Goldfinch, a crypto lending platform that linked investor capital with real-world debtors, is now displaying what occurs after the lending growth ends: the laborious threat sits in gathering from debtors as soon as progress has slowed.

The June 12 GIP-87 proposal would cease new protocol improvement, wind down Goldfinch Prime, hold legacy app entry accessible, create a U.S. belief construction, and pay Warbler Labs $150,000 USDC for wind-down providers.

The proposal stays below governance consideration, with group dialogue persevering with by way of June 20. No formal approval or rejection has been publicly recorded on the time of writing. The broader market implication stays the identical: tokenized non-public credit score can shift from yield era to borrower exercises whereas underlying loans stay lively.

In Goldfinch’s case, the subsequent section facilities on recoveries from legacy debtors, borrower-pool efficiency points, servicing prices, and the time it takes to show mortgage claims again into money.

That shift turns DeFi non-public credit score from an access-and-yield pitch right into a exercise take a look at. For buyers, protocols, and RWA lenders, the important thing query is whether or not underwriting, default administration, and borrower restoration can maintain up as soon as the mortgage e-book stops rising.

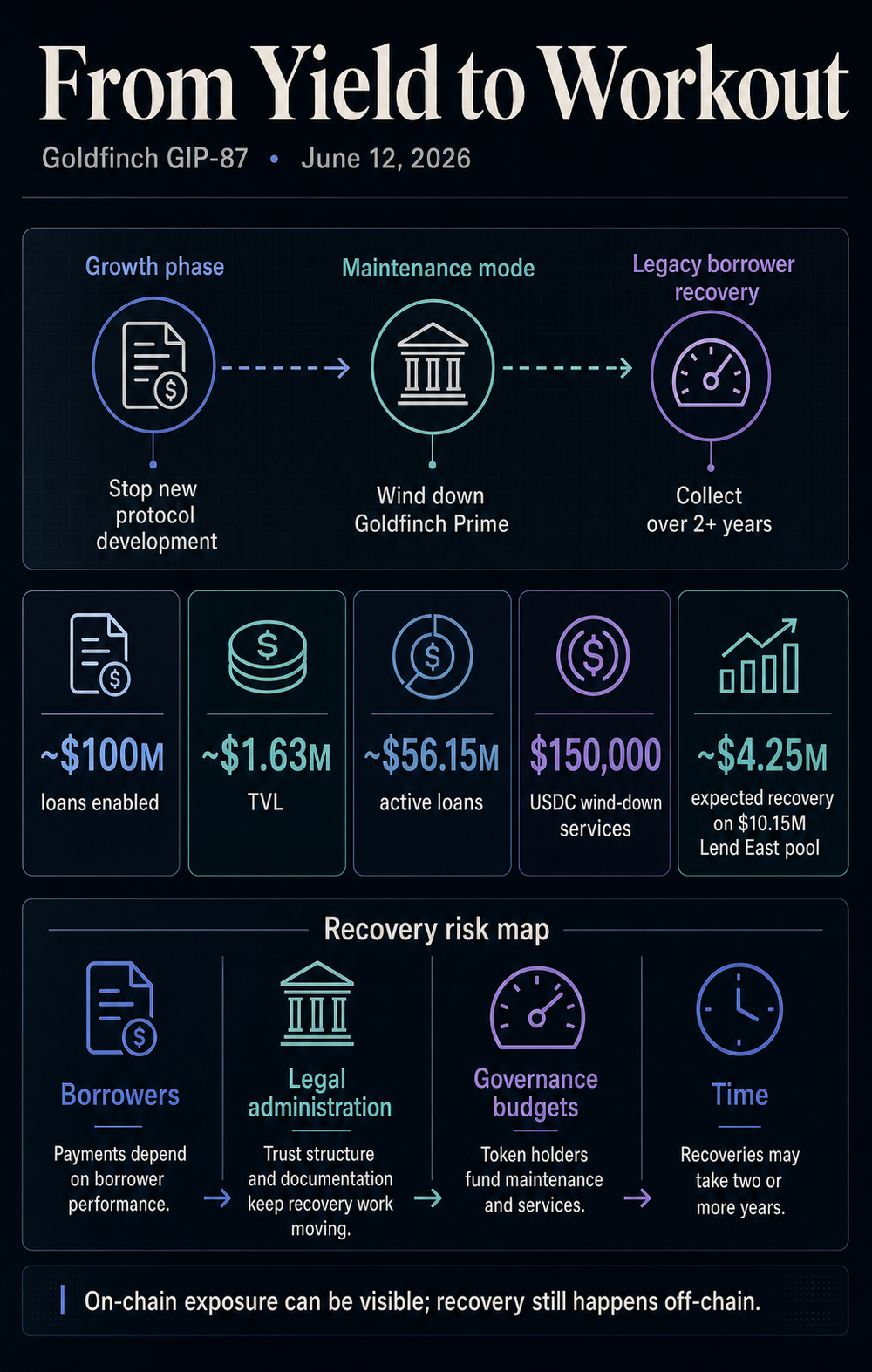

From mortgage progress to restoration work

The proposal says Goldfinch’s unique protocol enabled roughly $100 million in loans, whereas a number of borrower swimming pools had critical efficiency points. It could put the protocol into upkeep mode relatively than fund new improvement, with operations centered on gathering funds from legacy debtors.

That may be a completely different enterprise from origination. New lending rewards pace, distribution, and capital formation. Restoration rewards documentation, endurance, authorized leverage, borrower follow-up, and controls round who pays for the work.

Goldfinch is shifting towards a public restoration car for a private-credit e-book.

Current public knowledge exhibits Goldfinch with roughly $1.65 million in TVL, whereas lively loans stay materially bigger. The precise figures fluctuate over time, however the important thing commentary stays that the protocol’s lively credit score publicity considerably exceeds its present on-chain liquidity footprint.

