Calais Digital Belongings has turned UBS uMINT collateral right into a dwell buying and selling workflow on Bybit, giving tokenized money-market funds a concrete margin use case relatively than one other issuance milestone.

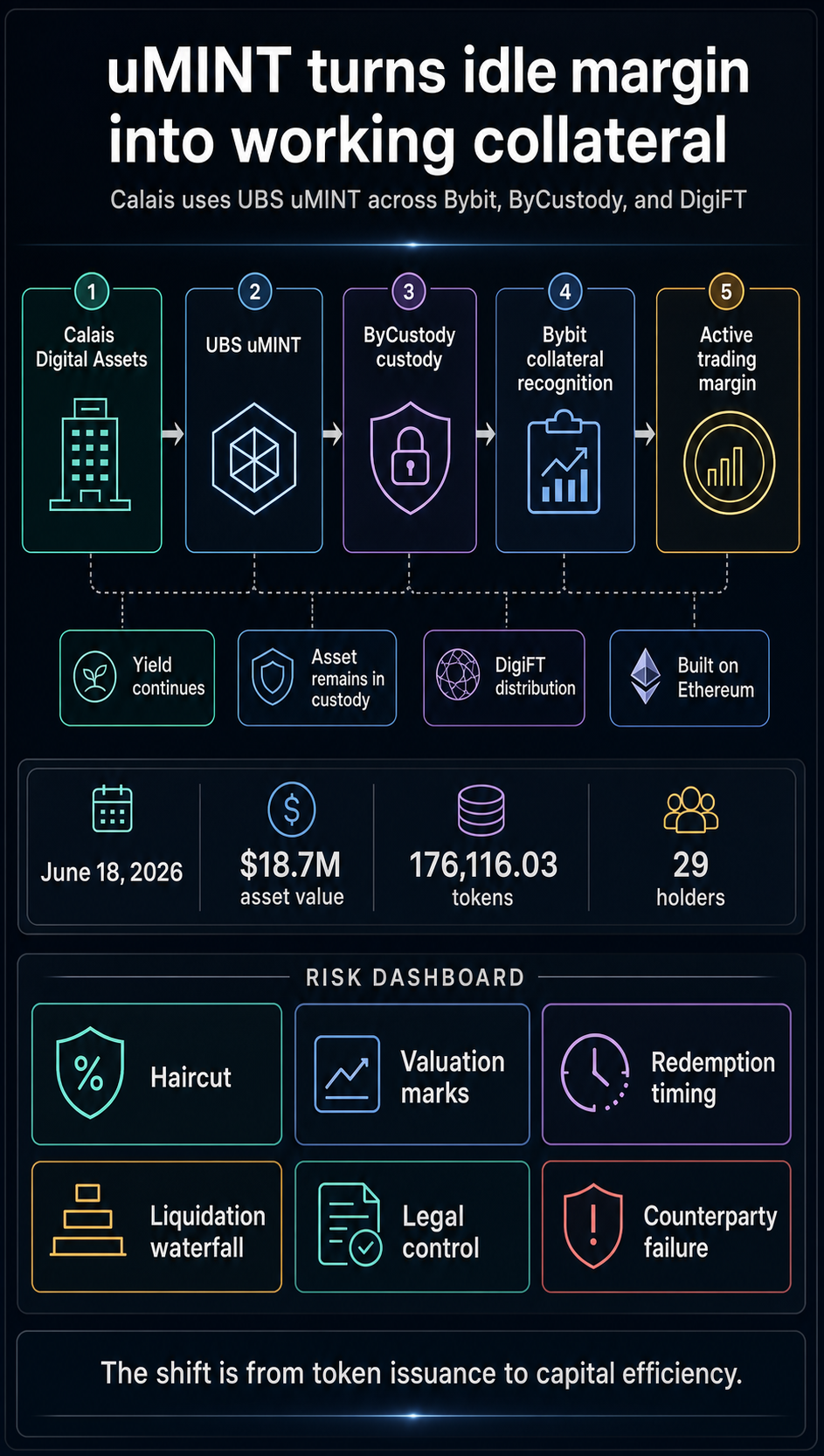

The setup runs throughout Bybit, ByCustody, and DigiFT, with the uMINT place remaining in custody whereas it’s acknowledged as change collateral.

The June 18 deployment is necessary as a result of collateral that may sometimes sit as idle money or money equal can nonetheless earn money-market yield whereas supporting buying and selling exercise.

For tokenized real-world property, that shifts the dialogue from issuance quantity to market plumbing. The query is whether or not these devices can develop into helpful sufficient to exchange idle margin inside actual buying and selling operations.

How UBS uMINT collateral works on Bybit

Calais, a Singapore-headquartered quantitative funding fund, is utilizing UBS uMINT as off-exchange settlement collateral in lively buying and selling operations.

The off-exchange settlement collateral transaction runs by means of a three-party setup: DigiFT supplies regulated entry and distribution for uMINT, ByCustody holds the asset, and Bybit accepts the custodied place as collateral on its change infrastructure.

That modifications the economics of margin. Conventional collateral preparations typically require a dealer to park money, stablecoins, or different eligible property in a kind that protects the buying and selling venue whereas limiting what the fund can earn on these property.

In DigiFT’s description, Calais can preserve publicity to a money-market product whereas utilizing that very same place to help buying and selling.

The excellence is operational relatively than beauty. A tokenized fund that exists on-chain is helpful as a settlement asset provided that venues, custodians, distributors, and authorized buildings agree on how it may be held, valued, and managed.

