Bitcoin’s second-quarter slide unfolded alongside a uncommon contraction within the stablecoin market, including one other signal that crypto liquidity weakened past spot costs alone.

Bitcoin traded under $60,000 in the course of the quarter, reaching its lowest degree since 2024, and fell 14% throughout Q2. On the similar time, complete stablecoin provide slipped to $312 billion, down greater than $3 billion from the earlier quarter, CEX.IO stated in a report shared with CryptoSlate.

The decline marked the primary quarterly drop in stablecoin provide because the third quarter of 2023. The pullback was small in proportion phrases, however it got here because the broader crypto market misplaced 6.2% of its worth.

That lifted stablecoins’ share of complete crypto market capitalization to 14% from 13%, exhibiting that buyers nonetheless held a bigger portion of the market in dollar-linked tokens at the same time as capital left the sector.

Stablecoins are sometimes handled as crypto’s money layer. Merchants use them to maneuver between exchanges, settle transactions, park funds and entry decentralized finance.

Consequently, a decline of their provide doesn’t robotically imply customers are abandoning stablecoins, however it signifies fewer digital {dollars} circulating available in the market at a time when buying and selling, transfers, and speculative exercise have additionally weakened.

Yield merchandise flip right into a drag

The sharpest change got here from yield-bearing stablecoins, which had been one of many stronger components of the market since mid-2023.

After rising each quarter for practically three years, the class fell by greater than $3.5 billion, or 15%, in Q2. The decline reversed a 19% achieve within the first quarter and confirmed how rapidly demand shifted away from crypto-native yield methods as market situations worsened.

Ethena’s sUSDe accounted for a lot of the drop. Its market capitalization fell by 52%, erasing practically $2 billion in market worth. Sky’s sUSDS additionally declined, dropping 16% in the course of the quarter.

These two belongings had helped drive earlier development in yield-bearing stablecoins, however they turned a supply of stress as customers lowered publicity.

Conversely, institutional urge for food for yield shifted towards merchandise backed by real-world belongings (RWAs) and short-term US authorities debt. BlackRock’s BUIDL tokenized fund grew by 2%, whereas different treasury-backed choices like USYC and USDY climbed 16% and 66%, respectively.

The bifurcated efficiency factors to a definite flight to security throughout the stablecoin market itself, with capital migrating from algorithmic and artificial DeFi mechanisms towards regulated, yield-bearing conventional monetary devices.

Layer-2 networks lose stablecoin balances

The contraction additionally confirmed up throughout blockchain networks, particularly on Ethereum layer-2s.

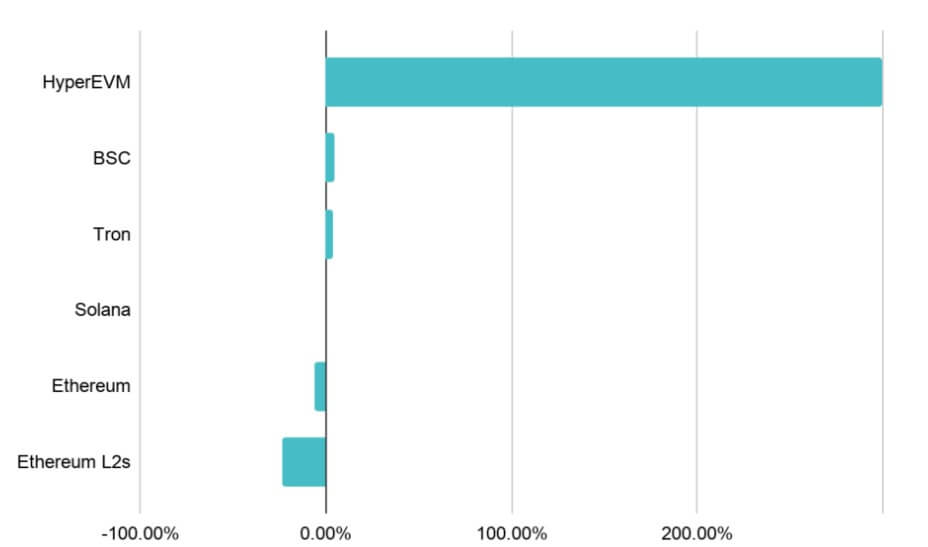

Stablecoin provide on Ethereum scaling networks fell 24%, or $4.34 billion, in Q2. That was the most important quarterly decline for the phase because the fourth quarter of 2022.

Arbitrum accounted for a lot of the fall. Its stablecoin provide dropped 45%, dropping $3.5 billion in the course of the quarter. The community had beforehand benefited from its function as a significant route into Hyperliquid.

HyperEVM’s personal stablecoin provide rose 300% to $5.6 billion, exhibiting that some liquidity shifted away from Arbitrum quite than leaving the market totally.