Energetic loans are excluded from TVL by default, so the 2 figures describe completely different features of the identical downside. TVL can present a small, reside DeFi footprint, whereas lively loans present a bigger e-book that also must be monitored, serviced, or recovered.

| Metric or time period | Progress-era studying | Exercise-era studying |

|---|---|---|

| About $100 million in loans enabled | Proof that Goldfinch reached significant private-credit scale | A bigger restoration floor if borrower efficiency deteriorates |

| About $1.63 million in TVL on June 23 | A small present DeFi liquidity footprint | Restricted on-chain capital relative to the work nonetheless connected to lively loans |

| About $56.15 million in lively loans on June 23 | Proof that the mortgage e-book has residual publicity | A reminder that publicity can outlast progress capital and token momentum |

| $150,000 USDC wind-down providers fee | A governance finances line | A visual price of servicing and restoration after origination |

| About $4.25 million anticipated restoration on a $10.15 million Lend East pool in April 2024 | A borrower-pool replace | A concrete instance of how private-credit losses can turn into sluggish restoration math |

Public lending dashboards proceed to point out a big hole between Goldfinch’s TVL and its active-loan e-book. These metrics seize completely different elements of the system.

TVL displays capital at the moment parked within the protocol, whereas lively loans characterize credit score publicity that also requires servicing, monitoring, restructuring, or restoration. The persistence of that hole highlights how restoration obligations can outlast a protocol’s progress section.

That hole is the place tokenized non-public credit score begins to look much less like liquid DeFi and extra like a public wrapper round private-credit servicing.

The chance disclosures level in the identical path. Senior Pool documentation warned that individuals may lose cash if debtors didn’t repay and will face liquidity limits if there was inadequate USDC within the pool.

The wind-down turns these basic product dangers into governance logistics: how a lot ought to nonetheless be funded, who performs the work, how legacy customers retain entry to the app, and what authorized construction handles borrower restoration.