A tokenized fund that may additionally fulfill change collateral necessities begins to behave extra like a working balance-sheet software.

| Query | Conventional idle margin | uMINT as OES collateral |

|---|---|---|

| The place the asset sits | Normally posted or reserved for the buying and selling venue | DigiFT says Calais’s uMINT stays in ByCustody |

| Yield remedy | Money or money equivalents might cease incomes for the dealer | DigiFT says Calais maintains yield whereas buying and selling |

| Change utility | Collateral backs buying and selling instantly | Bybit acknowledges the custodied uMINT as buying and selling collateral |

| Remaining danger | Venue, custody, and margin phrases stay central | Haircuts, redemptions, liquidation rights, and authorized remedy stay key questions |

The comparability is the core capital-efficiency declare. The tokenized place could be acknowledged by an change whereas remaining inside a custody association designed for institutional use.

That’s the place the deployment reaches past one other RWA announcement and turns into a dwell check of RWA collateral inside change margin infrastructure.

It additionally exhibits why token issuance alone is simply the primary layer. The commerce requires a distributor, custodian, and change to agree on custody, recognition, and operational management earlier than the fund place can perform as collateral in observe.

The rails and the size

The Calais deployment follows earlier plumbing. In October 2025, Bybit, DigiFT, and UBS uMINT launched institutional entry to collateral for the tokenized fund.

That earlier announcement established the fundamental institutional pitch: shares of UBS’s tokenized money-market fund, distributed by means of DigiFT, could possibly be used as collateral on Bybit.

In November 2024, uMINT launched as UBS’s first tokenized funding fund. UBS described the UBS USD Cash Market Funding Fund Token as a money-market funding constructed on Ethereum distributed ledger expertise.

The product is designed to present tokenholders entry to institutional-grade money administration backed by high-quality money-market devices.

These particulars are central as a result of uMINT is being positioned as a conservative cash-management publicity relatively than a unstable crypto margin publicity.

The Calais use case is about capital effectivity: a fund needs collateral that continues to be appropriate for buying and selling operations whereas nonetheless staying productive on the steadiness sheet.

CryptoSlate has already lined the unique uMINT launch and the broader development towards tokenized revenue merchandise changing into greater than passive holdings.

The brand new step is the particular exchange-margin workflow. The dwell peg is that an institutional buying and selling shopper is now utilizing the fund token as acknowledged collateral inside a Bybit, ByCustody, and DigiFT stack.

The present scale of uMINT nonetheless argues for restraint. The uMINT asset web page identifies UBS USD Cash Market Funding Fund Token as a U.S. Treasury asset on UBS Tokenize, with UBS Asset Administration (Singapore) Ltd. as supervisor and Ethereum because the native ERC-20 community.

On June 21, the overall asset worth was round $18.7 million, 176,116 tokens, and 29 holders.

These numbers make the product dwell however early. They present an actual tokenized money-market product with seen on-chain scale wired into an institutional collateral workflow, whereas broad adoption and standardization throughout crypto venues stay to be seen.

The enterprise challenge sits in market construction, relatively than worth motion. CryptoSlate’s mixture market pages can present broad context for the dimensions of the crypto market, however the operational driver is whether or not tokenized funds could be made helpful inside repeatable buying and selling processes.

These processes embrace custody, collateral recognition, settlement, valuation, liquidity, and danger management.

If the mannequin spreads, the impression can be sensible. Funds would have a stronger path to carry yield-bearing cash-management merchandise whereas posting buying and selling collateral.

Exchanges may compete on the standard of the property they acknowledge as margin, in addition to on liquidity and charges. Custodians and distributors would develop into a part of the buying and selling stack, relatively than solely post-trade infrastructure.

The onerous questions are nonetheless within the margin phrases

The identical options that make the Calais setup fascinating additionally go away a number of unresolved questions. Public particulars launched for the deployment omit the haircut Bybit applies to tokenized money-market fund collateral, the valuation supply, the frequency of collateral marks, and the liquidation waterfall if losses outpace redemption or switch processes.

Liquidity timing is one other stress level. Cash-market funds are designed for cash-management stability, however they’ll behave in a different way from stablecoins throughout a quick exchange-stress occasion.

RWA.xyz’s product web page lists subscription and redemption fields, whereas buying and selling companies nonetheless want to grasp what occurs when margin calls, change danger techniques, and fund liquidity home windows collide.

Authorized remedy is equally necessary. Segregated custody can cut back one class of venue danger, whereas chapter, management, and enforceability questions stay throughout a multi-party stack.

A fund utilizing the construction nonetheless wants confidence about who can transfer collateral, below what circumstances, and what occurs if the change, custodian, distributor, or one other middleman fails.

Eligibility will even form adoption. DigiFT’s supplies state that the product and companies can be found solely by means of approved and controlled intermediaries to eligible traders.

That factors to an expert and institutional lane earlier than any use of retail margin. If the mannequin expands, it’ll possible accomplish that first by means of certified purchasers, authorised custodians, and venue-specific collateral guidelines.

The Calais deployment is finest learn as a first-client implementation with significant implications. It exhibits a concrete path from token issuance to buying and selling utility: a UBS money-market token distributed by means of DigiFT can sit in ByCustody and nonetheless rely as collateral on Bybit.

The deployment reaches a ache level establishments perceive. Idle margin is dear. Yield-bearing collateral is enticing.

However the mannequin solely turns into sturdy if the operational controls can survive the moments when collateral is most necessary: market volatility, pressured deleveraging, liquidity stress, and counterparty failure.

The subsequent sign is whether or not extra funds, extra eligible property, and extra venues undertake related phrases with clear haircut, redemption, custody, and liquidation guidelines.

Till then, the Calais commerce marks a dwell proof level for tokenized money-market collateral, and a reminder that the true check for RWAs is whether or not they can do helpful work as soon as they get on-chain.