For many of the previous two years, debate about stablecoins in funds has targeted on the checkout display screen: will shoppers ever faucet a pockets as a substitute of a card?

Visa, Stripe, and Mastercard have answered with their capital. Visa now settles in USDC, Stripe purchased Bridge, and Mastercard is buying BVNK.

Every transfer displays the identical learn that stablecoins have gotten the settlement and liquidity layer beneath current manufacturers, and whoever controls that layer controls the economics of the following fee cycle.

Chainalysis put adjusted stablecoin quantity at $28 trillion in 2025 and projected it may attain $719 trillion by 2035 on natural progress, with a extra aggressive situation approaching $1.5 quadrillion.

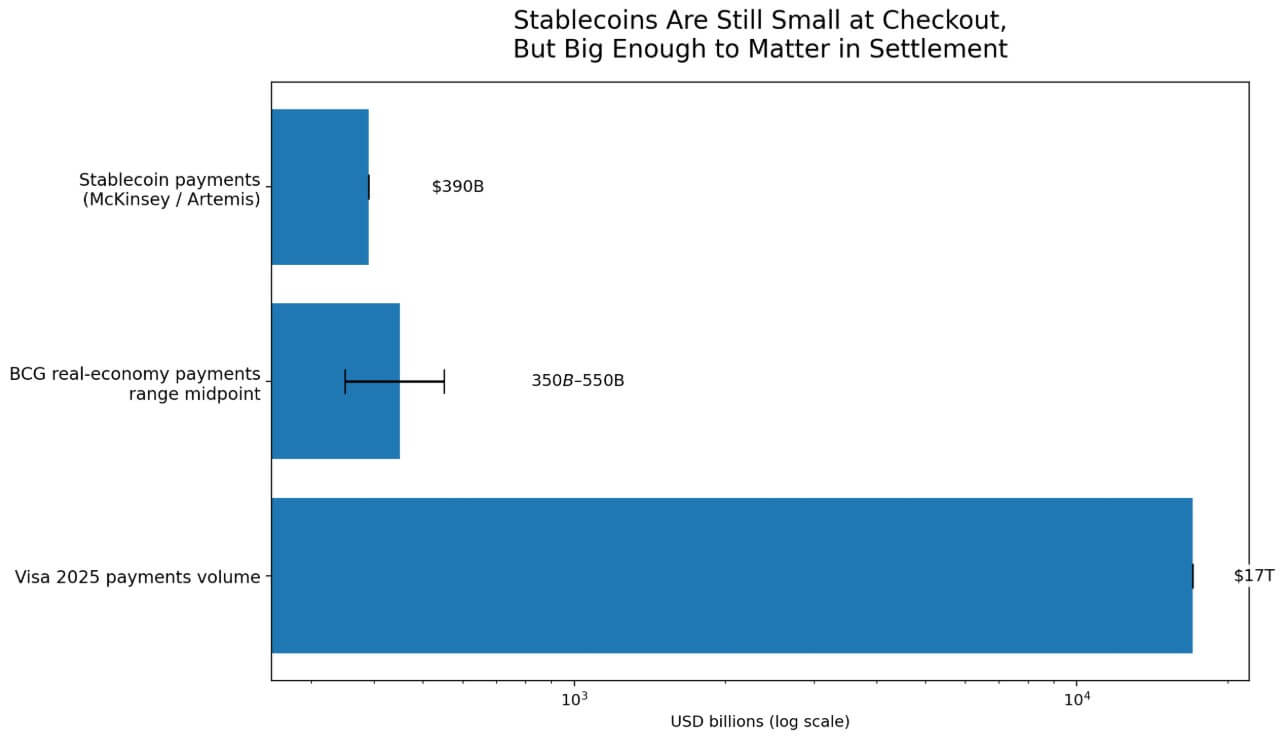

The grounding comes from McKinsey and Artemis, which estimate precise stablecoin funds at about $390 billion yearly, a determine corroborated by BCG’s $350-$550 billion vary, excluding non-economic and buying and selling flows.

At these ranges, stablecoins signify roughly 2.3% of Visa’s $17 trillion in funds quantity in 2025.

Stablecoins can reprice settlement economics at 2.3% penetration as a result of settlement and checkout function on separate infrastructure.

Many hybrid stablecoin fee flows by no means seem as on-chain service provider transactions. Crypto card transactions sometimes execute on conventional card rails, whereas the blockchain captures solely issuer inflows and outflows.

A stablecoin settlement layer can develop commercially with out ever changing into seen on the level of sale.

Three bets on the identical stack

Visa launched USDC settlement within the US in December 2025. By Mar. 25, its international stablecoin settlement exercise had reached an annualized run fee of $4.6 billion throughout greater than 130 stablecoin-linked card applications in additional than 50 nations.

Visa’s personal framing centered on treasury modernization and settlement effectivity, as its Canton Community effort prolonged that logic into fee, settlement, and treasury use circumstances for banks, a deliberate push to personal the orchestration layer for institutional stablecoin flows.

By March 2026, Bridge-enabled stablecoin-linked playing cards had gone reside in 18 nations, with plans to achieve 100-plus by year-end, and Visa was evaluating settlement optionality, quicker fund motion, and simplified blockchain abstraction for establishments.

Stripe’s 2025 annual letter, revealed Feb. 24, reported stablecoin funds quantity doubled to round $400 billion, with an estimated 60% in B2B flows, whereas Bridge quantity greater than quadrupled.

Bridge had received conditional OCC approval for a nationwide belief financial institution protecting custody, issuance, orchestration, and reserve administration.

