The euro-denominated stablecoin consortium Qivalis has obtained backing from 37 banks throughout 15 nations, and the asset is deliberate to launch within the second half of the yr.

ING famous that stablecoins already serve wholesale cross-border funds and blockchain-based bond settlement, however most of that exercise is denominated in US {dollars}, creating forex publicity for European corporates whose payroll, taxes, and accounting are denominated in euros.

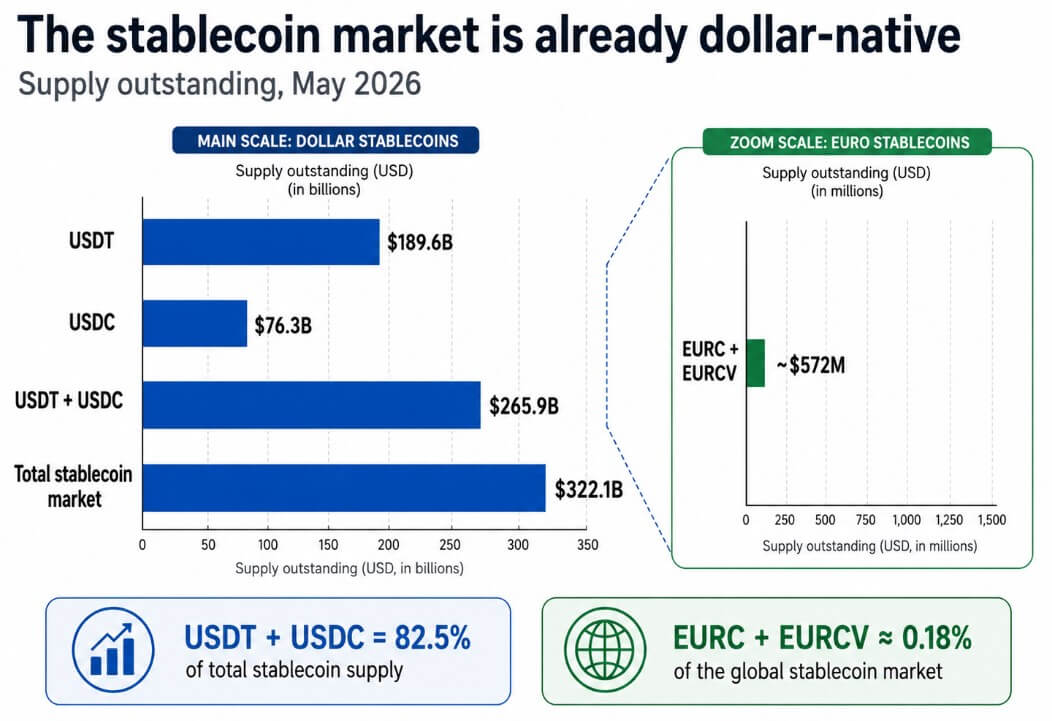

DeFiLlama places the worldwide stablecoin market at $322.1 billion, with USDT at $189.6 billion and USDC at $76.3 billion, accounting for 82.5% of the entire provide.

Circle stories €387.9 million EURC in circulation as of Could 18, whereas SG-FORGE’s EURCV stands at €105.6 million.

These two main euro tokens collectively equal roughly $572 million, about 0.18% of the worldwide stablecoin market, and now Europe’s distribution play should shut a roughly 450-to-1 window earlier than it might probably contest the rails.

Why the greenback’s lead is structural

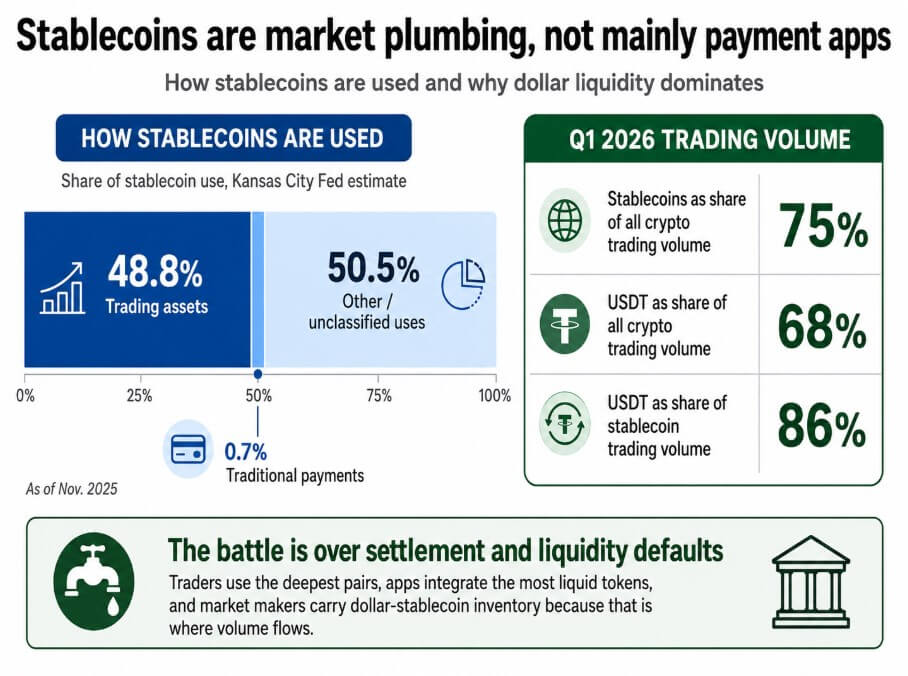

The Kansas Metropolis Fed estimated that as of November 2025, 48.8% of stablecoins had been used as buying and selling property throughout exchanges, finance protocols, and infrastructure, whereas conventional funds accounted for solely 0.7% of stablecoin use.

