Japan has lengthy been considered one of Ripple’s most fertile markets. SBI’s funding in Ripple dates to 2016, SBI Remit launched Japan’s first XRP-enabled worldwide remittance stream in 2021, and SBI VC Commerce counts XRP amongst its hottest belongings.

When Ripple and SBI introduced in August 2025 that SBI VC Commerce meant to distribute RLUSD in Japan, the transfer learn as a pure extension of an already deep native partnership.

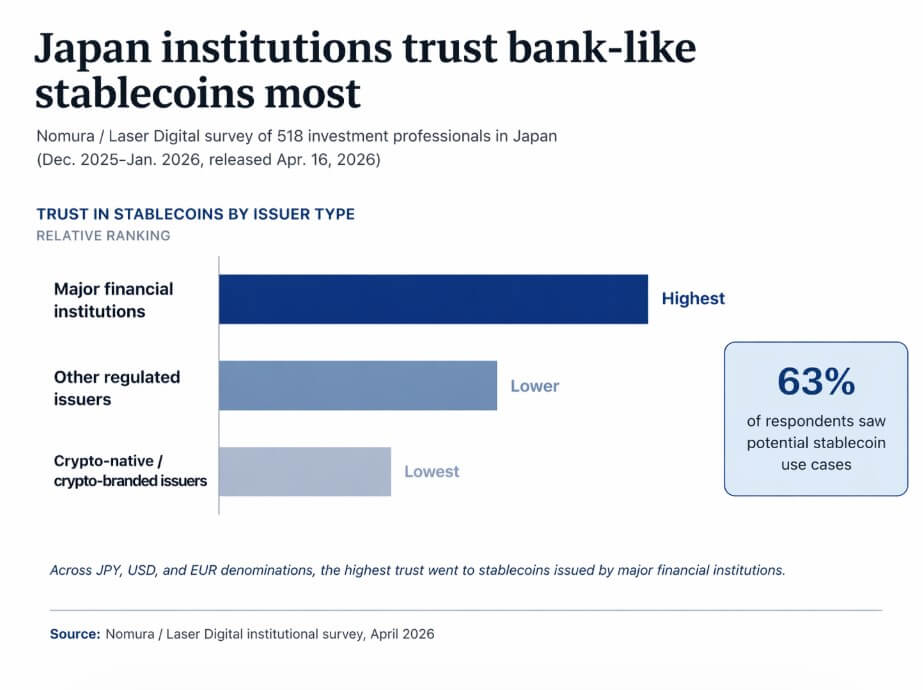

A current survey of 518 funding professionals in Japan, carried out by Nomura and Laser Digital between December 2025 and January 2026 and launched Apr. 16, discovered that 63% of respondents recognized potential makes use of for stablecoins, spanning treasury administration, cross-border funds, crypto investing, and tokenized securities.

Throughout JPY, USD, and EUR denominations, the stablecoins that drew the best institutional belief have been these issued by main monetary establishments.

Japan could also be Ripple’s friendliest proving floor and exactly the place the boundaries of crypto-branded stablecoins turn out to be seen.

Why Japan was purported to be totally different

Ripple’s place in Japan goes past normal distribution agreements. SBI Ripple Asia, a three way partnership shaped from SBI’s 2016 funding in Ripple, has operated as a part of Ripple’s regional infrastructure for almost a decade.

SBI Remit started utilizing Ripple Funds in 2017 and expanded XRP-based remittance corridors into the Philippines, Vietnam, and Indonesia in September 2023.

SBI VC Commerce’s personal investor supplies describe XRP as considered one of its hottest crypto belongings amongst clients.

That basis gave Ripple one thing most stablecoin issuers lack in Japan, which is pre-existing retail familiarity, regulated native companions, and a remittance infrastructure already working on Ripple rails.

