Citadel Securities’ newest SEC submitting and Blockchain Affiliation’s response expose one thing extra consequential: an early public battle over the actual prize in tokenized shares. Wall Avenue’s purpose is to stay indispensable when equities develop into tokenized.

The institution’s place on tokenization has moved quicker than most observers anticipated. Citadel Securities says it welcomes tokenization as a result of it may enhance outcomes for traders and issuers, together with effectivity in clearing and settlement and shareholder engagement.

Nasdaq unveiled an fairness token design in March, explicitly designed to protect regulated market infrastructure, maintain public corporations on the heart of possession information, and combine blockchain into the official share registry.

SIFMA informed Congress that tokenized securities can improve market infrastructure, investor entry, and capital formation.

Even the SEC is treating tokenized shares as a stay coverage class: Commissioner Hester Peirce stated in March that workers is engaged on a narrower innovation exemption for restricted buying and selling of sure tokenized securities.

Moreover, Chairman Paul Atkins stated market contributors ought to be capable of have interaction with decentralized functions on public, permissionless blockchains in the event that they need to.

That convergence makes the actual dispute tougher to caricature as outdated finance versus crypto, as conventional corporations favor tokenization. The controversy is over whether or not blockchain is deployed inside present management buildings or in ways in which scale back them.

The authorized battle behind the coverage argument

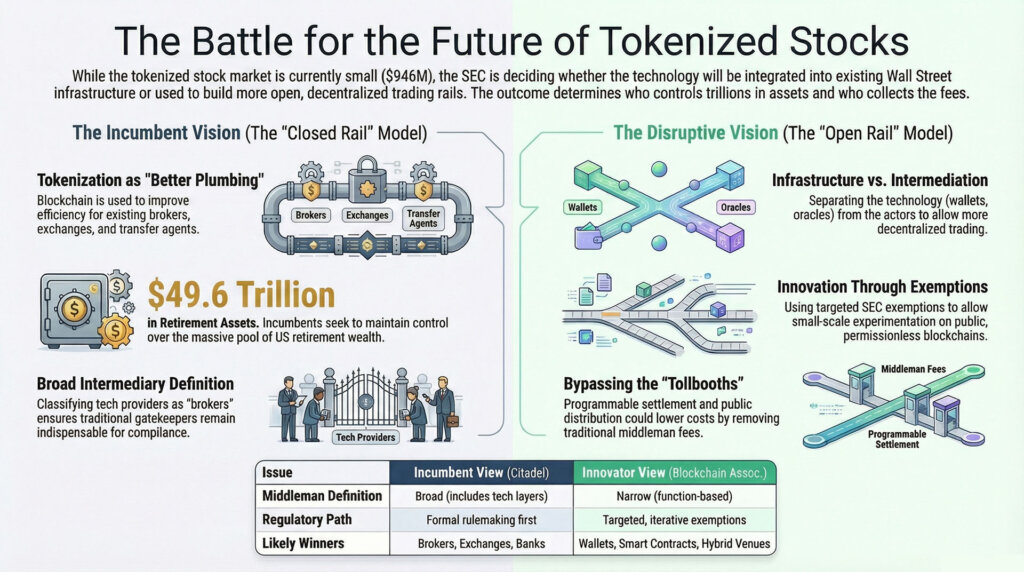

Citadel Securities’ core place is that the SEC ought to determine the intermediaries concerned in tokenized fairness buying and selling, keep away from broad exemptive aid from the alternate and broker-dealer definitions, and proceed by notice-and-comment rulemaking somewhat than focused exemptions.

Its supporting argument, sharpened by economist James Overdahl’s evaluation, is that broad aid dangers constructing a parallel regulatory regime with weaker investor protections and extra fragmented liquidity.

Blockchain Affiliation’s (BA) response says securities legal guidelines regulate actors performing coated market features, resembling brokers, sellers, and exchanges, and that Citadel Securities’ framing would stretch these classes to incorporate validators, entrance ends, wallets, liquidity suppliers, oracle suppliers, and builders in ways in which conflate infrastructure with intermediation.

BA additionally argues the SEC has a protracted historical past of utilizing no-action aid and focused exemptions earlier than formalizing guidelines, and that forcing tokenized equities by a full rulemaking cycle whereas the market continues to be small successfully advantages incumbents by conserving experimentation inside present pipes.

