The previous Bitcoin playbook ran on the straightforward logic that when world M2 expands, capital flows into danger property, and Bitcoin captures a disproportionate share.

That relationship powered the 2020-2021 bull market, and crypto Twitter spent the higher a part of 2024 charting M2 overlays as proof that the following leg was imminent.

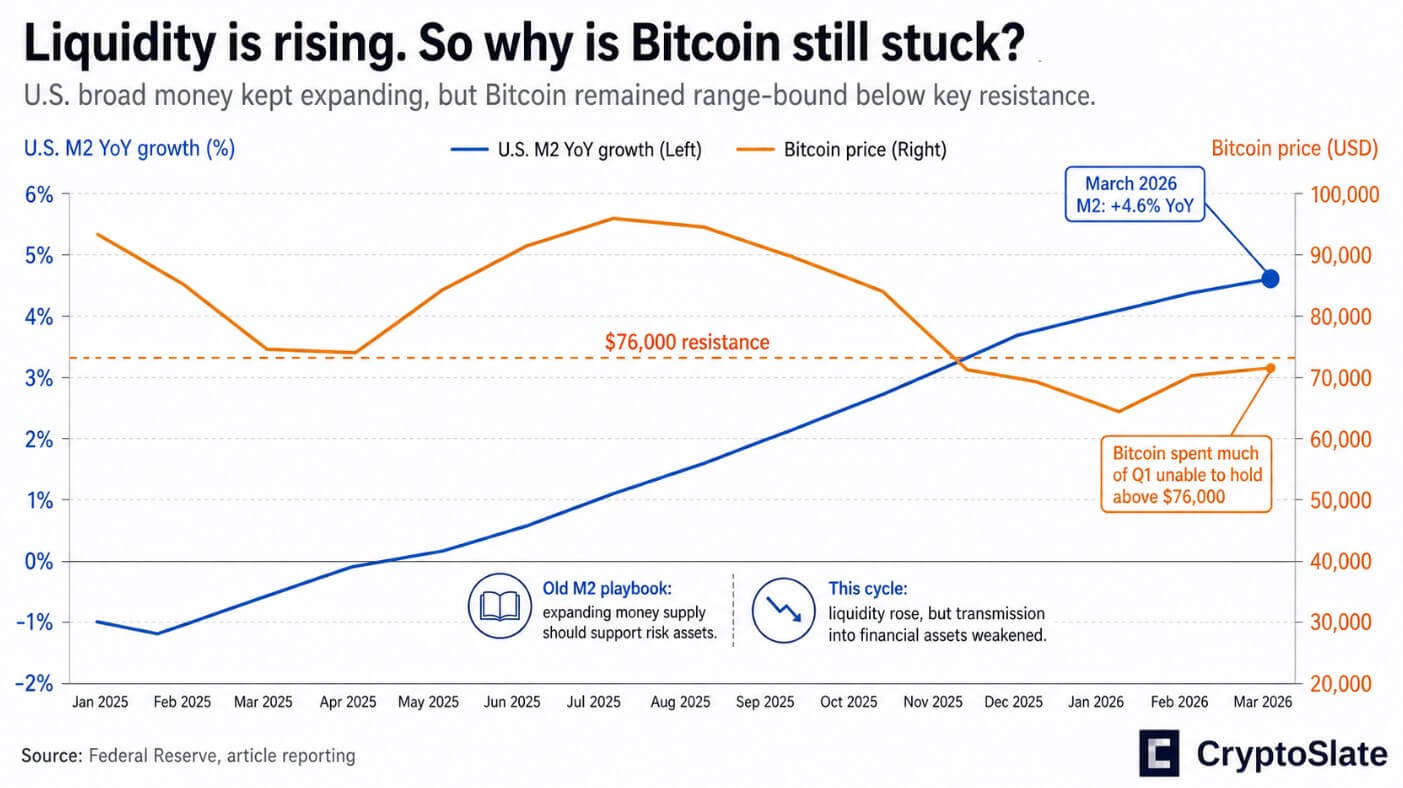

Now, the worldwide M2 has been increasing whereas Bitcoin has continued to underperform.

March 2026 US M2 printed at practically $22.7 trillion, up 4.6% yr over yr, and Bitcoin spent a lot of the primary quarter unable to carry above $76,000, a degree that Actual Imaginative and prescient chief crypto analyst Jamie Coutts recognized as key resistance on CryptoQuant’s Unbiased podcast.

Coutts’ analysis was that the transmission mechanism had modified, because the form of liquidity now determines if the growth really reaches monetary property.

Within the post-2008 QE period, the Federal Reserve purchased property straight, flooding the system with financial institution reserves that had nowhere to go however into equities, credit score, and finally crypto.

