The worldwide stablecoin market has climbed to a document $322 billion valuation, cementing the rise of digital {dollars} as one of many cryptocurrency sector’s most viable industrial merchandise.

The milestone displays an accelerating demand for real-time settlement, borderless cross-border transfers, and dependable greenback entry on blockchain rails.

Nevertheless, this enlargement can be intensifying anxieties inside the conventional banking sector, the place these privately issued tokens are more and more seen as a direct risk to core deposits, cost relationships, and the legacy plumbing of worldwide commerce.

In consequence, the friction is driving a basic restructuring of digital finance. As stablecoin issuers increase below newly established federal frameworks, a parallel defensive-offensive is unfolding: world banks are quietly deploying tokenized deposit programs that already route trillions of {dollars} yearly by means of blockchain-based infrastructure.

Stablecoin market strikes deeper into finance

Through the years, stablecoins have developed from a distinct segment crypto-trading refuge right into a settlement layer that threatens to disintermediate conventional banks.

Whereas dollar-pegged tokens initially gained traction as a volatility hedge for digital asset merchants, they’re now gaining a foothold in world remittances, service provider settlements, and cross-border company flows.

Regardless of this industrial enlargement, the market stays closely top-heavy. Tether (USDT) and Circle (USDC) preserve a strong duopoly, controlling greater than 80% of the circulating provide, with USDT alone accounting for almost 59%.

In the meantime, the same chokepoint exists on the community degree, the place Ethereum and Tron course of the overwhelming majority of excellent token balances.

But that structural focus isn’t deterring main conventional monetary gamers from constructing on various, high-throughput rails to seize market share.

For context, Western Union just lately launched USDPT, a US dollar-denominated cost stablecoin issued by Anchorage Digital Financial institution on the Solana community. Absolutely backed by financial institution deposits and short-dated Treasury payments, the token represents a deliberate push to route world cash transfers by means of digital-asset infrastructure moderately than legacy correspondent banking programs.

This pivot locations Western Union alongside a rising cohort of funds corporations, comparable to Payoneer, that deal with stablecoins as important industrial plumbing moderately than speculative devices.

For remittance companies and fintechs, the attraction is simple: blockchain rails provide round the clock settlement, bypass sluggish legacy intermediaries, and supply fast greenback liquidity to markets combating unreliable native currencies.

This utility has remodeled stablecoins into one of the crucial concrete industrial successes within the digital asset sector.

Whereas the present market dimension stays a fraction of worldwide industrial banking, aggressive forecasts venture that stablecoin adoption might scale right into a multitrillion-dollar sector by the tip of the last decade if fintechs absolutely combine digital {dollars} into on a regular basis monetary flows.

Even at their present scale, a whole bunch of billions of {dollars} in tokenized balances are already massive sufficient to affect US Treasury demand, dictate change liquidity, and drive a defensive rethink throughout Wall Road.

As stablecoins transfer deeper into mainstream finance, their affect is not contained inside the cryptocurrency ecosystem; they’re now the middle of a high-stakes coverage combat over who will management the way forward for world digital cash.

Regulation turns stablecoin progress right into a financial institution risk

This fast progress has revived a historic critique inside financial coverage circles: privately issued cash expands aggressively throughout market upturns however dangers triggering systemic crises if collective confidence fractures.

A current Wall Road Journal evaluation framed the stablecoin increase by means of this exact historic lens, warning that these tokens might replicate the vulnerabilities of 1800s-era “personal cash,” the place unregulated issuers chased yield on the expense of depositor security.

The underlying concern is that non-public issuers are inherently incentivized to maximise circulating provide and optimize reserve returns, probably creating liquidity mismatches during times of extreme market contraction.

The digital asset sector is pushing again strongly in opposition to this characterization. Faryar Shirzad, Chief Coverage Officer at Coinbase, factors out that non-public cash already underpins the trendy US monetary system, noting that industrial financial institution deposits and cash market fund shares comprise roughly 90% of the M2 cash provide.

From this angle, the related regulatory query isn’t whether or not an asset is publicly or privately issued, however whether or not its structural guardrails precisely match its distinctive threat profile.

This argument has gained vital authorized footing below the federal GENIUS Act framework. The laws introduces a purpose-built structure for cost stablecoins, whereas mandating strict reserve segregation, month-to-month unbiased attestations, and direct federal oversight.

The laws additionally requires issuers to again circulating tokens 1:1 with exceptionally secure, liquid belongings comparable to money, short-dated US Treasuries, and Federal Reserve-eligible repurchase agreements.

This statutory framework has created a pointy operational divide between stablecoin issuers and industrial banks, with the latter allowed to just accept deposits to increase credit score, handle advanced maturity transformations, use leverage, and generate fractional-reserve cash.

