The Clearing Home, the bank-owned operator of core U.S. fee infrastructure, is making ready a system that lets banks settle deposits on-chain.

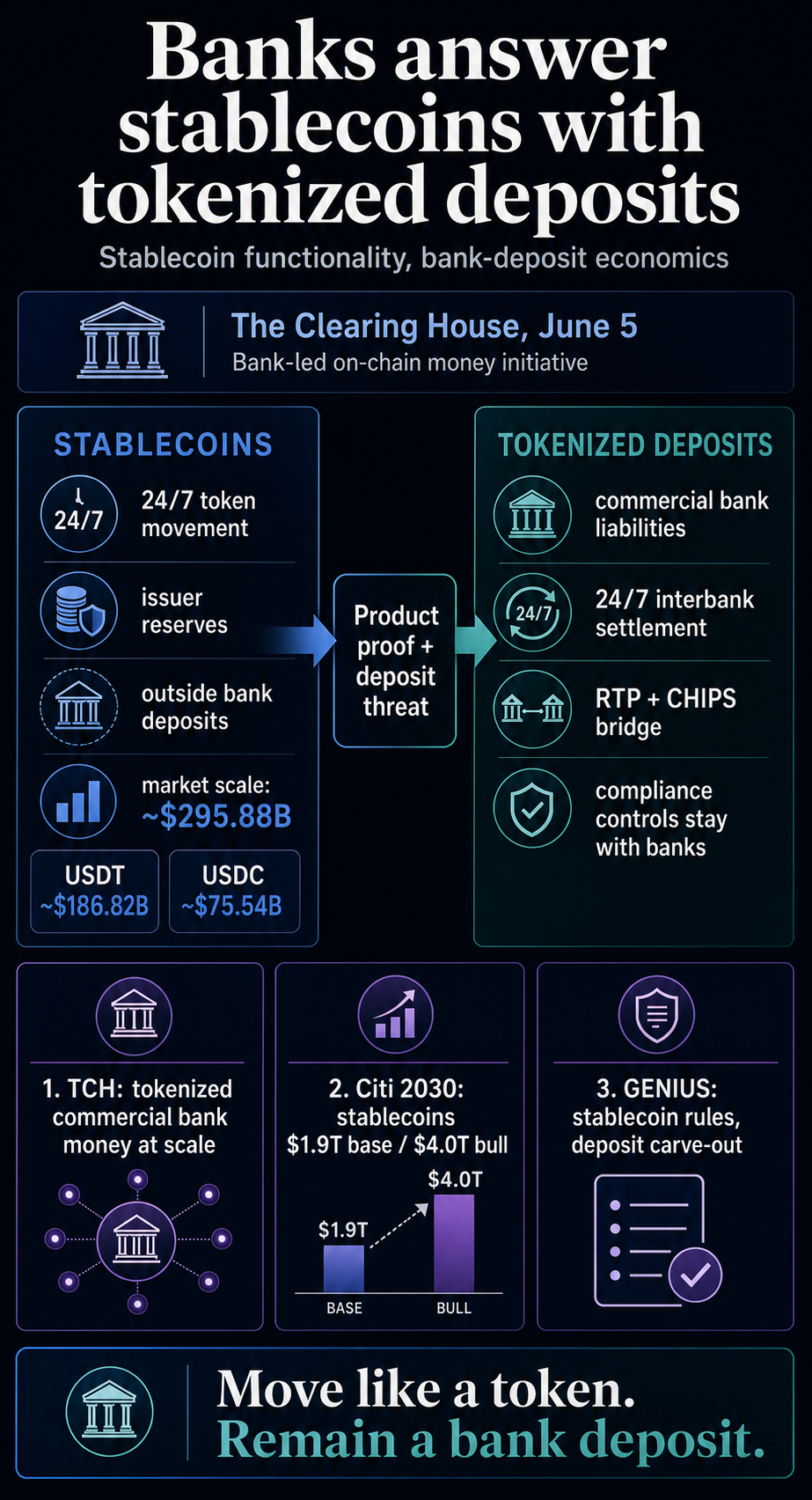

Its June 5 announcement places the most important U.S. banks behind a shared response to the stablecoin problem: greenback funds can now transfer across the clock, throughout blockchain rails, with programmable settlement.