The Lend East borrower replace offers these questions a concrete form. In April 2024, a Goldfinch discussion board replace stated the pool was anticipated to repay about $4.25 million towards a $10.15 million Goldfinch pool at the moment, implying a big anticipated principal shortfall.

That was an anticipated restoration determine on the time of the replace, earlier than any closing realized end result. It nonetheless exhibits how private-credit restoration turns into a matter of timelines, shortfalls, negotiations, and authorized paths relatively than dashboard balances.

That’s the place DeFi non-public credit score collides with conventional non-public credit score. Blockchains could make positions, tokens, and protocol exercise simpler to watch. Precise compensation nonetheless will depend on borrower habits, servicing, documentation, and authorized paths when a mortgage goes improper.

Governance turns into a part of the credit score stack

The $150,000 USDC fee to Warbler Labs is small in contrast with Goldfinch’s historic mortgage origination, nevertheless it makes the restoration operate express. In a progress section, governance budgets typically fund improvement, incentives, integrations, or growth.

Within the wind-down section, the finances covers upkeep, app continuity, authorized administration, and the labor required to gather on current obligations.

That adjustments what token holders are voting on. The choice considerations how a credit score e-book ought to be serviced after progress capital has exited.

The proposal’s U.S. belief construction and continued legacy app entry level to a section through which the system should protect enough infrastructure for funds and recoveries whereas scaling again work unrelated to the outdated mortgage e-book.

For RWA lenders, the lesson is an uncomfortable one. A tokenized private-credit platform has to show greater than origination demand. It has to show borrower choice, reporting self-discipline, restoration administration, servicing incentives, and governance controls.

If these items are weak, the chain could make the harm seen with out making the restoration simple.

Current CryptoSlate protection has proven the expansion aspect of the identical market. One private-credit lender is attempting to make use of AI to compress months of paperwork into one-day on-chain loans, whereas broader RWA protection has centered on how tokenized property match into DeFi’s composability limits.

Goldfinch’s proposal provides the half that growth narratives go away for later. Quicker origination should be paired with a reputable course of for dealing with sluggish compensation, missed funds, and disputes.

That distinction additionally explains why Goldfinch ought to be learn fastidiously. The proposal is a reside instance of how the credit score stack adjustments after the origination section, with demand elsewhere in RWA lending nonetheless higher than this single case.

The property could also be represented on-chain, however the restoration course of nonetheless runs by way of borrower habits, authorized administration, documentation, and governance-funded work.

What RWA lenders need to show subsequent

Goldfinch is one particular case in tokenized non-public credit score. DefiLlama knowledge nonetheless exhibits broader RWA lending TVL and DeFi active-loan exercise effectively past Goldfinch’s present footprint, leaving the sector’s demand image bigger than one protocol’s maintenance-mode proposal.

The extra helpful takeaway is restricted. Tokenized non-public credit score has two markets without delay. One seems when capital is deployed, yields are mentioned, and token costs commerce.

The opposite seems later, when debtors miss targets, restoration takes years, and governance has to resolve whether or not to maintain paying for the equipment that collects the remaining money.

That makes Goldfinch as a lot a restoration commerce as a DeFi protocol. Its future worth relies upon much less on new protocol options and extra on borrower funds, restoration administration, and whether or not the proposed construction can protect sufficient operational capability to gather what stays.

The following alerts are sensible. A proper governance end result would make clear whether or not GIP-87 turns into the working path. Updates from the proposed belief or directors would present whether or not restoration work has a transparent cadence.

Borrower fee updates would present whether or not the active-loan footprint converts into money or stays caught in negotiation. Different RWA lenders can even have to point out how they disclose borrower efficiency, fund servicing work, and shield customers when private-credit loans cease behaving like yield merchandise.

Goldfinch’s reply to the recovery-risk query is blunt. On-chain non-public credit score could make publicity simpler to trace, however restoration nonetheless will depend on off-chain debtors, authorized administration, governance budgets, and time.

The yield pitch brings capital in. The exercise checks whether or not the credit score was sound.