Whereas Washington makes an attempt to navigate the stablecoin battle between banks and crypto corporations over the Readability Act, Coinbase has now introduced the “Coinbase Stablecoin Credit score Technique” (CUSHY), focusing on certified buyers and establishments with publicity to public, non-public, and opportunistic credit score.

The agency additionally stated that it provides buyers entry to the structural alpha from tokenization, protocol incentives, and on-chain market construction.

The launch is a direct wager that stablecoins, which topped $33 trillion in transaction quantity in 2025 and had a mean of 89 million each day holding addresses, are mature sufficient to function distribution rails for institutional credit score.

Coinbase already earns closely from stablecoin economics, with $1.35 billion in stablecoin income in 2025, and subscriptions and providers accounting for 41% of internet income, in opposition to complete internet income of $6.88 billion.

Non-obligatory tokenized shares run on Superstate’s FundOS platform, with Northern Belief because the fund administrator, Coinbase Prime because the prime providers supplier, and Base, Solana, and Ethereum because the supported networks.

CUSHY matches Coinbase’s current trajectory by changing stablecoin infrastructure into an asset administration product with recurring institutional relationships.

| Merchandise | Element |

|---|---|

| Product | Coinbase Stablecoin Credit score Technique (CUSHY) |

| Issuer | Coinbase Asset Administration |

| Goal buyers | Certified buyers and establishments |

| Technique focus | Publicity to public, non-public, and opportunistic credit score |

| Extra return sources | Structural alpha from tokenization, protocol incentives, and on-chain market construction |

| Share construction | Non-obligatory tokenized shares |

| Tokenization platform | Superstate FundOS |

| Fund administrator | Northern Belief |

| Prime providers supplier | Coinbase Prime |

| Supported networks | Base, Solana, Ethereum |

| Strategic significance | Turns stablecoin infrastructure into an institutional credit-distribution and asset-management product slightly than a pure funds or buying and selling rail |

The credit score layer stablecoins have not touched but

McKinsey and Artemis estimate precise stablecoin fee exercise at roughly $390 billion in 2025, which remains to be small in contrast with the uncooked $33 trillion on-chain quantity determine that Coinbase cites.

BIS equally discovered annual stablecoin volumes of round $35 trillion in 2025, whereas acknowledging that real-economy use remained modest, with a lot of the uncooked quantity reflecting buying and selling, inner transfers, and automatic exercise.

Solely about $8 billion of that flowed via capital markets settlement in 2025, per McKinsey.

Non-public credit score is probably the most direct bridge between what stablecoins can do and what institutional finance really wants.

