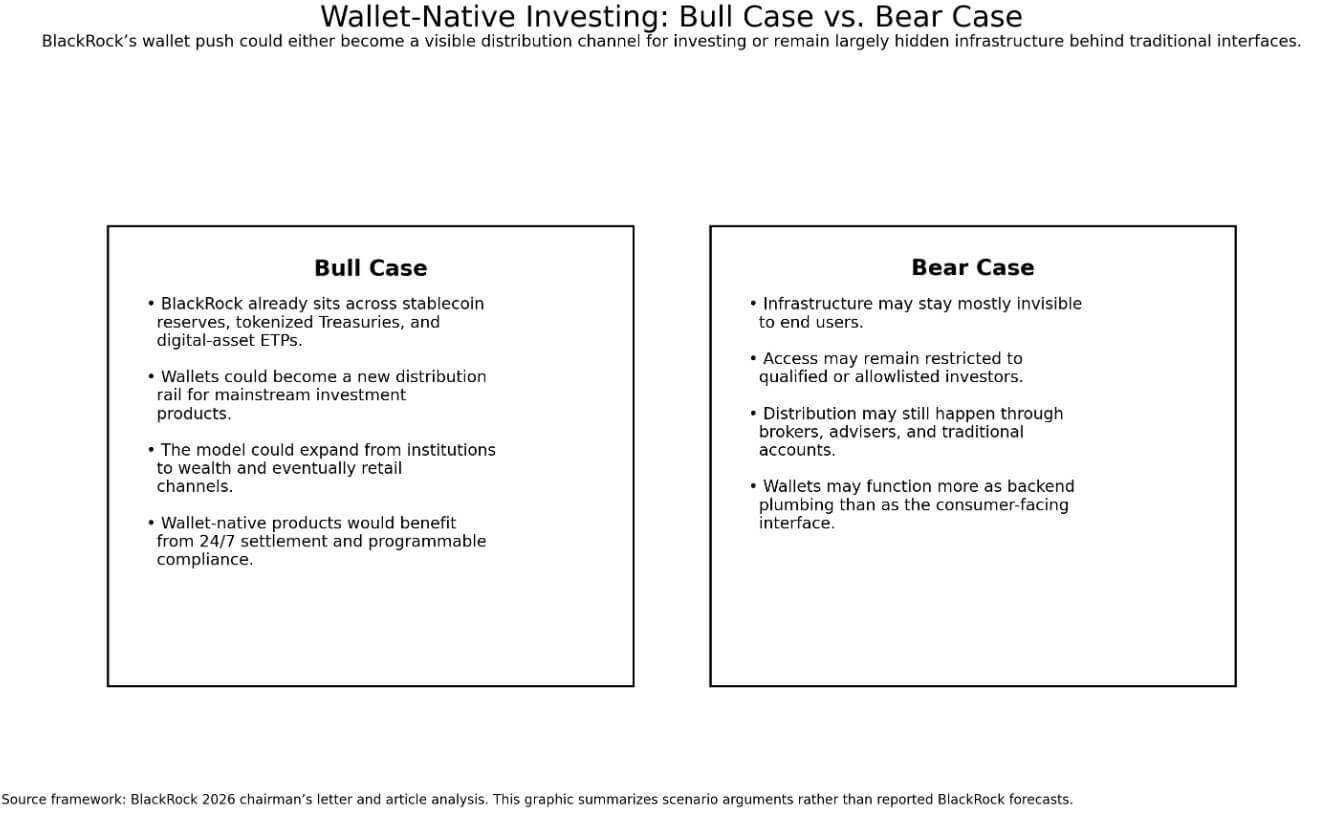

The bull case rests on the distribution scale, as BlackRock is already current at three factors within the digital monetary stack: backing the biggest greenback stablecoin’s reserve, inside the biggest tokenized Treasury fund, and managing the biggest pool of digital asset ETPs.

If the agency makes use of that infrastructure as a basis to push wallet-accessible merchandise into wealth and, ultimately, retail channels, it may speed up the timeline for mainstream wallet-native investing.

Fink’s language round ETFs, non-public credit score, and broader investor entry factors instantly factors down that path.

The bear case facilities on infrastructure staying invisible to finish customers. BlackRock expands tokenization, settlement infrastructure, and stablecoin interoperability, however on a regular basis buyers proceed to expertise these enhancements by brokers, advisers, and conventional account interfaces.

The present BUIDL construction factors in that route: US-qualified purchasers solely, $5 million minimal, allowlisted entry.

That’s institutional plumbing operating on on-chain structure, nonetheless effectively upstream of a shopper distribution product.

The letter emphasizes modernization and coexistence with conventional markets. The language is per gradual infrastructure enchancment.

What the letter doesn’t resolve

The chairman’s letter leaves essentially the most operationally particular questions open.

There is no such thing as a launch date, no named pockets product, no specified blockchain rail, and no clear assertion on whether or not BlackRock’s pockets ambition targets institutional counterparties, wealth channel shoppers, or mass retail.

“Lead the cost” alerts a strategic route whereas the product particulars stay unannounced.

What the letter establishes is that BlackRock has moved from observing tokenization to working inside it at scale, and that Fink now sees the distribution hole in digital wallets because the agency’s subsequent addressable downside.

Whether or not the product that closes that hole appears to be like like a regulated tokenized Treasury wrapper accessible by a fintech associate or one thing nearer to a self-custody funding account stays open.

The reply to this can seemingly outline the subsequent section of BlackRock’s digital asset story.

If BlackRock succeeds in making wallets a distribution rail for conventional funding merchandise, the aggressive benefit of crypto-native infrastructure shifts towards settlement finality, programmable compliance, and 24/7 market entry. These properties make pockets supply of regulated merchandise possible within the first place.