Intermediaries are the place the economics of routing, custody, market-making, settlement, and compliance converge. The regulatory definition of who counts as a intermediary determines who will get paid and who will get squeezed.

| Subject | Citadel Securities / incumbent view | Blockchain Affiliation view | What it means in observe |

|---|---|---|---|

| Who counts as middleman | Broad studying | Narrower, function-based studying | Determines who should register |

| Regulatory path | Rulemaking first | Focused exemptions / iterative aid | Determines pace of rollout |

| Market construction consequence | Tokenization inside present rails | Room for extra open rails | Decides whether or not middlemen maintain management |

| Doubtless winners | Brokers, exchanges, switch brokers | Wallets, interfaces, hybrid venues | Decides who captures charges |

| Important acknowledged concern | Investor safety / fragmentation | Class overreach / innovation delay | Competing theories of market security |

If the SEC adopts Citadel Securities’ broader middleman logic, tokenized shares land as higher plumbing wrapped round acquainted gatekeepers: the broker-dealer stack, alternate infrastructure, and switch brokers all maintain their place.

If the SEC leans towards BA’s infrastructure-versus-intermediation distinction, a few of that worth turns into obtainable to wallets, sensible contract venues, and public-chain distribution.

The present tokenized inventory market gives a concrete backdrop for that coverage selection.