RLUSD entered this market with institutional packaging that Ripple itself describes as enterprise-grade, absolutely backed by US greenback deposits, US authorities bonds, and money equivalents, constructed round compliance and built-in into Ripple Funds for cross-border and treasury-style flows.

Nomura’s survey complicates the learn that places Ripple in a robust hand. The belief premium that Japanese establishments place on main monetary establishment issuers displays a structural bias towards acquainted, supervised counterparties.

The FSA’s stablecoin framework limits issuance of digital-money-type stablecoins to banks, fund switch service suppliers, and belief corporations, with redemption and safeguarding necessities connected to every construction.

Financial institution-issued stablecoins provide safety equal to that of standard financial institution deposits. Japan’s regulatory structure, by design, concentrates credibility round supervised monetary entities. Ripple, no matter its compliance posture, falls outdoors that class.

The competitors already constructing

RLUSD’s deliberate distribution via SBI VC Commerce, nonetheless described in late 2025 SBI investor supplies as pending approval, falls inside a subject that Japan’s established monetary establishments are actively growing.

In November 2025, MUFG Financial institution, Mizuho Financial institution, SMBC, and Mitsubishi UFJ Belief and Progmat introduced an FSA-supported proof of idea for joint stablecoin issuance and cross-border settlement.

SBI’s personal supplies present that USDC is already permitted in Japan via its relationship with Circle, that RLUSD is deliberate for itemizing as soon as approval is cleared, and {that a} JPY-pegged stablecoin examine is underway with SMBC.

That aggressive image reframes what RLUSD is definitely competing for in Japan.

| Use case / market lane | Possible belief benefit |

|---|---|

| Cross-border funds | RLUSD / Ripple-linked infrastructure |

| Worldwide remittances | RLUSD / Ripple-linked infrastructure |

| Trade liquidity | RLUSD / crypto-linked issuers |

| Treasury administration | Main monetary establishment issuers |

| Tokenized securities settlement | Main monetary establishment issuers |

| Home company funds | Main monetary establishment issuers |

The open query is which issuer sorts will seize the highest-trust, highest-value institutional use circumstances, as Nomura’s 63% determine places adoption itself past doubt.

Treasury administration, tokenized securities settlement, and home company funds are the use circumstances most delicate to issuer id. Cross-border funds, trade liquidity, and worldwide remittances are the use circumstances the place Ripple’s current infrastructure and RLUSD’s design are strongest.

Ripple constructed its place in Japan via funds and remittances, and RLUSD’s rollout plan factors in the identical path. Nomura’s belief information factors to establishments reaching out to issuers with steadiness sheets and deposit protections they already acknowledge for broader use circumstances.