At the moment, Treasury issuance, reserve administration, money steadiness swings, and financial institution credit score creation have changed the central financial institution’s balance-sheet firehose.

The plumbing downside

The US public debt closed the fourth quarter of 2025 at over $38.5 trillion, up 6.3% yr over yr. In the meantime, US M2 grew by 4.6% over the identical interval.

Primarily based on probably the most primary numbers obtainable, debt is outpacing broad cash by practically two proportion factors yearly. The debt inventory now equals roughly 1.70x whole M2, a ratio with no trendy precedent in a supposedly accommodative financial atmosphere.

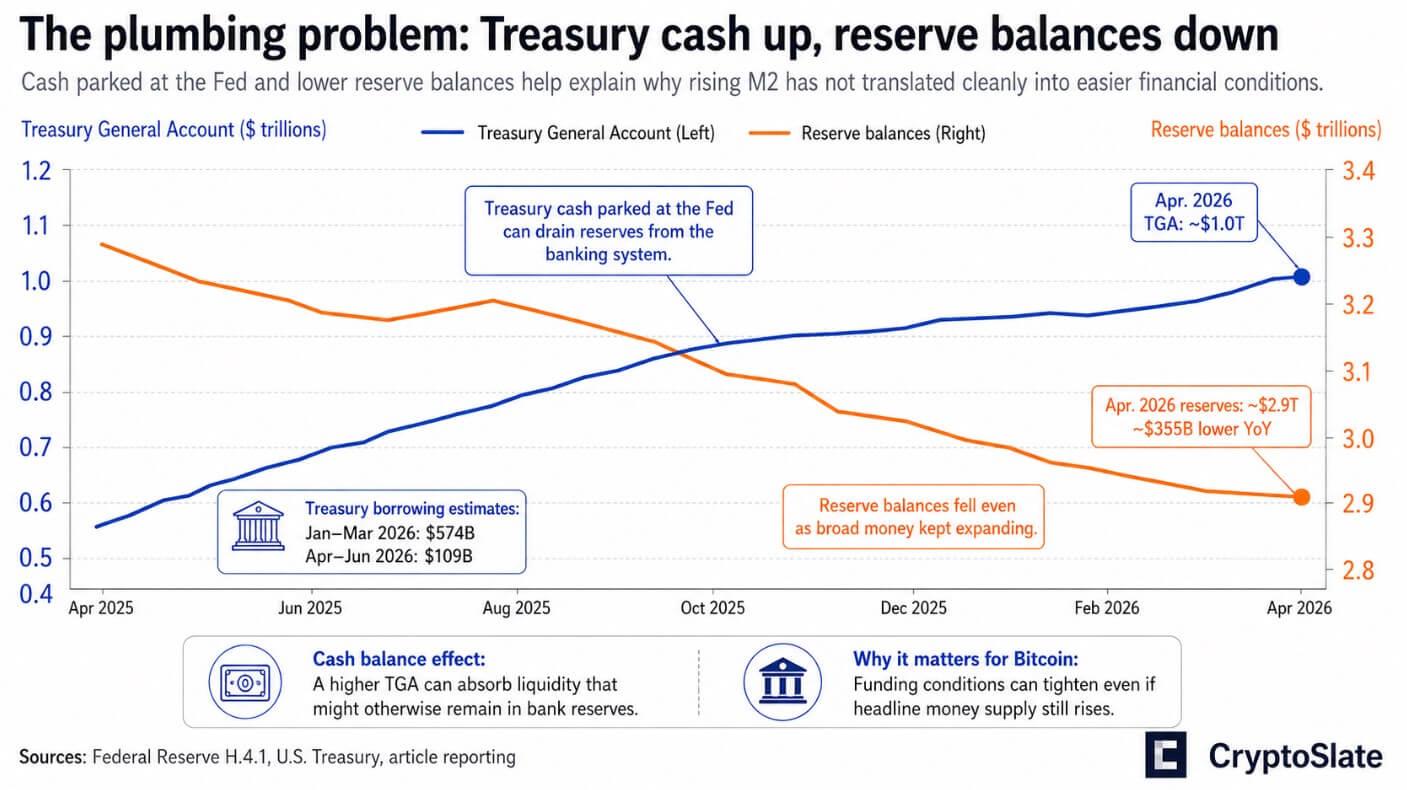

The Treasury’s personal borrowing estimates known as for $574 billion in internet marketable debt within the January-March 2026 quarter and one other $109 billion in April-June, whereas sustaining a money steadiness above $1 trillion.

The Treasury Common Account, which sits on the Federal Reserve, held roughly $1 trillion within the newest H.4.1 knowledge. Money parked on the Fed drains reserves from the banking system whilst M2 continues to tick up.

Reserve balances fell to about $2.9 trillion within the Fed’s Apr. 22 launch, down roughly $355 billion from a yr earlier.