Mastercard’s March 2026 settlement to amass BVNK for as much as $1.8 billion got here alongside an announcement that digital foreign money fee use circumstances had already reached no less than $350 billion in 2025, with the incremental alternative in cross-border remittances, payouts, peer-to-peer transfers, and B2B funds.

Mastercard additionally cited pace and programmability as solutions to treasury administration and business circulation ache factors.

Three corporations, three merchandise, and M&A methods, one shared thesis: stablecoin settlement is embedding itself into fee infrastructure earlier than any consumer-visible checkout revolution arrives.

| Firm | Transfer | What the transfer says | Major use circumstances | Doubtless management level |

|---|---|---|---|---|

| Visa | USDC settlement within the U.S.; 130+ stablecoin-linked card applications throughout 50+ nations; Canton Community push | Stablecoins are being handled as a settlement and treasury modernization layer, not only a checkout experiment | Service provider settlement, treasury operations, card-issuing orchestration, institutional settlement | Settlement + orchestration layer |

| Stripe / Bridge | Stripe acquired Bridge; stablecoin quantity round $400B in 2025; estimated 60% B2B; trust-bank path for custody, issuance, orchestration, and reserves | Stripe is constructing enterprise-grade stablecoin infrastructure for enterprise flows, not retail-only crypto funds | B2B funds, developer APIs, custody, issuance, reserve administration, enterprise infrastructure | Developer/compliance stack |

| Mastercard / BVNK | Mastercard agreed to amass BVNK; digital-currency fee use circumstances at $350B+ in 2025 | Mastercard sees stablecoins as a strategy to improve cross-border and business cash motion whereas preserving fiat connectivity | Cross-border remittances, payouts, P2P, B2B funds, treasury/business flows | Hall distribution + business flows |

The Federal Reserve confirmed in an Apr. 8 notice that stablecoin market capitalization reached $317 billion as of Apr. 6, up greater than 50% since early 2025.

Congress enacted the GENIUS Act in July 2025, supplying the formal US authorized framework that institutional adoption requires.

Citi’s September 2025 base case put stablecoin issuance at $1.9 trillion by 2030, supporting roughly $100 trillion in annual transaction exercise, and projected greater than $1 trillion in incremental demand for US Treasuries at that scale.

At $317 billion in present capitalization, the stablecoin market is about 16.7% of Citi’s 2030 goal, which is much sufficient alongside that the biggest fee networks have dedicated capital, but early sufficient that the result stays open.

What to anticipate

The bull case activates how briskly compliance infrastructure can take up stablecoin settlement at enterprise scale.

Regulatory readability arrived by way of the GENIUS Act, with Visa and Bridge concentrating on 100-plus nations by year-end. Stripe and Bridge are constructing towards regulated custody and reserve administration.

If enterprises can deal with stablecoin settlement as routine treasury operations, cross-border payouts, service provider settlements, and B2B flows will migrate to on-chain rails quicker than any single forecast can seize.

In that setting, Citi’s $1.9 trillion issuance projection turns into a flooring, and the companies that personal orchestration, compliance, reserves, and interoperability requirements seize the structural economics of the brand new stack.

The bear case requires open stablecoin rails to stay fragmented lengthy sufficient for incumbents to soak up the performance as a proprietary function.

The Fed’s April 2026 notice flagged extra advanced intermediation chains, vertical integration, opacity, and run danger as vulnerabilities that push regulated establishments towards permissioned alternate options.

Citi’s personal evaluation means that bank-issued tokenized cash may exceed open stablecoins in institutional quantity, with adoption anchored in company treasuries and capital markets, the place compliance necessities favor closed networks.

In that consequence, stablecoins proceed to develop, whereas the financial advantages accrue to regulated, permissioned programs. Incumbents deploy stablecoins as a function, and the plumbing stays proprietary.

| Situation | What occurs | Who captures the economics | What it means for funds |

|---|---|---|---|

| Bull case | Stablecoin settlement turns into routine for treasury, cross-border payouts, service provider settlement, and B2B flows | Visa, Stripe/Bridge, Mastercard, and compliant infrastructure suppliers | Stablecoins develop into a default back-end rail beneath current fee manufacturers |

| Base case | Stablecoins develop steadily in chosen corridors and enterprise workflows, however checkout stays principally unchanged | Incumbents plus a handful of infrastructure specialists | A hybrid system emerges: playing cards and banks on the entrance finish, stablecoins more and more beneath |

| Bear case | Open stablecoin rails keep fragmented; incumbents take up stablecoin performance as a proprietary function | Regulated incumbents and permissioned-network operators | Stablecoins nonetheless develop, however principally inside closed or semi-closed programs |

| Management-point battle | Orchestration, compliance, reserves, FX administration, and interoperability requirements develop into decisive | Whoever owns the back-end stack somewhat than the checkout display screen | The important thing query shifts from who owns the cardboard to who owns cash motion |

The management factors

Visa, Stripe, and Mastercard are every working for various segments of the back-end stack: Visa by way of settlement and card-issuing orchestration, Stripe and Bridge by way of developer APIs, B2B infrastructure, and controlled custody, and Mastercard by way of cross-border corridors, remittances, and business treasury.

Their positioning displays a shared learn that the decisive contest runs by way of orchestration, compliance, reserves, overseas change administration, and interoperability requirements.

Chainalysis initiatives stablecoin transaction volumes may intersect Visa and Mastercard off-chain volumes between 2031 and 2039. The extra consequential inflection preceded that projection by years.

The biggest card networks started redesigning their settlement and payout infrastructure round stablecoins whilst stablecoins accounted for lower than 3% of worldwide fee flows.

The companies that construct essentially the most defensible positions in orchestration and compliance over the following 36 months will decide who captures the economics of that intersection.