Banks need these options whereas retaining the client balances, compliance controls, and deposit economics that sit contained in the regulated banking system.

The initiative would allow clearing and settlement of tokenized business financial institution cash at scale. TCH mentioned it could help 24/7 on-chain clearing and settlement of tokenized deposits between banks whereas linking blockchain-based exercise with established fiat rails resembling RTP and CHIPS, in keeping with The Clearing Home announcement.

That construction provides banks a distinct instrument from a financial institution stablecoin. Stablecoins transfer greenback claims outdoors the deposit system. Tokenized deposits attempt to transfer financial institution deposits with a number of the identical digital options whereas retaining the cash as business financial institution liabilities.

The technique is defensive and opportunistic on the identical time. Banks are embracing crypto rails as a result of stablecoins proved demand for tokenized {dollars}, and since stablecoins threaten the deposit base that makes banking economics work.

Financial institution cash strikes onto crypto rails

The Clearing Home enters this combat as bank-owned funds infrastructure. Its owner-bank web page says it’s owned by the world’s largest business banks, and the brand new announcement says it’s owned by 25 of the nation’s largest monetary establishments.

That possession is central as a result of the proposed community retains financial institution cash inside financial institution rails whereas giving deposits a digital-asset-style settlement layer.

The announcement describes tokenized deposits that may settle between banks, carry richer transaction information, and help automated workflows. The connectivity layer to RTP and CHIPS is equally essential. It factors to a managed bridge between on-chain exercise and financial institution fee programs.

The Clearing Home already has a tokenization precedent inside bank-controlled fee flows. Its DDA Token Service replaces buyer account numbers with tokens and manages translation again to account numbers in a safe atmosphere, together with for compliance functions.

That service is a separate Open Banking payment-token product. It exhibits the working precept banks try to hold ahead: expose much less delicate financial institution data, protect compliance visibility, and preserve the financial institution because the trusted management level.

Citi’s analysis exhibits why banks care. In its Stablecoins 2030 report, Citi raised its 2030 stablecoin issuance forecast to $1.9 trillion in its base case and $4.0 trillion in its bull case.

The identical report argues that stablecoins will coexist with financial institution tokens resembling tokenized deposits and deposit tokens, and that bank-token transaction volumes might exceed stablecoin volumes by 2030.

Citi’s separate Tokenization 2030 analysis factors to the institutional purpose. Present stablecoins can create pre-funding and fragmentation points for institutional settlement.

Tokenized deposits issued by regulated banks are one of many options market contributors are exploring for on-chain liquidity.

| Query | Tokenized deposits | Cost stablecoins |

|---|---|---|

| Who stands behind the cash? | A regulated financial institution deposit legal responsibility. | A permitted or overseas stablecoin issuer backed by reserves. |

| What characteristic is banks’ reply to stablecoins? | 24/7 settlement, programmability, interoperability, and richer information inside financial institution rails. | On-chain transferability, world availability, and token-based settlement. |

| How does yield match? | Deposit economics stay with banks and their account relationships. | GENIUS bars issuer-paid curiosity or yield solely for holding, utilizing, or retaining the fee stablecoin. |

| What’s the strategic incentive? | Maintain buyer cash and compliance contained in the financial institution system. | Develop digital-dollar utilization by non-deposit tokens and reserve-backed fee belongings. |

The authorized cut up banks try to protect

The coverage backdrop helps clarify why banks have chosen tokenized deposits as a substitute of issuing stablecoins and shifting on.

The GENIUS Act creates a framework for fee stablecoins, requires permitted issuers to keep up no less than one-to-one reserves, and prohibits issuer-paid curiosity or yield solely for holding, utilizing, or retaining a fee stablecoin.

The textual content additionally excludes deposits recorded utilizing distributed ledger know-how from the fee stablecoin definition.

That exclusion is central to the banks’ opening. A deposit could be recorded in a brand new method with out turning into a fee stablecoin. The authorized wrapper is decisive as a result of it decides whether or not the cash is handled as a financial institution deposit or as a tokenized declare on a stablecoin issuer’s reserves.

