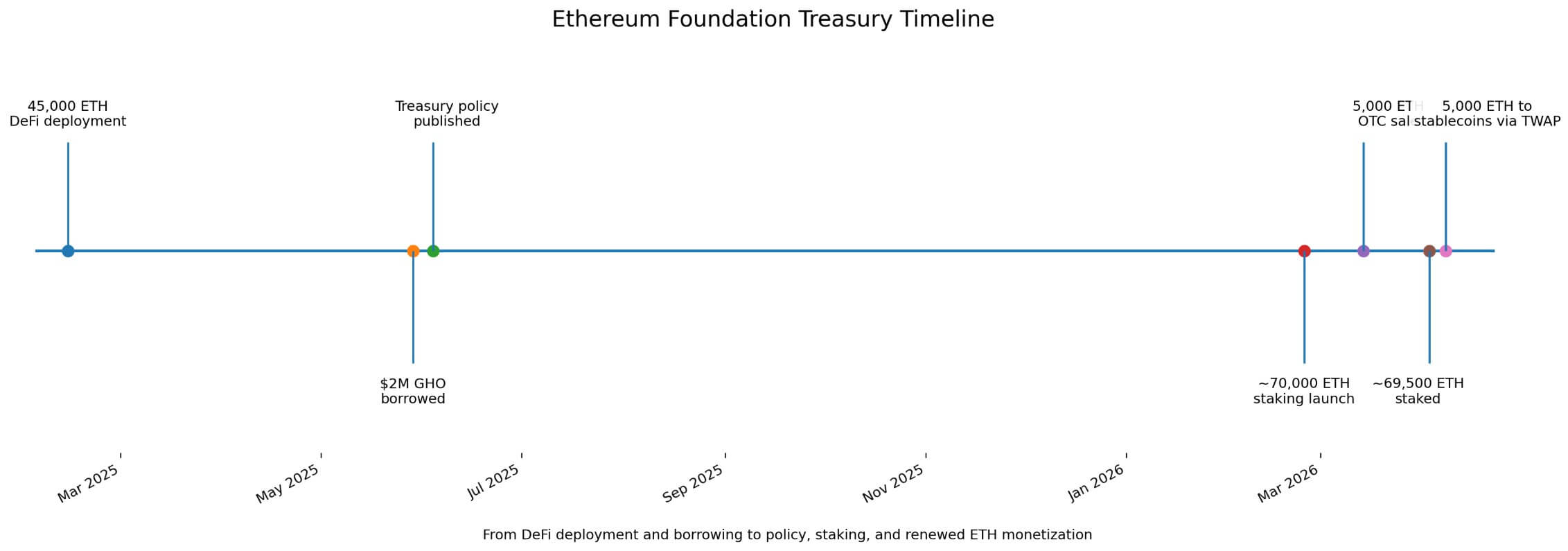

The Ethereum Basis (EF) introduced on Apr. 8 that it might convert 5,000 ETH into stablecoins by CoWSwap’s TWAP characteristic to fund analysis, grants, and donations.

The announcement reopened a debate over what the muse’s treasury overhaul was ever meant to perform. During the last yr, EF moved treasury property into DeFi, borrowed towards ETH collateral, after which launched a staking initiative centered on about 70,000 ETH.

The truth described in EF’s June 2025 treasury coverage instructed a special mannequin. It tied monetization to a fiat-denominated working buffer and saved ETH gross sales, staking, and stablecoin borrowing inside the identical treasury framework.

On Feb. 13, 2025, EF Treasury stated it had deployed 45,000 ETH throughout Spark, Aave Prime, Aave Core, and Compound. On Could 29, it borrowed $2 million in GHO towards its Aave place.

The transfer carried symbolic weight as a result of it confirmed EF utilizing DeFi rails to lift working capital with out promoting spot ETH.

By early April, that interpretation had filtered into retail discourse, as a Reddit submit argued that EF was “now not promoting.” One commenter replied that “it’s good that they stopped promoting.”

Regardless of anecdotal proof, this type of chatter reveals how the stronger model of the thesis had already entered circulation earlier than EF introduced the Apr. 8 conversion.

The promoting continues

As EF launched its staking initiative on Feb. 24, it stated it might stake 70,000 ETH, with rewards routed again to the treasury.

On Mar. 14, it finalized a 5,000 ETH OTC sale to BitMine at a median value of $2,042.96. On Apr. 3, on-chain exercise pushed the staked complete to roughly 69,500 ETH, near the goal. Then got here the Apr. 8 CoWSwap conversion, highlighting that promoting and staking had already been working facet by facet for weeks.