CEX.IO’s information for the primary quarter exhibits stablecoins accounting for 75% of all crypto buying and selling quantity, with USDT alone accounting for 68% of all crypto quantity and 86% of stablecoin buying and selling quantity.

Merchants use the deepest pairs, purposes combine probably the most liquid tokens, and market makers carry dollar-stablecoin stock as a result of that’s the place quantity flows.

The White Home reality sheet on the GENIUS Act states that the regulation will strengthen the greenback’s standing as a reserve forex and improve demand for US Treasuries by requiring stablecoin issuers to again their property with {dollars} and Treasury payments.

ECB President Christine Lagarde responded in Could 2026 by noting that each greenback stablecoin that scales additionally scales up demand for dollar-backed property, and cited a analysis discovering {that a} $3.5 billion influx into greenback stablecoins can decrease three-month Treasury invoice yields by 2.5-3.5 foundation factors.

RWA.xyz exhibits $33.8 billion in distributed tokenized real-world asset worth and $340 billion in represented asset worth, with tokenized US Treasuries alone at over $15.4 billion. Each tokenized asset has a settlement leg, and most of these legs are at the moment settled in greenback stablecoins.

If European bonds, actual property funds, and commerce receivables proceed to settle in USDT or USDC, European corporates can have moved their property on-chain, making them dollar-native by default.

Europe’s counterattack runs via financial institution networks

Below the EU’s Markets in Crypto-Belongings regulation, euro-denominated stablecoins issued by regulated entities can function throughout member states with out separate nationwide licenses.

That provides Qivalis a compliance benefit that Tether, which holds no MiCA license, can not simply replicate. The bank-distribution layer is what separates Qivalis from EURC, which has but to draw the institutional liquidity required for scale.

The structure being fashioned contains company treasury administration, cross-border provider funds, and settlement of blockchain-based bonds and fund shares. These are institutional workflows the place financial institution connectivity and counterparty help decide adoption.

Qivalis is betting that 37 banks could make euro stablecoins accessible to company treasurers, who obtain stablecoins via their banking companions.

Liquidity traps and regulatory overcorrection

JPMorgan initiatives the stablecoin market will attain roughly $500 billion by the top of 2028, which, from the present $322.1 billion base, implies about 18.6% annualized progress.

In that state of affairs, greenback stablecoins develop proportionally, and the general market fails to develop quick sufficient to offer euro tokens room to construct significant change depth.

Qivalis turns into a compliance product satisfactory for chosen cross-border treasury pilots however unable to reset DeFi collateral preferences or change defaults.

The IMF’s COFER information for the final quarter of 2025 exhibits the euro at 20.25% of world official FX reserves, in contrast with the greenback at 56.77%.

In a bearish case, euro stablecoins replicate that disparity, and European tokenized property proceed to settle in digital {dollars} as a result of USDT and USDC dominate change pairs, DeFi pool depth, and market maker inventories.

If the ECB or nationwide supervisors constrain issuance of public-chain euro stablecoins in favor of tokenized deposits or a CBDC, Qivalis’s financial institution distribution community turns into irrelevant.

Banks that joined to supply a regulated stablecoin could find yourself providing a special instrument that doesn’t interoperate with DeFi protocols or non-EU exchanges below a special framework.

That fragmentation leaves greenback tokens as the sensible default for any transaction crossing the EU perimeter.

The euro settlement beachhead

Normal Chartered initiatives that the stablecoin market will attain $2 trillion by the top of 2028, with as much as $1 trillion in web new demand for Treasury payments.

Reaching $2 trillion from $322.1 billion requires roughly 102.8% annualized progress, or about $54 billion of web provide progress per thirty days via end-2028.

| Situation | 2028 stablecoin market | Euro stablecoin share | Euro liquidity consequence | Strategic which means |

|---|---|---|---|---|

| Bear / greenback entice | ~$500B | <1% | <$5B | Euro tokens stay compliance merchandise; greenback rails dominate settlement. |

| Base / twin rail | ~$1T | 1–2% | $10B–$20B | Europe will get usable home rails, however world liquidity stays USD-led. |

| Bull / euro beachhead | ~$2T | 3–5% | $60B–$100B | Euro stablecoins turn out to be credible settlement property for EU tokenized securities, funds, and company treasury flows. |

In that atmosphere, euro stablecoins capturing 3-5% of the market would imply $60 billion to $100 billion in euro-denominated on-chain liquidity, enough to help real change depth, DeFi collateral use, and tokenized fund settlement at institutional scale.

Euro stablecoins can safe that place by changing into the default settlement asset for EU tokenized securities earlier than these requirements harden round greenback rails, a prize that carries its personal logic unbiased of any displacement of USDT in world crypto buying and selling.

The RWA market continues to be early, which suggests the window to determine euro-denominated settlement rails is open. If Qivalis reaches enough liquidity earlier than tokenized EU property undertake greenback defaults, European monetary infrastructure avoids changing into dollar-native on the plumbing layer.

That consequence would resolve whether or not the following technology of European company finance runs on digital euros or digital {dollars}.

The competition is over settlement defaults

Europe’s objective is to make euro-denominated cash accessible in the mean time when conventional finance strikes on-chain and earlier than defaults set in.

Qivalis’s 37-bank consortium is a guess that institutional distribution can generate the liquidity, counterparty community, and compliance stack integration that corporates require earlier than they route treasury flows via a euro stablecoin.

Whether or not that guess pays off by the top of 2028 will rely on how briskly tokenized asset markets develop, how aggressively European banks activate their Qivalis relationships, and whether or not regulators deal with public-chain euro stablecoins as infrastructure price defending or as a danger price constraining.