Broad cash expands on paper whereas the plumbing that truly strikes reserves into monetary markets tightens on the margin.

Financial institution credit score remains to be increasing, with industrial loans and leases reaching roughly $13.7 trillion by mid-April, whereas that credit score seems to be flowing into real-economy absorption.

On the Apr. 29 FOMC assembly, the coverage price was held at 3.5%-3.75%, and whole property stayed round $6.7 trillion. Officers cited inflation as their main restraint, with no steadiness sheet growth on the agenda.

Why the previous chart broke

Coutts argued on the podcast that Bitcoin’s underperformance displays plumbing friction.

The selloff from late 2024 into early 2025 drew on tightening reserve circumstances within the fourth quarter, Treasury dynamics tied to a authorities shutdown, derivatives-driven deleveraging, and the increasing function of ETF and derivatives markets in Bitcoin’s worth construction.

None of these forces seem in a world M2 overlay, as they’re options of a monetary system through which Treasury provide, reserve administration, and funding circumstances have turn out to be the true battleground.

Gold affords the clearest cross-market affirmation. Central banks purchased 244 tonnes of gold within the first quarter, up 3% yr over yr, with whole gold demand reaching 1,231 tonnes and a file $193 billion by worth, per the World Gold Council.

Official establishments are hedging sovereign debt credibility at scale, however they’re doing it by means of gold, an asset central banks can legally maintain.

The IMF’s newest Fiscal Monitor discovered that world public debt now appears set to achieve 100% of GDP by 2029, with the US and China driving a lot of the acceleration.

The Congressional Finances Workplace tasks a $1.9 trillion federal deficit in FY2026 and debt held by the general public increasing from 101% of GDP to 120% by 2036, a structural provide overhang that can proceed to compete with danger urge for food for a similar pool of reserves and capital.

Two outcomes

Within the bull case, inflation cools towards the Fed’s projected path, the Treasury money steadiness declines, reserves rebuild, and financial institution credit score continues to increase with no progress scare.

In that setup, the “liquidity remains to be increasing” thesis regains traction. Bitcoin can re-rate shortly as a result of the debt-to-liquidity mismatch prevents the tightening of economic circumstances on the margin.

Coutts handled the $60,000 zone as a worth flooring and put the percentages that the cycle low is already in at higher than 50-50.

Within the bear case, debt issuance stays heavy, inflation stays sticky, Treasury funding pressure persists, and the Fed can’t ease with out reigniting the inflation it has spent two years suppressing.

Bitcoin then behaves much less like a financial hedge and extra like a high-beta danger asset uncovered to charges, funding circumstances, and periodic deleveraging.

The April flash PMI from S&P World already described progress operating near a 1% annualized tempo. This fragile growth doesn’t have to tip into recession to generate the form of funding shocks that hit Bitcoin hardest.

| Issue | Bull case | Bear case |

|---|---|---|

| Inflation | Cools towards the Fed’s projected path | Stays sticky sufficient to maintain policymakers cautious |

| Treasury money steadiness | Declines, lowering reserve drain | Stays elevated, persevering with to soak up liquidity |

| Reserve balances | Rebuild from present ranges | Keep tight or fall additional |

| Debt issuance | Stays manageable relative to liquidity progress | Stays heavy and outpaces liquidity progress |

| Fed stance | Can ease or soften with out reigniting inflation | Can’t ease meaningfully with out risking one other inflation wave |

| Financial institution credit score | Retains increasing with no progress scare | Expands weakly or is offset by tighter funding circumstances |

| Monetary circumstances | Loosen on the margin | Keep restrictive and liable to stress episodes |

| Market plumbing | Treasury provide and reserves cease performing as a headwind | Treasury funding pressure and reserve friction stay the principle battleground |

| Bitcoin habits | Re-rates increased because the liquidity thesis regains traction; $60,000 holds as a worth flooring | Trades like a high-beta danger asset, with sharp drawdowns, failed breakouts, and doable retests of decrease assist |

| Investor takeaway | Increasing liquidity is sufficient to take up debt and assist danger property | Liquidity should be rising, however not quick sufficient to offset debt, reserves, and Treasury provide |

Coutts separates the long-term financial case for Bitcoin from the medium-term worth habits that reserve flows really drive.

In a regime the place debt outpaces broad cash, the place the Fed manages from a restrictive flooring, the place Treasury money balances drain reserves whilst M2 ticks up, the operative query for buyers is whether or not that growth is operating quick sufficient to soak up debt, reserves, and Treasury provide concurrently.

Till debt and reserve circumstances flip decisively in Bitcoin’s favor, the asset will maintain delivering the sharp drawdowns and irritating consolidations that outline a market caught between a constructive long-run thesis and a tighter-than-expected short-run funding atmosphere.