Celsius froze withdrawals in June 2022 earlier than submitting for Chapter 11 in July 2022, and Genesis froze redemptions after FTX’s collapse and filed for chapter in January 2023, owing roughly $3.4 billion to its 50 largest collectors.

BlockFi, Celsius, Genesis, and Voyager collectively accounted for 40% of the crypto lending market and 82% of CeFi lending at their peaks, per Galaxy knowledge. The 2022 unwind uncovered two failures concurrently: dangerous loans and the entire opacity of the place threat sat inside these stability sheets.

The reply crypto landed on was to place lending on-chain, which helped tackle a number of the opacity downside.

Constructing the credit score infrastructure that institutional lenders require, similar to outlined seniority, first-loss retention, enforceable custody preparations, unbiased administration, borrower servicing, and legal-grade chapter isolation, demanded a unique method completely.

Maple and Kraken’s warehouse facility is a take a look at of whether or not DeFi can ship that infrastructure on the collateral layer, utilizing liquid BTC and ETH because the asset base.

| Credit score mannequin | What it solved | What it left uncovered | Why it issues |

|---|---|---|---|

| 2021–2022 CeFi lending | Easy accessibility to yield and borrowing | Opaque stability sheets, unclear threat location, weak buyer visibility | Celsius, Genesis, BlockFi and Voyager uncovered the failure mode |

| Automated DeFi lending | Clear collateral and liquidation guidelines | Restricted servicing, exercise, authorized restoration and borrower monitoring | Aave/Morpho-style swimming pools are clear however slender |

| RWA non-public credit score | Actual-world yield introduced onchain | Restoration nonetheless relies on offchain authorized processes | Goldfinch/Lend East confirmed visibility doesn’t equal restoration |

| Maple/Kraken warehouse facility | Outlined roles, seniority, custody, first-loss capital and onchain reporting | Nonetheless uncovered to BTC/ETH collateral volatility and execution threat | Assessments whether or not DeFi can run institutional credit score infrastructure |