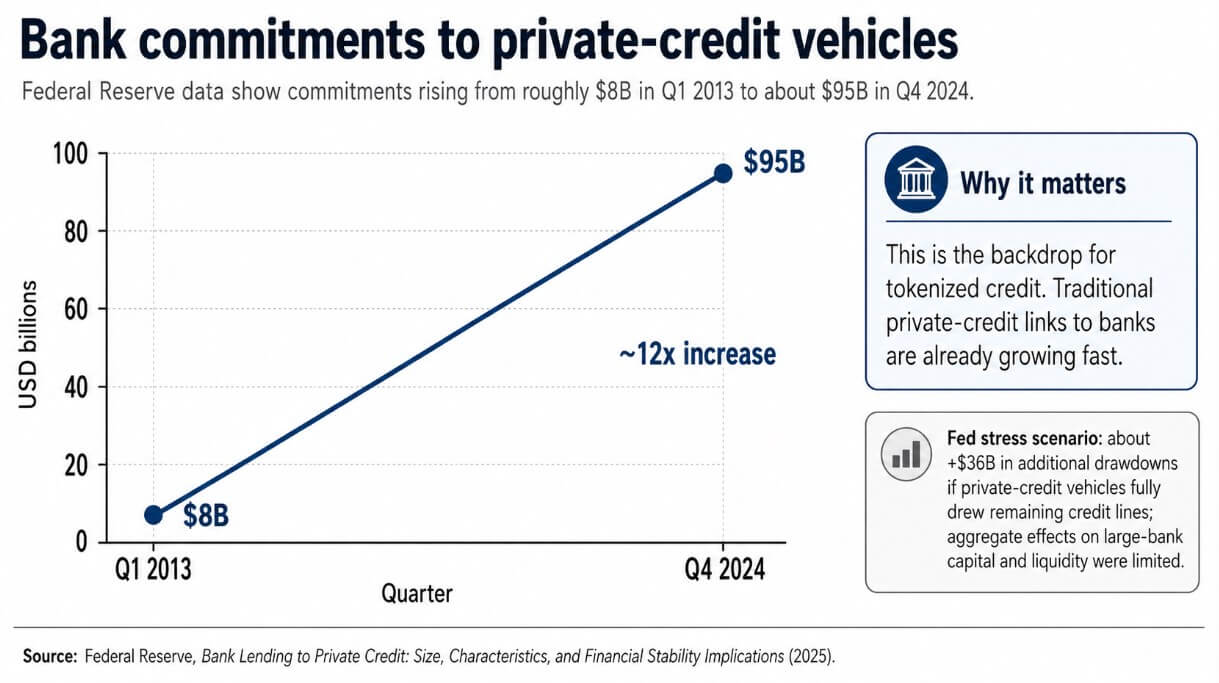

The Federal Reserve tracked financial institution commitments to personal credit score autos, climbing from roughly $8 billion within the first quarter of 2013 to about $95 billion within the fourth quarter of 2024.

That growth occurred totally inside conventional monetary plumbing by way of bilateral relationships, guide fund administration, and restricted secondary-market entry.

In principle, on-chain rails rework subscription and switch mechanics with out affecting credit score underwriting. Coinbase is betting that operational enhancements alone are sufficient to attract institutional allocators towards tokenized buildings.

BCG places tokenized US Treasuries at $13.6 billion in April 2026, whereas RWA.xyz reveals tokenized credit score at $5.01 billion in distributed worth and $21.2 billion in represented worth, with represented worth up 5.54% over the previous 30 days.

Credit score danger survives the wrapper

The expertise improves subscription mechanics, switch velocity, and observability, and the underlying belongings retain all of the opacity, illiquidity, and borrower dependence they’d in any conventional construction.

A tokenized share in a private-credit fund can transfer on a blockchain at any hour; no counterparty can liquidate the underlying mortgage on demand.

That distinction between the wrapper’s obvious liquidity and the asset’s precise liquidity is the oldest danger in structured finance, and tokenization doesn’t resolve it.

Coinbase’s CUSHY leaves the core stress between digital rail velocity and credit score market depth intact.

The Federal Reserve put particular numbers to personal credit score danger, noting a roughly $36 billion improve in drawdowns, with restricted mixture results on giant banks’ capital and liquidity ratios in a stress state of affairs wherein non-public credit score autos absolutely drew down their final credit score traces.

The direct bank-stability implications seem contained for now, however the Fed additionally flagged opacity and intensifying interconnectedness between banks and private-credit autos as components warranting shut monitoring. Coinbase is constructing on a sector the Fed is watching carefully.