The FDIC has drawn a associated distinction. Its April 2026 proposed-rule abstract says deposits held as reserves backing a fee stablecoin wouldn’t be pass-through insured to stablecoin holders.

It additionally says deposit insurance coverage therapy for deposits doesn’t rely upon whether or not an insured depository establishment information these deposit liabilities utilizing distributed ledger know-how.

The rule remains to be proposed slightly than ultimate. Nonetheless, the path is evident sufficient for the present combat. Tokenized deposits let banks argue that clients can get blockchain-style settlement with out stepping outdoors deposit regulation.

Stablecoins give customers a greenback token, however the holder’s declare and insurance coverage profile are totally different from an extraordinary financial institution deposit.

The OCC can also be implementing GENIUS Act guidelines for permitted fee stablecoin issuers, overseas issuers, and associated custody actions underneath its supervision, in keeping with its February discover of proposed rulemaking.

Which means the banks’ tokenized-deposit push is arriving because the regulatory perimeter round stablecoins is being constructed.

That distinction places the TCH community within the tokenized-deposit class slightly than the stablecoin launch class. The product copies the settlement expertise that made stablecoins helpful, however the authorized declare, balance-sheet therapy, and compliance perimeter are supposed to stay inside banking.

The query is whether or not that managed model can match the pace and attain customers now count on from greenback tokens.

The combat is admittedly about deposit economics

The cleanest approach to perceive the TCH initiative is as banks responding to a market sign from stablecoins.

Stablecoin scale already makes the difficulty bank-relevant. On June 8, CryptoSlate market information confirmed roughly $296 billion in stablecoin sector market cap, with USDT at about $187 billion and USDC at about $76 billion.

The broader crypto market stood close to $2.2 trillion. These numbers transfer, however the path is clear: stablecoins are too giant to deal with as a facet product of buying and selling venues.

That development has already develop into a coverage combat. The identical pressure runs by bank-run warnings and tokenized-deposit defenses, financial institution strain over stablecoin rewards, and the query of who captures digital-dollar economics.

The CLARITY Act provides one other layer as a result of it moved digital-asset market-structure guidelines by the Home whereas the combat over fee rails, wallets, reserves, and yield continued in parallel.

Banking teams have been specific about their worry. The American Bankers Affiliation and 52 state bankers associations warned Congress that yield-like stablecoin incentives threat disintermediating deposit taking and lending, in keeping with the ABA’s December assertion.

The priority is direct: if clients can maintain greenback tokens that transfer quicker and supply rewards, some balances might depart financial institution accounts.

However the dimension of that threat is contested. The Council of Financial Advisers modeled the baseline lending impression of eliminating stablecoin yield at $2.1 billion, whereas a stacked worst-case situation reached $531 billion in further combination lending, in keeping with its April evaluation.

These are mannequin outputs, not measured deposit flight.

The Federal Reserve’s December observe can also be extra conditional than the bank-lobby framing. It says stablecoin results on financial institution deposits rely upon the place demand comes from, how issuers make investments reserves, and whether or not issuers achieve entry to central-bank accounts.

Stablecoins can cut back deposits, recycle deposits into totally different types, or change the construction of financial institution funding even when the whole quantity of deposits doesn’t fall, in keeping with the Fed evaluation.

That’s the reason the TCH transfer is defensive and offensive on the identical time: it protects the deposit relationship whereas attempting to soak up the a part of the stablecoin product that clients and establishments have validated.

Quicker settlement, programmable cash motion, and higher connectivity to digital asset markets have develop into a part of the financial institution product race.

The unresolved query is whether or not a bank-led community can match the open-network benefits that made stablecoins helpful within the first place. The TCH announcement leaves launch timing, ledger design, working guidelines, and public-chain interoperability unresolved.

For now, the file helps a sharper conclusion than both facet’s speaking factors. Stablecoins compelled banks to maneuver. Tokenized deposits are the financial institution reply: transfer the cash like a token, however preserve the cash contained in the financial institution.