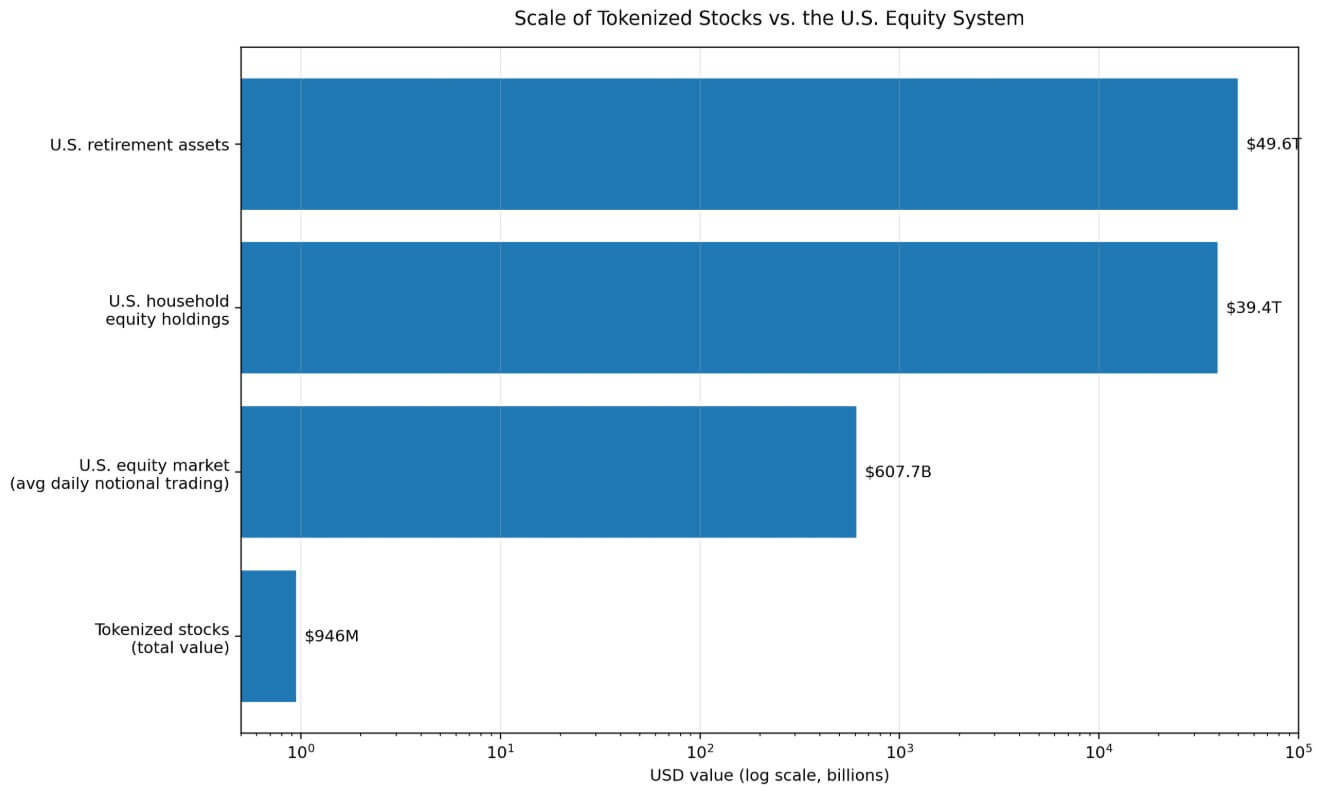

RWA.xyz lists tokenized shares with a complete worth of $946 million and a month-to-month switch quantity of $2.86 billion as of March, throughout 203,630 holders.

That whole sits effectively beneath the US fairness market, which SIFMA’s 2025 Truth Ebook reveals averaged $607.7 billion in every day notional buying and selling in 2024, towards US family fairness holdings of roughly $39.4 trillion and whole retirement belongings of $49.6 trillion.

Policymakers are designing the structure of a tiny market at the moment.

McKinsey’s 2024 tokenization outlook argues that publicly traded equities are a later-wave asset class exactly due to regulatory complexity, that means the principles written now will decide who captures that wave as soon as it arrives.

The bullish case

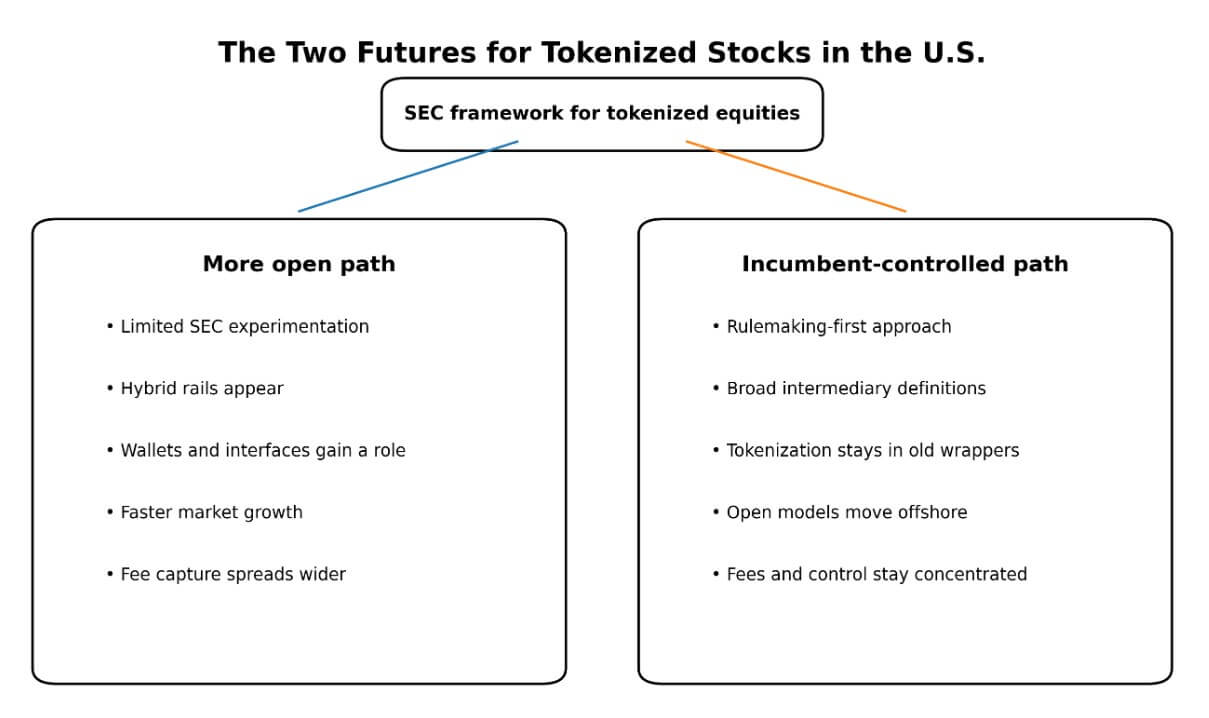

If the SEC permits restricted experimentation with novel platforms whereas nonetheless requiring significant investor protections, at the least some worth migrates away from the incumbent stack.