Alternatively, the regulated stablecoin issuers operate strictly as full-reserve transaction autos, prohibited from lending or leveraging reserve belongings and structurally mitigating the “attain for yield” that traditionally triggered money-market disruptions.

Regardless of these authorized separations, industrial banks view the enlargement of stablecoins as an existential balance-sheet risk.

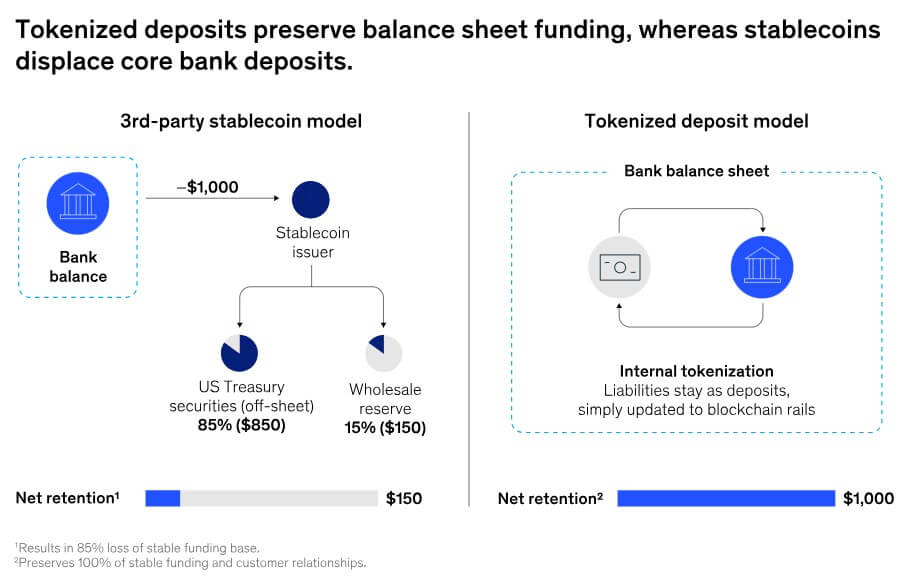

When an enterprise or retail shopper exchanges fiat foreign money for a third-party stablecoin, that liquidity is successfully drained from the standard banking system.

This shifts the monetary relationship from a closely regulated deposit establishment to a non-bank digital issuer, costing the financial institution entry to important cost knowledge, transaction charges, and, most critically, low-cost funding.

In consequence, Wall Road has more and more mounted a direct technological counteroffensive in opposition to the rising business.

Banks construct a $4 trillion on-chain counterweight

To guard their steadiness sheets from this nonbank disintermediation, conventional monetary establishments are shifting aggressively onto the blockchain with their very own various: tokenized deposits.

A tokenized deposit updates the technical kind issue of a standard checking account by putting deposit liabilities instantly onto blockchain rails.

As a substitute of a company treasury division offloading money to a third-party crypto wrapper like USDT or USDC, the shopper retains their deposit relationship with a regulated industrial financial institution.

The shopper captures the basic operational benefits of blockchain expertise, comparable to smart-contract programmability, near-instant settlement finality, and automatic reconciliation, whereas protecting their capital securely contained in the established banking perimeter.

This structural structure offers industrial banks with a strong aggressive benefit. As a result of tokenized deposits are merely conventional financial institution liabilities represented on a ledger, they routinely inherit current authorized, regulatory, and clearing frameworks.

Moreover, they circumvent a significant industrial limitation of stablecoins: whereas licensed stablecoin issuers are largely prohibited from paying yield to token holders below world regulatory frameworks, industrial banks can leverage their conventional fractional-reserve lending operations to pay aggressive rates of interest on tokenized balances.

Whereas stablecoins dominate public media protection, bank-led tokenization networks have quietly achieved an order-of-magnitude greater transaction quantity.

Whole stablecoin cost exercise is estimated to achieve $400 billion in 2025; in contrast, institutional tokenized deposit networks are at the moment on monitor to facilitate greater than $4 trillion in annual transaction quantity, McKinsey famous.

A lot of this immense quantity is pushed by proprietary wall-garden infrastructure comparable to JPMorgan Chase’s Kinexys, which is estimated to course of greater than $1 trillion yearly for inner company treasury actions, cross-border intercompany settlements, and wholesale liquidity positioning.

These large monetary flows happen deep inside permissioned, institutional ledger environments moderately than on public, retail-facing blockchains, making them much less seen to the general public however deeply disruptive to world company banking.

Nevertheless, the first vulnerability of the banking sector’s technique is extreme community fragmentation.

Whereas stablecoins take pleasure in large community results resulting from their native interoperability throughout public blockchains, tokenized deposits are at the moment confined to closed, single-bank permissioned networks.

A tokenized greenback minted on one financial institution’s proprietary blockchain can not naturally work together with a sensible contract operating on a competitor’s ledger, threatening to interchange legacy correspondent banking friction with a brand new community of remoted digital islands.