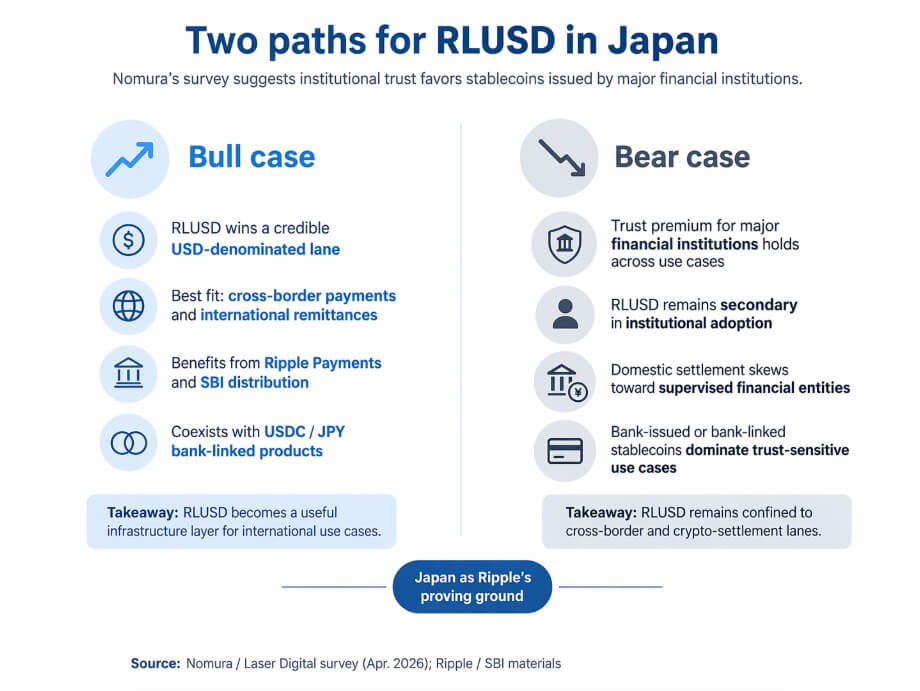

Two paths from right here

The bull case for RLUSD in Japan is determined by how narrowly establishments truly apply the belief premium captured by Nomura’s survey.

If Japanese establishments draw a sensible distinction between issuer id for home yen-denominated settlement and issuer id for USD-denominated cross-border infrastructure, RLUSD has a reputable lane.

Ripple Funds already routes worldwide flows, SBI VC Commerce already serves institutional crypto shoppers, and RLUSD, as a compliant USD stablecoin built-in into an current cross-border fee community, might occupy the USD settlement position in Japan’s institutional stack without having to win the home belief competitors outright.

In that state of affairs, RLUSD turns into a reputable infrastructure for worldwide use circumstances, whereas SBI’s parallel USDC and JPY stablecoins deal with home demand.

Ripple’s enterprise positioning would show adequate for the lanes it already occupies, even when it doesn’t broaden into the higher-trust home settlement enterprise.

The bear case follows instantly from Nomura’s information and Japan’s issuer construction.

If the belief premium for main monetary establishment issuers proves sticky throughout all stablecoin use circumstances, RLUSD will stay secondary within the Japanese institutional market no matter its compliance credentials.

Banks and belief corporations constructing their very own stablecoin merchandise carry the deposit-protection framing and regulatory familiarity that Nomura’s respondents seem to prize.

RLUSD, nevertheless well-packaged, arrives as a crypto-network product distributed via a neighborhood associate. This can be a construction that Japanese establishments should learn as crypto-adjacent, outdoors the supervised monetary entity class that Nomura’s belief premium rewards.

In that consequence, RLUSD’s presence in Japan mirrors its world positioning as helpful for Ripple Funds flows and trade liquidity, with home institutional settlement concentrated amongst supervised monetary entities.

That might be a significant ceiling even in Ripple’s friendliest market.

Nomura’s wording is “main monetary establishments.” That distinction creates some house for non-bank-regulated issuers to compete on belief grounds, significantly fund switch service suppliers and belief corporations that fall inside Japan’s issuer-authorization framework.

The 63% use-case determine displays present institutional pondering amongst asset managers, household places of work, and public curiosity organizations.

That demand exists now, and it’ll stream towards merchandise first. The open variable is which merchandise seize the most important share of its trust-sensitive demand.

The broader body

Ripple’s place in Japan provides it an unusually helpful vantage level on the stablecoin belief query.

If RLUSD finds a sturdy institutional foothold in Japan regardless of the belief premium Nomura’s survey paperwork, that will reveal that compliance framing and native distribution can compete with issuer id even in a bank-centered market.

If RLUSD stays confined to the cross-border and crypto-settlement lanes the place Ripple already operates, that will verify that belief in a funds community and belief in a stablecoin issuer are distinct, and that Japan’s institutional market retains them separate.

The megabank stablecoin buildout continuing in parallel solutions the identical query from the opposite aspect. MUFG, Mizuho, and SMBC are constructing stablecoins with the intent of competing within the home belief market themselves.

Japan is a preview of what institutional stablecoin markets appear like when the monetary institution arrives with its personal merchandise, its personal issuer credibility, and a regulatory framework designed round its personal construction.