Dealer-dealers retain a central function whereas wallets, interfaces, and sensible contract venues carry out work that at the moment falls solely inside the scope of licensed intermediaries. Longer buying and selling hours, programmable settlement, and public chain distribution decrease the friction price of fairness possession in ways in which the prevailing dealer structure can not simply replicate.

Atkins’s specific reference to public, permissionless blockchains as a reputable vacation spot for market contributors offers that consequence regulatory backing.

BA’s argument that the SEC can construct a focused, conditional framework by present exemptive authority additionally makes the timeline extra believable.

If the exemption strikes quicker than a full rule, new entrants and new architectures get a window to function earlier than incumbents can totally form the ultimate framework by remark cycles.

The $946 million tokenized inventory market already demonstrates actual switch exercise, indicating that programmability will increase turnover even at a small scale.

As total tokenized RWA markets move $26 billion and draw institutional consideration, tokenized equities in a extra open regulatory setting provide clear upside in each excellent worth and charge economics, bypassing the outdated tollbooths.

Nasdaq’s design, regardless of its incumbent-friendly framing, additionally signifies that main alternate operators view tokenization as a development alternative somewhat than a menace.

An SEC framework that preserves investor protections whereas opening the door to hybrid rails offers even conventional gamers an incentive to construct towards public-chain bridges somewhat than purely closed programs.

That competitors may speed up technological and person expertise enhancements, bringing retail fairness holders onto on-chain rails quicker than present forecasts anticipate.

The bearish case

If the SEC prioritizes formal rulemaking and adopts Citadel Securities’ broader studying of the middleman definitions, tokenized equities largely keep inside the broker-dealer and alternate wrappers.

The person relationship, entry management, compliance layer, and settlement legitimacy keep concentrated in acquainted arms.

Tokenization turns into higher plumbing for a similar construction, with quicker settlement, cleaner shareholder information, and extra environment friendly company actions. The financial distribution of fairness market intermediation stays intact.

The IAC draft provides institutional weight to that consequence.

The SEC Investor Advisory Committee’s market-structure advice says the Fee ought to protect necessary disclosures, regulation, and oversight of intermediaries, and best-execution-style protections, and explicitly opposes a blanket innovation exemption.

If the ultimate framework displays IAC-style warning, essentially the most structurally disruptive variations of tokenized equities, these operating on public, permissionless chains with non-custodial interfaces, keep exterior US regulatory attain.

That regulatory warning carries a second-order consequence that extends past home markets.

If ambiguity round middleman definitions retains the US caught close to the present $946 million tokenized inventory base whereas cleaner frameworks develop offshore, the standard-setting energy over the following era of fairness rails migrates with the experimentation.

Incumbents protect their present place within the quick run, however the US monetary sector loses the design benefit that comes from being the venue the place the structure proves itself at scale.

SIFMA’s argument that tokenized securities ought to combine into the prevailing federal framework can even learn as a slow-roll technique: integration on incumbent phrases, at a rulemaking tempo, with established gamers steering each new structure by remark cycles they know easy methods to navigate.

Nasdaq’s fairness token design illustrates the ceiling of this state of affairs.

A design explicitly constructed to protect issuer management, present regulatory frameworks, and established market safeguards is technologically fascinating and operationally cleaner than at the moment’s infrastructure, with charge and management economics staying concentrated the place they’re.

If that design turns into the dominant US template, then the extra open architectures that might truly reassign middleman economics keep both offshore or theoretical.

The choice level

The arduous a part of the tokenization dialogue is deciding whether or not it modifications who controls the market.

If the SEC solutions that tokenized shares can exist solely inside outdated channels with outdated gatekeepers, then tokenization turns into higher plumbing for a similar construction.

If it leaves room for extra open rails, the largest disruption might be to the corporations that used to take a seat within the center.

The SEC’s energetic work now facilities on whether or not the primary stay US framework preserves the outdated management stack or leaves room to reassign a part of it. That call will decide who captures the fairness token market as soon as it strikes from $946 million to the size that makes the structure everlasting.