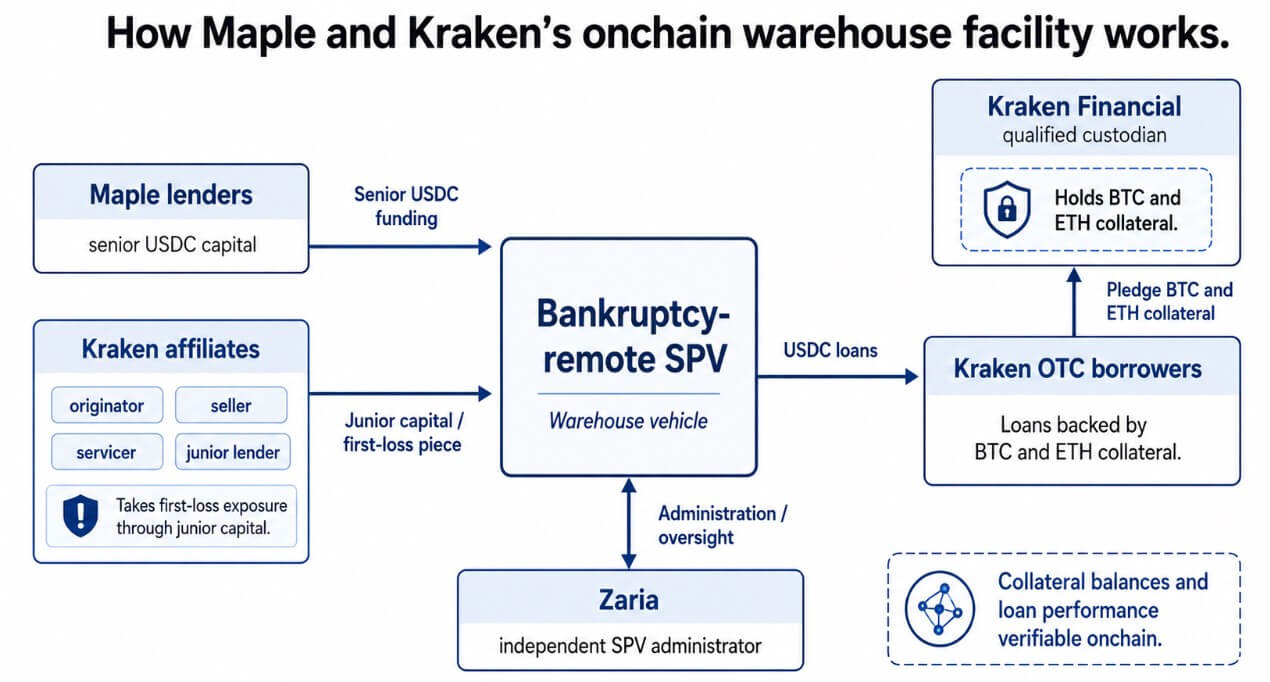

What the construction does

Kraken funds its OTC lending e book via the USDC facility, with Maple lenders offering senior capital and Kraken associates originating, promoting, and servicing the loans whereas retaining junior publicity, which means Kraken absorbs losses earlier than senior lenders take any hit.

Kraken Monetary, a Wyoming-chartered SPDI and controlled certified custodian, holds the BTC and ETH collateral, and Zaria administers the SPV independently.

Kraken structured the ability inside a bankruptcy-remote SPV to isolate it from Kraken’s entity threat and says that collateral balances and mortgage efficiency are verifiable on-chain in actual time.

Aave liquidates debtors when the well being issue falls beneath 1, and Morpho when LTV exceeds the market’s outlined threshold, each collateral-ratio and liquidation engines, clear and automatic however bounded by what automated liquidation can deal with.

Origination, servicing, monitoring, exercise, and credit score restoration require human judgment, authorized relationships, and institutional construction that automated protocols depart unaddressed.

Maple and Kraken are including these layers, together with authorized structuring that goes past what good contracts alone can implement.

Kraken’s most forward-looking announcement line is “repeatable template for added originators,” framing the ability as a credit score infrastructure template open to different originators.

If that declare holds, the construction turns into a mannequin for exchanges, custodians, and OTC desks in search of to develop their lending books by bringing in senior outdoors capital.

The issue Goldfinch recognized

In April 2024, a Goldfinch governance replace mentioned Lend East anticipated to repay roughly $4.25 million of a $10.15 million pool, a roughly 58% principal loss, with the chain logging the loss in actual time whereas Warbler Labs turned to exterior counsel and off-chain authorized processes to pursue restoration.

Maple and Kraken goal to sidestep that particular failure mode by utilizing liquid BTC and ETH as collateral, with execution on a crypto change taking seconds, recovering a defaulted trade-finance receivable in an rising market takes years.

The collateral alternative concentrates threat in market liquidity and execution velocity, a take a look at the construction can run rapidly towards observable knowledge.

The structural guess is that crypto-native collateral pairs greatest with warehouse finance, with outlined roles, outlined seniority, and outlined triggers, and a borrower underwriting layer on prime.

RWA.xyz exhibits tokenized credit score at $5.73 billion in distributed worth as of June 25, with Maple as the most important platform by worth at roughly $1.4 billion and a 24.6% market share. These figures present that actual institutional capital is already allotted to the class.

Warehouse finance as credit score infrastructure

Galaxy’s newest leverage report put complete crypto-collateralized lending at $67.42 billion on the finish of the primary quarter, down 5.1% quarter over quarter and 14.3% beneath the excessive registered within the third quarter of 2025.

DeFi lending apps nonetheless held $28.22 billion in excellent loans, down 13.82% within the first quarter, whereas CeFi lenders had $25.43 billion in open borrows, down 7.23% on the quarter.

Combining DeFi apps and CeFi lending venues, Galaxy tracked $53.65 billion of excellent crypto-collateralized borrows at quarter-end, with DeFi’s share narrowing to 52.6% from 54.3% within the final quarter of 2025.

Galaxy mentioned DeFi open borrows had already fallen to $23.29 billion as of Could 1, down 50.58% from their Sept. 19, 2025, all-time excessive of $47.13 billion, following exploits and capital flight that hit on-chain lending.