Ethereum’s base layer recorded a fair bigger absolute decline, dropping greater than $10 billion in stablecoin provide. CEX.IO stated that was Ethereum’s steepest quarterly drop because the first quarter of 2023.

Different networks moved in the wrong way. Tron added $3.4 billion in stablecoin provide, whereas BNB Chain gained $700 million.

The rise in these chains was largely tied to fee exercise, exhibiting that stablecoins used for transfers and settlement remained extra resilient than these tied to DeFi and buying and selling flows.

The network-level information factors to a market that’s not contracting evenly. Some crypto-native liquidity channels weakened sharply, whereas payment-heavy chains continued to develop.

That distinction might form how rapidly the market stabilizes if buying and selling exercise stays subdued.

USDC positive factors share as buying and selling falls

A clearer affirmation of systemic deceleration appeared in community exercise metrics, however USDC stood out as an exception.

CEX.io said that complete stablecoin buying and selling quantity fell 18% to $6.8 trillion. USDT quantity dropped 24%, reflecting a broader decline in crypto buying and selling exercise.

Alternatively, USDC quantity rose 34%, making it the one main stablecoin to report absolute buying and selling development in the course of the quarter. That pushed USDC’s share of complete crypto buying and selling quantity to 12.5%, a report excessive. The earlier excessive was 11%, set within the fourth quarter of 2023.

The shift partly displays modifications in centralized change markets, particularly in Europe. Tether has not secured authorization underneath the European Union’s Markets in Crypto-Belongings (MiCA) framework, and exchanges have been decreasing USDT help in regulated European venues.

That has created extra room for USDC, which has benefited from Circle’s compliance place within the area.

CEX.IO’s platform information confirmed an identical sample. USDC accounted for 60% of stablecoin-related monetary operations on the change in Q2, up from 58% within the first quarter and 27% within the first quarter of 2025.

The figures present USDC gaining floor at the same time as the general buying and selling atmosphere cooled. That provides Circle’s token a stronger place in regulated change exercise, whereas USDT’s dominance faces extra stress in markets the place compliance necessities are tightening.

Transfers present a broader slowdown

Notably, the clearest signal of weaker exercise within the stablecoin sector got here from transaction information.

Stablecoin transaction counts fell to 4.48 billion in Q2, down 530 million from the earlier quarter. CEX.IO stated that was the most important absolute quarterly decline on report. The 11% drop was additionally the steepest proportion decline because the fourth quarter of 2022.

The slowdown remained seen after eradicating bot, automated, and non-economic exercise. Adjusted transaction counts fell to 613 million, down about 11 million from Q1.

The smaller decline in adjusted exercise means that a big a part of the general drop got here from infrastructure-related and automatic flows quite than peculiar customers alone.

Adjusted transaction quantity additionally fell. Natural stablecoin switch quantity dropped 5.5% to $4.09 trillion, ending a run of 10 consecutive quarterly will increase. The reversal adopted an 18.3% achieve within the first quarter, making the Q2 decline extra notable.

Nonetheless, smaller transfers held up higher. Transfers under $250 rose 5% to $19.39 billion. That enhance means that retail-sized funds and peer-to-peer motion remained energetic at the same time as bigger transfers slowed.

The distinction between small and huge transfers is necessary for the second half of the 12 months. If smaller funds proceed to develop whereas high-value buying and selling and infrastructure flows decline, stablecoins might turn out to be much less tied to crypto market cycles over time. If bigger flows proceed to fall, nonetheless, the market might face an extended liquidity reset.

Regulation now meets a weaker market

The second-half outlook will rely partly on whether or not regulation brings new demand rapidly sufficient to offset weaker crypto-native exercise.

In Europe, MiCA’s transition interval ended July 1, forcing crypto-asset service suppliers to function underneath the bloc’s authorization regime or cease serving EU purchasers.

That would proceed to reshape stablecoin buying and selling pairs, significantly the place exchanges transfer away from USDT and towards regulated alternate options.

Within the US, the GENIUS Act is pushing stablecoin issuers towards clearer reserve, redemption and supervision requirements. The CLARITY Act might add a broader market construction framework for digital belongings, although its path stays tied to the Senate calendar and unresolved political fights.

Conventional monetary corporations are additionally shifting deeper into stablecoins. For context, SoFi and MoneyGram have introduced plans for stablecoins, whereas Japan’s three largest banks have superior work on a joint yen-pegged token.

These efforts counsel that institutional curiosity has not disappeared, at the same time as crypto-native demand weakened in Q2.

The query is whether or not new fee, banking, and real-world asset use circumstances can offset the stress from declining buying and selling exercise.

Through the 2022-2023 downturn, stablecoin provide took a couple of 12 months to return to sustained development.

Nevertheless, the present cycle might not comply with that timing as a result of the market is extra diversified than it was three years in the past.