Overcoming this impediment requires intensive authorized and operational coordination moderately than purely technical fixes.

To attain true interbank fungibility, worldwide banking coalitions are actively testing shared orchestration networks and unified ledger initiatives, together with the Financial institution for Worldwide Settlements’ Mission Agorá, the Swift orchestration layer, Partior, and Chainlink’s CCIP.

Digital {dollars} transfer towards a layered system

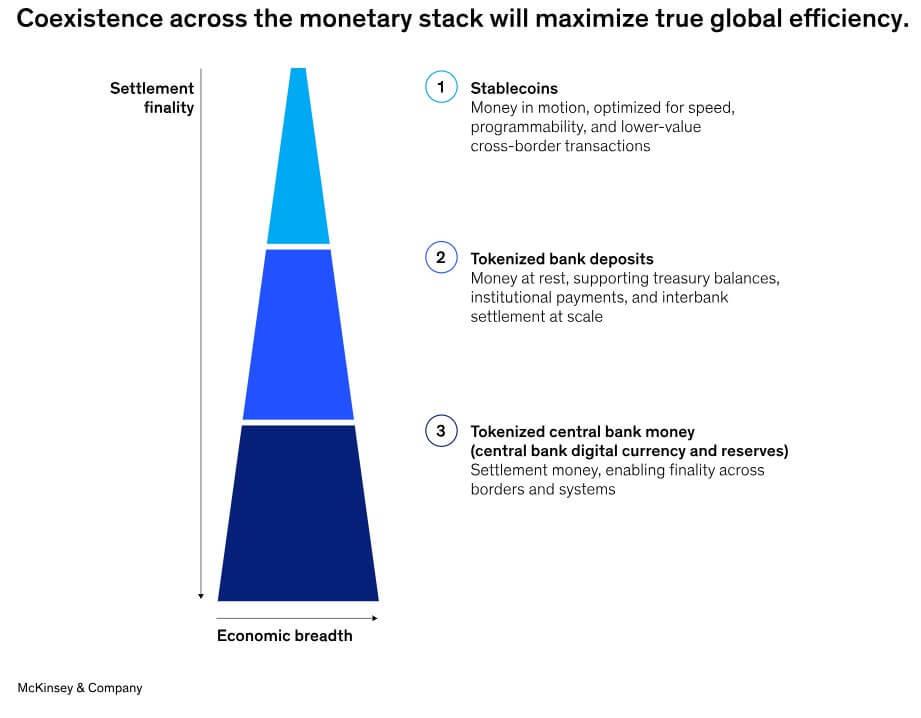

The unfolding battle between crypto-native companies and Wall Road giants means that the way forward for digital cash won’t be dominated by a single token or platform.

As a substitute, the worldwide monetary system is steadily organizing itself into a classy, three-layer digital-dollar financial stack, the place distinct types of tokenized worth fulfill extremely specialised financial roles:

- Stablecoins: “Cash in Movement”

Positioned on the user-facing prime layer of the stack, open-source stablecoins like USDC and USDT will possible preserve their dominance throughout public, permissionless networks.

Their deep change liquidity, borderless accessibility, and frictionless distribution make them the perfect instrument for retail digital asset buying and selling, decentralized finance (DeFi) protocols, peer-to-peer world remittances, and cross-border industrial transactions in areas missing steady native banking infrastructure.

- Tokenized Financial institution Deposits: “Cash at Relaxation”

Occupying the institutional mid-layer, bank-led tokenized deposits are poised to turn into the default settlement asset for high-value company finance.

As a result of they protect institutional financial institution steadiness sheets, provide regulatory alignment, allow curiosity accumulation, and combine instantly with legacy cash-management companies, these devices are structurally optimized for company treasury balances, wholesale enterprise funds, and large-scale industrial financial institution settlements.

- Tokenized Central Financial institution Cash: “Settlement Cash”

Forming the sovereign basis of your entire system, wholesale central financial institution digital currencies (CBDCs) and tokenized central financial institution reserves will function the last word risk-mitigation layer.

Working primarily behind the scenes, this sovereign asset shall be used strictly to resolve imbalances and execute closing, irrevocable settlements between disparate industrial financial institution networks, thereby eliminating institutional counterparty threat on the macro degree.

Finally, the record-breaking $322 billion stablecoin market proves that the market demand for a modernized, real-time digital greenback is everlasting.

On the identical time, the $4 trillion scale of bank-led tokenization proves that conventional monetary establishments don’t have any intention of surrendering the way forward for funds to nonbank crypto enterprises.

As these ecosystems transfer towards inevitability, the definitive battleground will not be over the underlying expertise itself, however over the regulatory perimeters, interoperability requirements, and supreme management of the shopper relationship.