That makes Maple and Kraken’s services extra related to institutional credit score returns, nevertheless it requires solutions on collateral custody, first-loss safety, servicing, liquidation triggers, authorized isolation, and what lenders can confirm earlier than stress hits.

Warehouse strains in conventional credit score are the bridge between mortgage origination and scaled capital markets.

A World Financial institution/IFC doc describes them as revolving services used to construct mortgage portfolios for future securitization, with property pledged to an SPV and core threat mitigants together with servicing, belief agreements, custodians, overcollateralization, and authorized enforceability.

SIFMA reported $232.3 billion in US ABS issuance via Could 2026, up 12.6% yr over yr, the size standardized structured credit score reaches when its infrastructure is trusted.

| Market / metric | Information level | Article implication |

|---|---|---|

| Whole crypto-collateralized lending | $67.42B in Q1 2026 | Crypto credit score is massive sufficient to wish institutional infrastructure |

| DeFi lending app loans | $28.22B in Q1 2026 | Onchain lending stays important, however risky |

| CeFi open borrows | $25.43B in Q1 2026 | Centralized lending is rebuilding, however wants belief constructions |

| DeFi open borrows by Could 1 | $23.29B | Capital flight after exploits exhibits clear swimming pools usually are not sufficient |

| DeFi decline from Sept. 2025 ATH | -50.58% | The sector nonetheless lacks sturdy institutional confidence |

| Tokenized credit score distributed worth | $5.73B | Institutional capital is already getting into structured onchain credit score |

| Maple tokenized-credit worth | ~$1.4B | Maple is already a serious participant within the class |

| Maple tokenized-credit share | 24.6% | Exhibits why this facility issues past one deal |

| US ABS issuance via Could 2026 | $232.3B | Conventional structured credit score exhibits the size attainable with trusted infrastructure |

If Maple and Kraken carry out via regular market volatility, the template turns into out there to different originators.

Standardized LTV bands, collateral eligibility guidelines, liquidation triggers, custody preparations, servicing obligations, and on-chain reporting templates might comply with, creating the constant credit score documentation that institutional capital must allocate at scale.

The place the construction will get examined

The chance has moved from opaque stability sheets to execution, together with correct pricing throughout collateral declines, well timed margin calls, liquid markets for liquidation, responsive custody, and servicer efficiency when it counts most.

If BTC or ETH gaps decrease quicker than margin calls execute, the ability relies on public sale depth and execution velocity, and a number of lenders liquidating comparable collateral concurrently can amplify promoting.

That’s the similar forced-liquidation dynamic that crypto markets have skilled repeatedly throughout sharp drawdowns.

Authorized construction reduces opacity, whereas collateral worth volatility stays out there no matter how the credit score stack is structured.

The mannequin proves itself throughout a pointy BTC or ETH worth drop, a liquidity hole in collateral markets, a borrower default, a servicer impairment, or a authorized take a look at of the SPV’s chapter remoteness.

Coinbase affords USDC borrowing towards BTC collateral via Morpho, with liquidation triggered at 86% of the BTC collateral’s market worth.

Maple and Kraken construct the institutional layers above that mannequin, and every layer provides an operational dependency that requires efficiency throughout a fast collateral decline.

What comes subsequent

Warehouse services in conventional credit score usually precede securitization, and originators use them to build up mortgage swimming pools, construct efficiency historical past, and standardize documentation earlier than accessing broader capital markets.

If Maple and Kraken’s loans carry out via a full market cycle, the following step could possibly be bigger swimming pools of crypto-backed credit score financed by institutional traders who want that efficiency document earlier than they’ll allocate.

If this template spreads, crypto credit score might develop constant underwriting standards: which collateral qualifies, at what LTV, with what liquidation triggers, held by what kind of custodian, serviced underneath what obligations, reported in what on-chain format.

That consistency enabled the normal ABS market to succeed in $232 billion in annual issuance, permitting consumers to underwrite a construction as soon as and apply that framework throughout the whole mortgage pool.

Crypto-backed credit score wants that very same infrastructure layer earlier than institutional capital allocates to it at scale, with Maple and Kraken operating the primary take a look at of whether or not DeFi can construct it.