The bull case

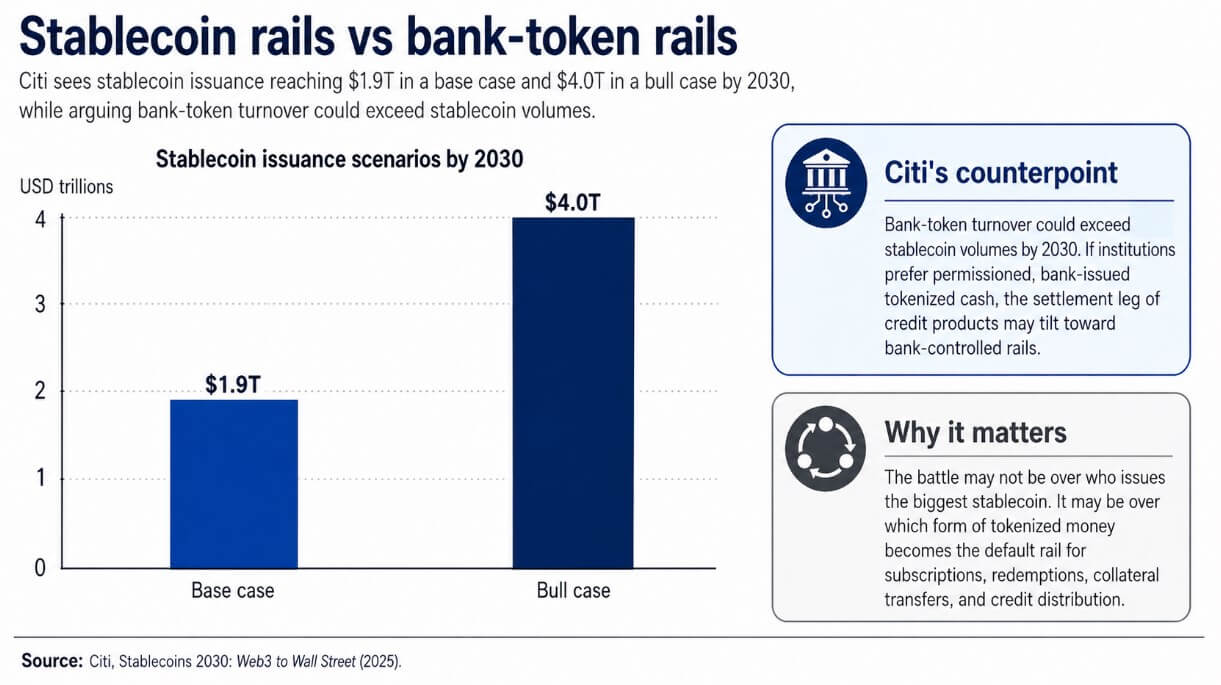

If Citi’s projection of $1.9 trillion in stablecoin issuance by 2030 in its base state of affairs proves directionally proper, CUSHY appears to be like early.

In that surroundings, stablecoins grow to be the default cash leg for fund subscriptions, redemptions, collateral actions, and secondary transfers in private-credit and asset-based-lending buildings.

Coinbase’s current infrastructure stack positions it nearer to that consequence.

The $17.8 billion in common USDC balances held in Coinbase merchandise throughout 2025 reveals that institutional capital already sits inside its infrastructure, and that pointing that capital towards credit score merchandise with recurring administration economics is the pure extension.

Coinbase explicitly frames CUSHY round digitally native debtors migrating to extra environment friendly digital rails, a thesis backed by BIS information exhibiting non-public credit score lending to SaaS companies climbed from roughly $8 billion in 2015 to greater than $500 billion by the top of 2025.

If these debtors desire on-chain entry to capital, an institutional fund already working on tokenized rails and a public-chain stablecoin settlement layer will get there first.

The bear case

Citi’s evaluation presents the counterargument that financial institution token turnover may exceed stablecoin volumes by 2030.

If establishments desire permissioned, bank-issued tokenized money for the settlement leg of credit score merchandise, Coinbase could assist show that institutional credit score belongs on-chain whereas watching probably the most profitable flows consolidate round bank-controlled infrastructure.

The credit score thesis might be right, and Coinbase may nonetheless discover itself competing in opposition to JPMorgan’s tokenized deposit rails and related permissioned programs for the institutional relationship.

The liquidity mismatch danger amplifies that consequence. A credit score occasion or gating episode inside a tokenized private-credit automobile would manifest as an on-chain liquidity failure in buyers’ consciousness, freezing urge for food throughout your entire tokenized-credit class, no matter which issuer induced it.

Coinbase’s first-mover place turns into a legal responsibility if an early stumble units the narrative earlier than the product matures.

The query now’s whether or not institutional allocators belief public chain stablecoin networks greater than the permissioned token programs that enormous banks are constructing in parallel.