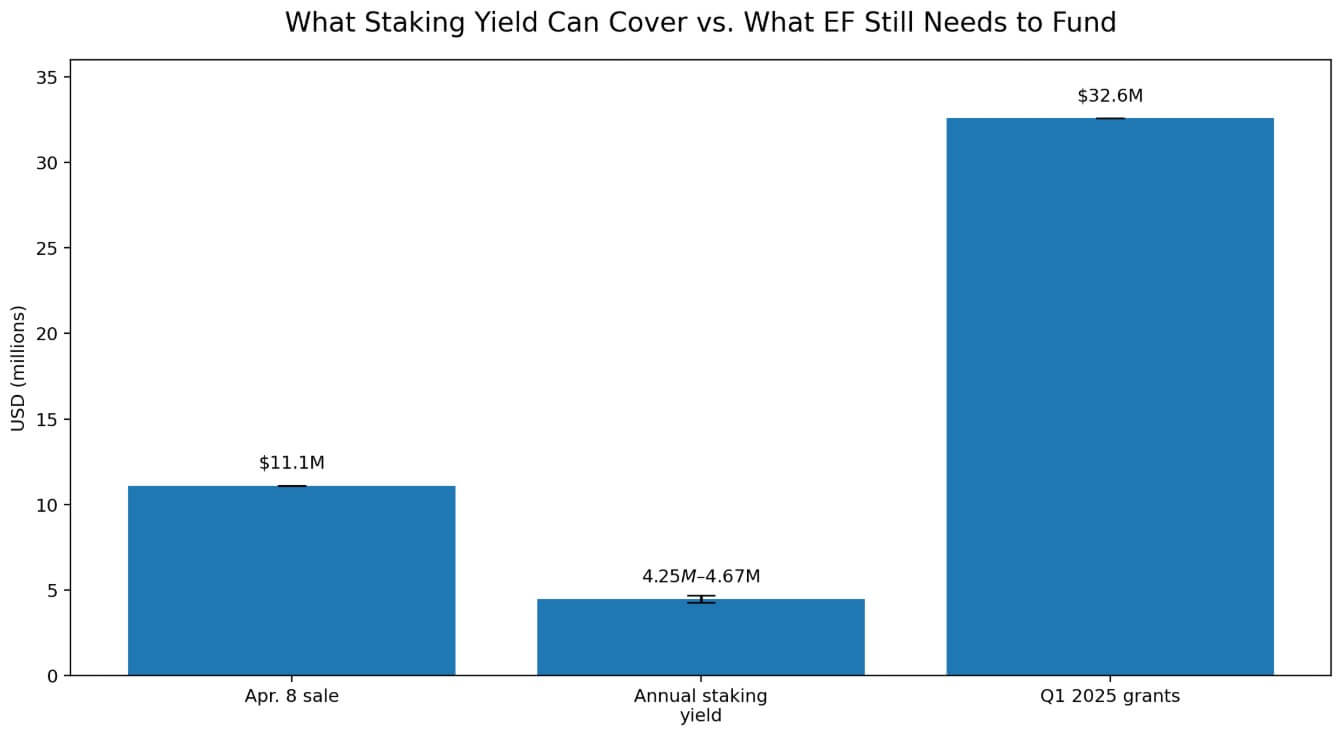

At an ETH value round $2,220.76, a 5,000 ETH conversion equals about $11.1 million, whereas ETH staking reference charges in early April sat round 2.73% to three.00%.

Utilized to 70,000 ETH, that produces roughly 1,912 to 2,102 ETH a yr, price about $4.25 million to $4.67 million at present costs. A single 5,000 ETH sale equals about 2.4 to 2.6 instances the full-year yield from all the 70,000 ETH staking sleeve.

The staking program improves treasury effectivity and reduces funding necessities, but it surely stays nicely under the dimensions wanted to switch treasury gross sales.

The EF June 2025 framework set annual opex at 15% of treasury and the working buffer at 2.5 years, which means a fiat-denominated reserve equal to 37.5% of treasury.

Utilized solely as an illustration to EF’s final full treasury snapshot, the Oct. 31, 2024, report confirmed $970.2 million in complete treasury and $181.5 million in non-crypto property, implying a coverage goal reserve of about $363.8 million.

EF had already publicly added stablecoin publicity after that snapshot, deploying 2,400 ETH and about $6 million in stablecoins into Morpho in October 2025, and it later introduced further ETH-to-stablecoin conversions in October 2025 and April 2026.

The precise present dimension of EF’s fiat-like bucket and whether or not tokenized RWA holdings have already been added in materials dimension are nonetheless unknown. So the 2024 snapshot ought to nonetheless be handled as illustrative slightly than as a stand-in for as we speak’s steadiness sheet.

EF’s personal allocation replace confirmed $32.6 million in grants for the primary quarter of 2025. At as we speak’s ETH value, that equals roughly 14,700 ETH. The Apr. 8 conversion covers solely about 33% of that quarter’s grant complete, excluding protocol analysis, staffing, operations, and broader trade help.

Yield and borrowing depart the fiat-denominated price range intact and nonetheless require periodic monetization.

Potential outcomes

The bull case for EF rests on easy treasury arithmetic, as a better ETH value and a decrease long-run opex ratio would enable the muse to keep up its greenback buffer whereas monetizing fewer cash.

| State of affairs | What adjustments | Possible treasury impact |

|---|---|---|

| Bull case | ETH value rises, long-run opex ratio falls | Fewer cash must be offered to keep up fiat buffer |

| Base case | Blended technique continues | Staking, DeFi, borrowing, and periodic gross sales coexist |

| Bear case | ETH value weakens, spending stress rises | Extra ETH could must be monetized to protect runway |

| Key implication | Reserve goal stays fiat-denominated | “Much less promoting” narrative breaks down if ETH falls |

In that setting, staking rewards and selective borrowing can scale back quarterly gross sales and provides EF extra flexibility round venue alternative, whether or not by OTC blocks, TWAP execution, or conservative DeFi positions.

Treasury modernization would then present up in decrease cadence, smaller clips, and higher execution.

The bear case runs by the identical framework in reverse, as EF’s reserve goal is denominated in fiat phrases.

A weaker ETH value can pressure extra monetization to protect runway, particularly if the muse leans into its counter-cyclical mandate and spends extra aggressively throughout more durable market circumstances.

Underneath that setup, a big staking sleeve nonetheless generates yield, however the reserve requirement can rise sooner than that yield offsets it.

Public expectations constructed round “much less promoting” then collide with the balance-sheet self-discipline EF had already written into coverage.

The Apr. 8 conversion introduced that self-discipline again into view. EF’s treasury technique had already mixed DeFi deployment, stablecoin borrowing, staking, and periodic ETH gross sales.

The market narrative prolonged past the written coverage and past the muse’s personal post-staking transaction report.